alexsl/iStock Unreleased by way of Getty Photos

Thesis

The inventory market is infamous for fully ignoring enterprise fundamentals at each the greed and really feel excessive, as illustrated by the present situations of Alibaba (NYSE:BABA) and Amazon (NASDAQ:AMZN). The distinction between these two shares is so stark that it not solely serves to point out a selected funding alternative but additionally serves as a common instance of market psychology. Admittedly, these two shares are usually not solely comparable and there are definitely variations. A few of the uncertainties and dangers confronted by BABA are usually not shared by AMZN.

And my thesis right here is that the present market valuation has already priced in all of the dangers surrounding BABA. Extra particularly,

- BABA’s inventory worth has not too long ago turn into dominated by market sentiment and disconnected from fundamentals. Its inventory costs simply fluctuated 10%-plus in a number of days or perhaps a single day not too long ago in response to information and sentiments that will or could not have direct relevance to its enterprise fundamentals. Then again, AMZN’s inventory worth appeared to be immune from information and fundamentals. It has been buying and selling sideways in a slender vary (and at an elevated valuation) regardless of its mounting money movement points and all of the geopolitical and macroeconomic dangers.

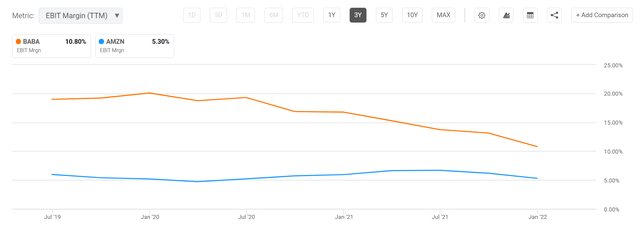

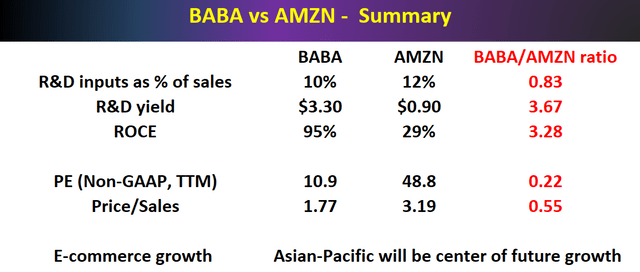

- As proven within the subsequent chart, each BABA and AMZN are valued at about 1.8x and three.2x worth to gross sales ratio, respectively, a reduction by nearly an element of 2x (1.8x to be actual). As we glance deeper subsequent, the low cost turns into even bigger than on the floor. The second chart compares the revenue margin between BABA and Amazon. BABA’s EBIT revenue margin is sort of twice that of Amazon – not solely reveals BABA’s superior profitability (and AMZN’s regarding and deteriorating profitability) but additionally additional highlights the valuation hole. The gross sales of BABA ought to be price about 2x as invaluable as that of AMZN due to the upper margin, however the present valuation is the alternative. And as you have been seeing the rest of this text, BABA additionally enjoys superior fundamentals in different keys points, equivalent to R&D output, return on capital employed, and progress potential.

- Lastly, except for their drastically completely different valuations, there are a lot of comparable points between these two e-commerce giants. And a comparability between them may additionally present insights into the evolving e-commerce panorama. Evaluating what they’re researching and growing provides us a peek on the future funding path on this area.

In search of Alpha In search of Alpha

Each R&D aggressively however BABA enjoys means higher yield

As talked about in our earlier writings, we don’t spend money on a given tech inventory as a result of we have now excessive confidence in a sure product that they’re growing within the pipeline. As an alternative, we’re extra targeted on A) the recurring sources out there to fund new R&D efforts sustainably, and B) the general effectivity of the R&D course of.

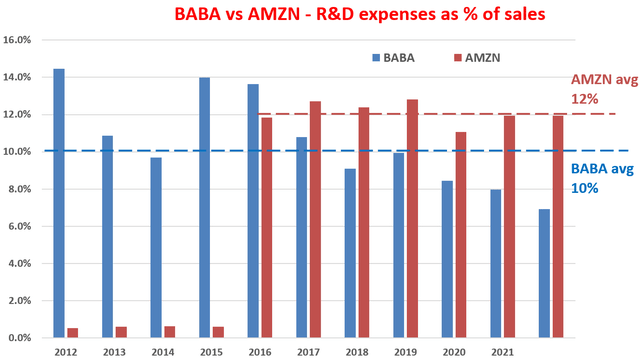

So let’s first see how effectively and sustainably BABA and AMZN can fund their new R&D efforts. The brief reply is: Extraordinarily effectively. The following chart reveals the R&D bills of BABA and AMZN over the previous decade. As seen, each have been persistently investing closely in R&D lately. AMZN did not spend meaningfully on R&D earlier than 2016. However since 2016, AMZN on common has been spending about 12% of its complete income on R&D efforts. And BABA spends a bit much less, on common 10%. Each ranges are according to the typical of different overachievers within the tech area, such because the FAAMG group.

