Revealed on August eleventh, 2022 by Josh Arnold

When buyers consider sectors within the inventory market which can be susceptible to have dividend longevity, the expertise sector usually isn’t one which involves thoughts. The tech sector itself isn’t sufficiently old to rival the longest standing dividend streaks present in different sectors, and lots of firms inside IT have enterprise fashions which can be too risky to generate sustainable dividends.

Nonetheless, not all tech shares are created equal.

Pc Providers (CSVI) is an IT inventory that has boosted its dividend for a particularly spectacular 50 consecutive years. That makes it stand out not solely amongst different IT shares, however actually, amongst nearly every other inventory available in the market immediately.

It additionally lands Pc Providers on the checklist of Blue Chip shares, a bunch of greater than 350 firms which have boosted their dividends for at the very least 10 consecutive years. These firms have stood the take a look at of time and aggressive threats to return ever-higher quantities of capital to shareholders.

With this in thoughts, we’ve created an inventory of 350+ Blue Chip shares, which you’ll obtain by clicking beneath:

Along with the Excel spreadsheet above, we’re individually reviewing the highest 50 blue chip shares immediately as ranked utilizing anticipated whole returns from the Certain Evaluation Analysis Database.

This text within the 2022 Blue Chip Shares In Focus sequence will analyze Pc Providers’ enterprise mannequin, development prospects, and whole returns.

Enterprise Overview

Pc Providers is an IT firm that serves principally monetary firms within the US. It presents core processing, digital banking, managed companies, funds processing, regulatory compliance, and different companies to banks and different companies. It has a protracted slate of companies that assist smaller monetary establishments with duties that might be cost-prohibitive to supply themselves, and the corporate has created a pleasant area of interest for itself over the a long time.

Pc Providers was based in 1965, produces about $320 million in annual income, and has a market cap of $1 billion immediately, following sizable weak spot within the inventory in 2022.

The corporate reported first quarter earnings on July eleventh, 2022, and outcomes had been robust, producing file income and earnings for the quarter.

Supply: Q1 earnings launch

Income was up 5.7% to $81 million in Q1, with development coming from increased gross sales in digital banking, funds processing, cybersecurity, and doc supply. Excluding contract termination charges, natural income was up 6.1% in Q1.

Working bills had been up 6.4% to $61.6 million, which was attributable to increased advertising and marketing and journey bills, increased price of products offered on higher volumes in funds processing, digital banking, doc supply, and cybersecurity, in addition to elevated software program and tools bills. These had been partially offset by decrease personnel prices attributable to decrease profit-sharing plan contributions.

Working revenue was up 3.7% to $19.5 million, slower than the speed of income development attributable to expense development. That meant working margin was 24% of income, down from 24.5% a 12 months in the past.

Internet revenue was up 2.3% to $14.7 million, or up 3.8% on a per-share foundation at 54 cents for Q1.

