JLGutierrez

Here’s a company with one approved product in one rare disease, another product just approved and about to be launched, revenue guidance for full year 2023 being “between $390 million and $395 million,” and little to no debt – but a market cap of just $1.7bn. We have seen preclinical companies with higher market caps, haven’t we? Then why does this company stock fall drastically on raising just $150mn?

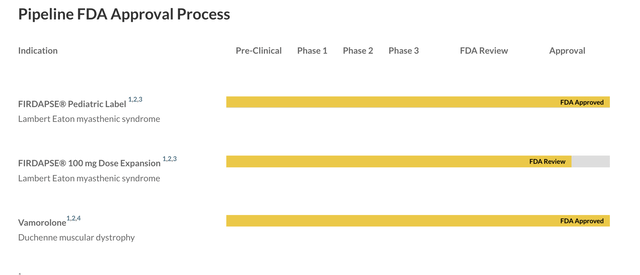

The problems with Catalyst Pharmaceuticals, Inc. (NASDAQ:CPRX) are that it has no major data catalysts to speak of, it has a major patent challenge brewing, it is low on cash with very high R&D and G&A expenses, and it has no pipeline molecule beyond the approved drugs. The current pipeline looks like this:

CPRX PIPELINE (CPRX WEBSITE)

The company is doing due diligence to acquire another epilepsy product after FYCOMPA, however, as they noted in their Nov earnings call, there is no immediate plan to complete such a buy:

And so we’ve made it clear that from a strategic plan that our emphasis on our next acquisition really we’d like it something to be compatible with our epilepsy franchise, and we think it’s a growing opportunity and clearly we’ve made that point. I would not say that there is anything imminent. We are in deep diligence from a couple of opportunities.

I covered CPRX in April, and I mainly focused on the patent issue. I covered the same patent issue in a January article; before that, I had last covered CPRX in 2018, right after the first Firdapse approval in LEMS. The patent issue began after Teva Pharmaceutical (TEVA) filed an ANDA and questioned the validity of 6 Orange Book listed patents held on Firdapse. The earlier of these patents expire in 2032, so, with any luck, CPRX had 9 more years left to get revenue from Firdapse, which means, given the ~$400mn they made last year from the drug, and assuming a 10% growth for 9-10 years, that the drug is worth at least $8bn to CPRX, in simplistic terms. This is what they stand to lose over the ANDA issue.

I discussed the ugly 3,4-DAP story in details earlier. Frankly, it does not make me happy that something like this can be possible. Medicine can be a terribly ugly business, but this is not the right place to run an ethics monologue. Long story short, there is some merit to the ANDA, in my opinion. Courts have already ruled against the ANDA in a way when they ruled against Jacobus, but we will have to see how it works out. As I noted in my 2018 article, though, about the molecule:

…a base formulation discovered by Scottish scientists in the 1970s, used worldwide for decades for a nominal price or for free, and now being marketed with exclusive pricing simply by adding a phosphate base to the chemical indeed seems somehow wrong. The phosphate salt does nothing except to make the drug preservable without refrigeration.

However, in retrospect, I don’t think it is as black and white as I made it out to be. Phosphate salts are commonly used to make medicinal products stable. However, Jacobus never bothered to try this out. The question should be: what happens when 3,4-Diaminopyridine (3,4-DAP) becomes unstable and breaks down? What are the byproducts of that reaction? Are these byproducts safe? How common would it be for a LEMS patient to mistakenly ingress such a byproduct when taking 3,4-Diaminopyridine (3,4-DAP)? Does the new version from CPRX, which adds the phosphate salt, remove this problem? If it does, it does not only make 3,4-Diaminopyridine (3,4-DAP) more stable and give it longer shelf life – it also makes it safer.

On top of that, there are clinical trials to prove the safety and efficacy of the formulation. Jacobus did not do these trials – neither, for that matter, did TEVA. Therefore, CPRX did add value to the original compound, 3,4-Diaminopyridine (3,4-DAP). Thus, they should be allowed to profit from their entrepreneurship, if not for their innovation.

These are moral questions, and investors might wonder why I am bothering them with this. However, someday a judge is going to couch these thoughts in legal language and make a decision on that ANDA. These questions will then look worthwhile, all $8bn of it.

Financials

CPRX has a market cap of $1.7bn and a cash balance of $121mn. The company filed a $500mn shelf offering in September, and ended up with a $150mn secondary offering in January. This value should be added to their cash balance, along with profits, if any, from the quarter. Product revenues in the third quarter of 2023, were $102.6 million, compared to $57.2 million for the third quarter of 2022, representing an increase of 79.5% year-over-year. This includes FYCOMPA net product revenues of $36.4 million, which is a new addition. Research and development expenses were $83.7 million, while selling, general, and administrative expenses were $33.6 million. The company said full-year 2023 total revenues would be between $390 million and $395 million. Given this rate of expenses, and ignoring profits, they do not have cash for more than 2 quarters.

Bottom Line

Catalyst stock plummeted considerably two weeks ago after posting that offering. The stock still has not recovered. This presents an opportunity of sorts for Catalyst Pharmaceuticals, Inc. shares, if you are willing to bet that the ANDA will be resolved in its favor. I have no particular opinion on that, so I will remain neutral despite the attractive drop in price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}