Writer primarily based on In search of Alpha knowledge

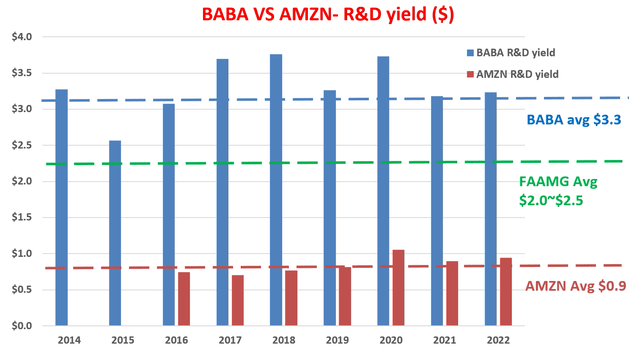

Then the subsequent query is, how efficient is their R&D course of? That is the place the distinction kicks in as proven within the subsequent chart. The chart reveals a variation of Buffett’s $1 check on R&D bills. Suggested by Buffett, we don’t solely take heed to CEOs’ pitches on their sensible new concepts that can shake the earth (once more). We additionally look at the financials to see if their phrases are corroborated by the numbers. And in BABA and AMZN’s circumstances, their numbers are proven right here. The evaluation methodology is detailed in our earlier writings and in abstract:

- The aim of any company R&D is clearly to generate revenue. Due to this fact, this evaluation quantifies the yield by taking the ratio between revenue and R&D expenditures. We used the working money movement because the measure for revenue.

- Additionally, most R&D investments don’t produce any end in the identical 12 months. They sometimes have a lifetime of some years. Due to this fact, this evaluation assumes a three-year common funding cycle for R&D. And in consequence, we used the three-year shifting common of working money movement to signify this three-year cycle.

As you’ll be able to see, the R&D yield for each has been remarkably constant though at completely different ranges. In BABA’s case, its R&D yield has been regular round a mean of $3.3 lately. This degree of R&D yield may be very aggressive even among the many overachieving FAAMG group. The FAAMG group boasts a mean R&D yield of round $2 to $2.5 lately. And the one one which generates a considerably excessive R&D yield on this group is Apple (AAPL), which generates an R&D yield of $4.7 of revenue output from each $1 of R&D bills.

AMZN’s R&D yield of $0.9, however, is considerably decrease than BABA’s and can be the bottom among the many FAAMG group. And observe that since AMZN did not spend meaningfully on R&D earlier than 2016, we solely began reporting its R&D yield beginning in 2016.

Subsequent, we are going to look at their profitability to gasoline their R&D efforts sustainably and likewise dive into a few of the particular R&D efforts they’re endeavor.

Writer

BABA enjoys far superior profitability

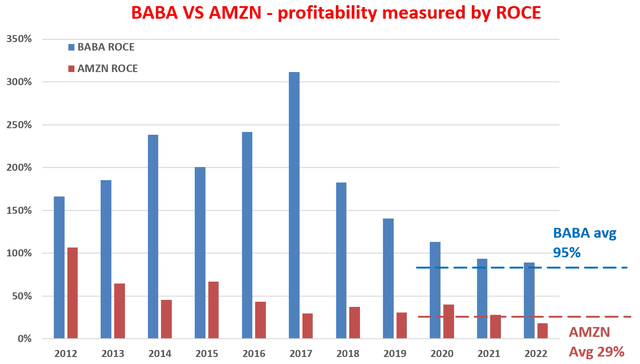

As defined in our earlier writings, to us, an important profitability measure is ROCE (return on capital employed) as a result of:

ROCE considers the return of capital ACTUALLY employed and due to this fact gives perception into how a lot further capital a enterprise wants to speculate to be able to earn a given additional quantity of earnings – a key to estimating the long-term progress charge. As a result of after we assume as long-term enterprise homeowners, the expansion charge is “merely” the product of ROCE and reinvestment charge, i.e.,

Lengthy-Time period Development Price = ROCE * Reinvestment Price

The ROCE of each shares has been detailed in our earlier articles and I’ll simply straight quote the outcomes beneath. On this evaluation, I take into account the next gadgets capital truly employed A) Working capital (together with payables, receivables, stock), B) Gross Property, Plant, and Tools, and C) Analysis and improvement bills are additionally capitalized. As you’ll be able to see, BABA was in a position to keep a remarkably excessive ROCE over the previous decade. It has been astronomical within the early a part of the last decade exceeding 150%. It has declined as a consequence of all of the drama lately that you’re accustomed to (China’s tightened rules, excessive tax charges, slow-down of the general financial progress in China, et al). However nonetheless, its ROCE is on common about 95% lately.