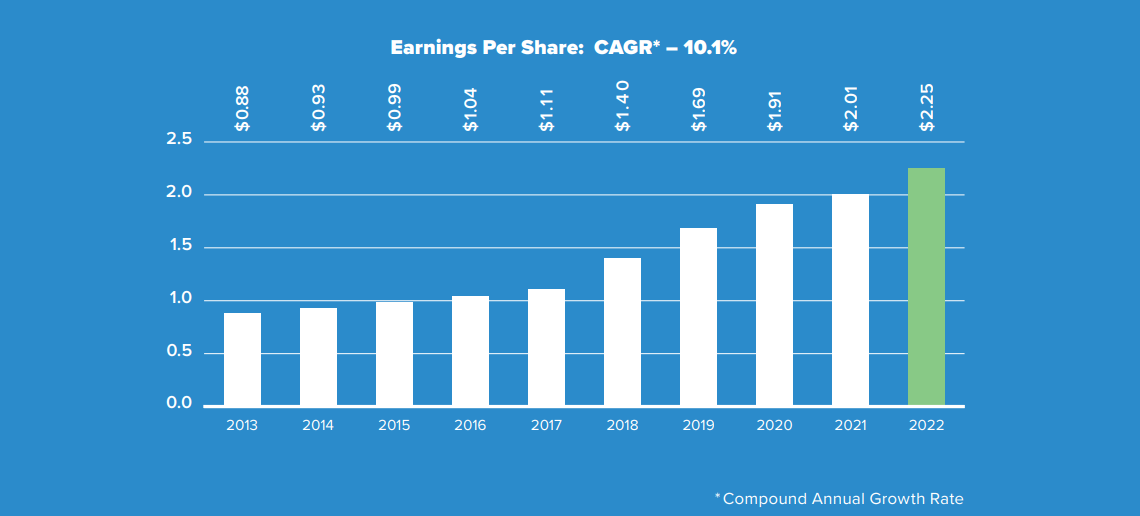

Progress Prospects

Pc Providers has a really spectacular historical past of development, with the previous decade seeing a median annual enhance in earnings-per-share of greater than 10%. As well as, the corporate has produced increased earnings yearly in that interval. That observe file places Pc Providers in uncommon firm, significantly amongst firms that serve monetary establishments.

Supply: Annual report

We don’t see that type of development as sustainable, however we do anticipate 7% annual earnings-per-share development within the years to return. We imagine the corporate can develop earnings through a mixture of income development, a small measure of margin growth, and to a lesser extent, share repurchases. Pc Providers prioritizes the dividend, then capital expenditures, then share repurchases on the subject of using its money movement.

The dividend has grown at greater than 14% on common previously decade, and once more, we see that degree as unsustainable. Nonetheless, we do assume 10% dividend development is attainable as the corporate continues to develop earnings, and return a lot of its free money movement to shareholders.

The corporate’s steadiness sheet can be in terrific form, because it has no long-term debt, however has a $76 million money place as of the top of the primary quarter. Given this, even when earnings had been to dip briefly, we imagine administration would defend the dividend in any respect prices.

Aggressive Benefits & Recession Efficiency

Whereas Pc Providers is definitely a small operator in what’s a really massive IT sector, it has created a distinct segment with smaller monetary establishments that has served it properly over the a long time. The corporate competes the place it will be inefficient for larger gamers on condition that the market isn’t that huge. However Pc Providers has carved out a terrific, worthwhile enterprise and it has model recognition in consequence.

Recessions aren’t sort to banks, and given banks are the corporate’s prospects, earnings may very well be crimped throughout a recession. Nonetheless, Pc Providers’ choices are requirements for its prospects, so they can not merely cease cost processing, or different core companies. We due to this fact imagine recession resilience is sort of good for Pc Providers, and the way it’s been in a position to increase its dividend for half a century.

The payout ratio is beneath 50% of earnings for this 12 months, and at the side of the clear steadiness sheet and sturdy development outlook, we’ve no worries about dividend security going ahead.

Valuation & Anticipated Returns

We assess truthful worth for the inventory at 17.4 occasions earnings, however shares commerce immediately at simply 15 occasions earnings. That suggests we may see a ~3% annual tailwind to whole returns ought to the valuation reflate to normalized ranges.

The dividend yield can be as much as 2.9% immediately, following dividend raises and inventory value weak spot. That’s about double the S&P 500’s yield, so the inventory is enticing on an revenue foundation as properly.

Coupled with our 7% development estimate, we see whole annual return potential of 13% within the years to return, placing the inventory firmly into ‘purchase’ territory.

Ultimate Ideas

Pc Providers is definitely not one of many largest dividend shares accessible immediately, however we see the area of interest the corporate has carved out as very enticing. It helps long-term earnings development, the administration crew may be very shareholder-friendly, and the inventory presents enticing whole return potential.

The dividend enhance streak can be at 50 years, placing Pc Providers in rarified firm on that measure, and we see it as enticing for worth buyers, these in search of a excessive yield, and development inventory buyers.

The Blue Chips checklist is just not the one method to shortly display for shares that often pay rising dividends.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}