Mauricio Graiki/iStock Editorial via Getty Images

Banco do Brasil S.A. (OTCPK:BDORY) has had a strong year, but 2023 will be more challenging, given the prospect of a macro downturn ahead. Still, I maintain a bullish fundamental view. For one, the strong ROE guide is supported by revenue growth momentum YTD and initiatives to unlock more operating leverage in the coming quarters. Plus, asset quality has outperformed peers through the headwinds thus far, and any economic growth slowdown will be somewhat offset by easing inflation and an improving labor market.

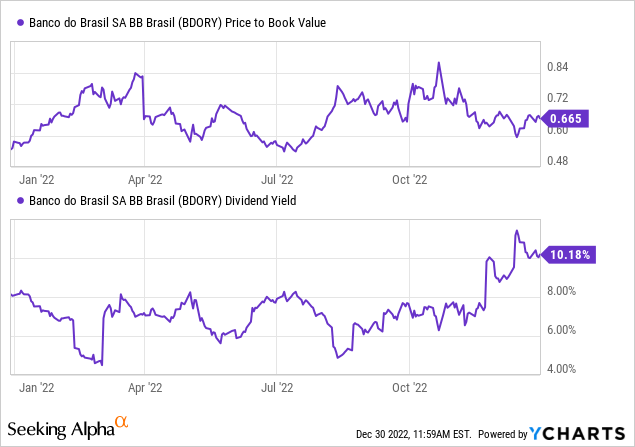

As Banco do Brasil S.A. is a state-owned company, governance risks remain, though, particularly with potential management changes post-election. Yet, times have changed, and the bank has better controls in place to protect minority shareholder rights, including via policies on Board composition and succession planning. At ~3x fwd P/E and 0.6-0.7x P/Book, despite being on target to deliver an >20% ROE this year, there is far too much pessimism priced into the stock, in my view. A well-covered double-digit % dividend yield means investors get paid to wait.

Post-Election Governance Concerns Likely Are Overblown

Going forward, there remain uncertainties around the fiscal outlook and the pending appointment of a new Finance minister following the election. As a state-owned bank, Banco do Brasil is particularly exposed to policy decisions by the federal government; chief among them being the appointment of a CEO. Recent reports indicate a status quo scenario – the three potential names currently in the running for the CEO position (in addition to the current CEO) are all career employees at Banco do Brasil. So, while the Lower House’s approval of a policy change allowing a person with political ties thirty days (from 36 months prior) before they can take on a management position at a state-owned company is hardly confidence-inspiring, Banco do Brasil looks to be unaffected for now.

More broadly, Brazilian state-owned companies have seen marked improvements in their governance. Banco do Brasil, for instance, has undergone positive changes to its succession policy and other corporate governance initiatives, better protecting minorities from external intervention. For instance, half of the Board is independent, with representation from minority shareholders as well. The listing of its common shares on the ‘new market’ segment of B3 (OTCPK:BOLSY) also grants one vote per share and equal rights with regard to future share sales by the majority shareholder. Still, some overhang is perhaps warranted, pending better visibility on the new administration’s view of public banks and their role in national development. At the current ~30% book value discount, though, the governance concerns seem overblown, in my view.

Banco do Brasil

Asset Quality Intact Ahead of a Tough Macro Outlook

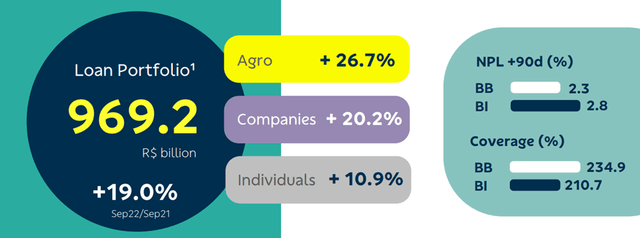

The Brazilian banking sector reported a marked divergence in asset quality in Q3 – while Bradesco SA (BBD) and Itaú Unibanco (ITUB) saw delinquency rates increase, Banco do Brasil outperformed the private banks on the back of its more defensive loan portfolio. This bodes well for the bank heading into a year when asset quality poses the biggest downside risk to Brazil banks’ earnings trajectory. Of note, country-level credit ratios screen unfavorably, with consumer indebtedness on the rise amid higher borrowing costs.

Banco do Brasil

Banco do Brasil has excelled in this regard, transitioning away from credit cards to non-account holders in recent quarters. Per management, credit card approval rates have been cut to 7-10% (from ~30% prior), supporting guidance for the credit card NPL ratio to trend lower in the coming quarters. Impressively, the bank has balanced this pullback without sacrificing adjusted returns, as the credit card segment remains on track for growth. Going forward, the NPL trends in the consumer portfolio will be worth monitoring, along with the overall net cost of risk following sequential growth in Q3.

On Track for >20% ROEs

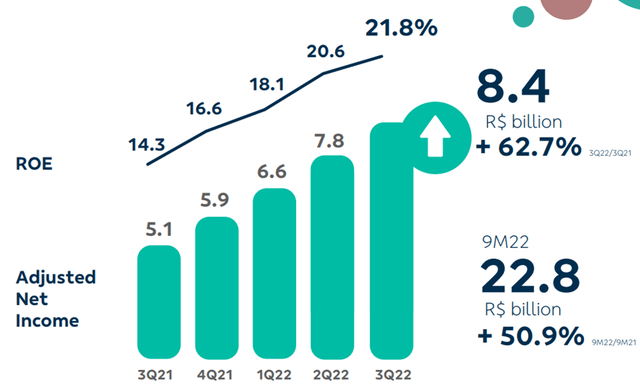

Banco do Brasil delivered a best-in-class 22% ROE result in its last quarter, so its guidance for continued profitability into FY23 was not all that surprising. Higher rates are a tailwind for the net interest margin, but even in a potential H2 2023 rate cut scenario, the bank could still benefit from its liabilities getting repriced lower. By contrast, most of its credit operations are denominated in fixed rates, allowing for a wider spread over the near term. On the revenue side, loans will likely remain the key driver – even a conservative loan growth assumption in line with the system still yields a high-single-digits % YoY outcome.

Banco do Brasil

On the expense side, operating leverage benefits will be key. The bank’s current guidance is for expenses to stay close to the mid-point of its FY22 opex guidance; going forward, though, the efficiency initiatives within its next five-year master plan should yield incremental upside. As a result, I see room for net interest income growth (targeted at high-single-digits %) to outpace loans over time. Net, higher profitability bodes well for the capital position (CET1 is within the 11-12.5% range) and dividend payout (currently at 40%) for 2023, posing upside to the double-digit % dividend yield.

Strong Loan Growth Momentum

Coming off a strong 2022, Banco do Brasil likely won’t have things as good in 2023. Asset quality remains the key concern given the prospect of a more challenging economic environment next year, though there are silver linings. With inflation showing signs of easing and labor conditions improving as well, concerns about consumer debt levels in Brazil could prove unfounded. Plus, the bank continues to see strong loan growth momentum and operating leverage benefits, driving continued >20% ROEs.

While some discount is perhaps warranted given the governance risks related to post-election changes in management (appointed by the government), early signs indicate a status quo scenario at Banco do Brasil. Governance has also improved over the years, and the bank’s non-government shareholders are better protected against political intervention than before. At a ~30% discount to book, despite sustaining best-in-class ROEs this year, most of the downside risks for Banco do Brasil S.A. are likely priced in here. The attractive dividend yield should also appeal to income investors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

stories larger income and earnings for Q1 2025")

{kind=link}