AMZN’s ROCE has proven the same sample. It too has loved a a lot greater ROCE within the early a part of the last decade. And it too has witnessed a gentle decline through the years. Lately, its ROCE has been comparatively low, with a mean of round 29%. A ROCE of 29% remains to be a wholesome degree (my estimate of the ROCE for the general economic system is about 20%). Nonetheless, it is not akin to BABA or different overachievers within the FAANG pack.

Subsequent, we are going to look at their key segments and initiatives to type a projection of their future profitability and progress drivers.

Writer

Development prospects and closing verdict

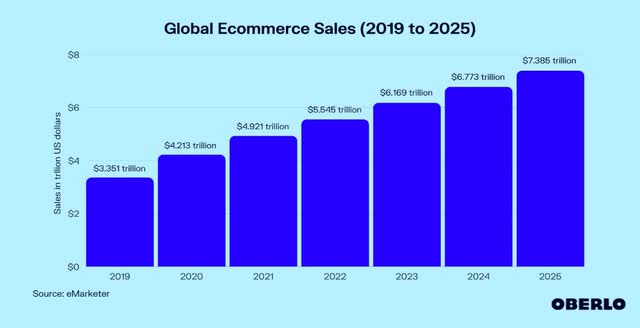

Trying ahead, I see each as effectively poised to learn from the secular pattern of e-commerce penetration. Once we are so used to the American means of on-line buying, it is simple to type the impression that e-commerce has already saturated. The fact is that the worldwide e-commerce penetration remains to be ONLY at about 20% presently. That means 80% of the commerce remains to be presently carried out offline. When it comes to absolute quantity, as you’ll be able to see from the next chart, international retail e-commerce gross sales have reached $4.2 trillion in 2020. And it is projected to nearly double by 2026, reaching $7.4 trillion of revenues within the retail e-commerce enterprise. The e-commerce motion is simply getting began and the majority of the expansion alternative is but to return. And leaders like BABA and AMZN are each greatest poised to capitalize on this secular pattern.

OBERLO knowledge

I additionally see each get pleasure from super progress alternatives in different areas in addition to e-commerce. Each are leaders within the cloud computing area, particularly in their very own geographical areas. This section has super progress potential because the world shifts to the pure “pay per use” mannequin, and the expansion is simply beginning as start-ups, enterprises, authorities companies, and tutorial establishments shift their computing must this new mannequin. In BABA’s case, its cloud computing, worldwide avenues, and home platform enlargement are all having fun with momentum. These segments all present promise for profitability and progress within the close to future to keep up their excessive R&D yield and excessive ROCE. Equally, AMZN’s AWS unit is predicted to develop considerably within the close to future to assist elevate the underside line. It has not too long ago introduced choices equivalent to Cloud WAN, a managed vast space community, and Amplify Studio, a brand new visible improvement surroundings. Furthermore, AMZN’s additionally introduced the deliberate $8.45 billion buy of MGM Film Studios, and I am optimistic concerning the synergies with its streaming companies.

Additionally, I do see some uneven progress alternatives for BABA. As aforementioned, each shares are greatest poised to capitalize on the world’s unstoppable shift towards e-commerce. Nonetheless, the remaining shift can be inconsistently distributed and the Asian-Pacific area would be the heart of the momentum. As proven within the chart above, world retail e-commerce gross sales are anticipated to exceed $7.3 trillion by 2025. The twist is that the Asian-Pacific area can be the place many of the progress can be. By 2023, the Western continents will contribute 16% of the overall B2B e-commerce quantity, whereas the remaining 84% would come from the non-Western world. And BABA is greatest poised to learn with its scale and attain, authorities help, and cultural and geographic proximity.

Lastly, the next desk summarizes all the important thing metrics mentioned above. As talked about early on, my thesis is that the dangers surrounding BABA have been absolutely priced in already. Even when we put apart the difficulty of valuations and dangers, there are a lot of comparable points between these two e-commerce giants (in all probability greater than their variations). Evaluating and contrasting their R&D efforts, profitability, and future progress areas not solely elucidate their very own funding prospects but additionally present perception into different e-commerce funding alternatives.

Writer

Dangers

I don’t assume there’s a have to repeat BABA’s dangers anymore. Different SA authors have offered glorious protection already. And we ourselves have additionally assessed these dangers primarily based on a Kelly evaluation.

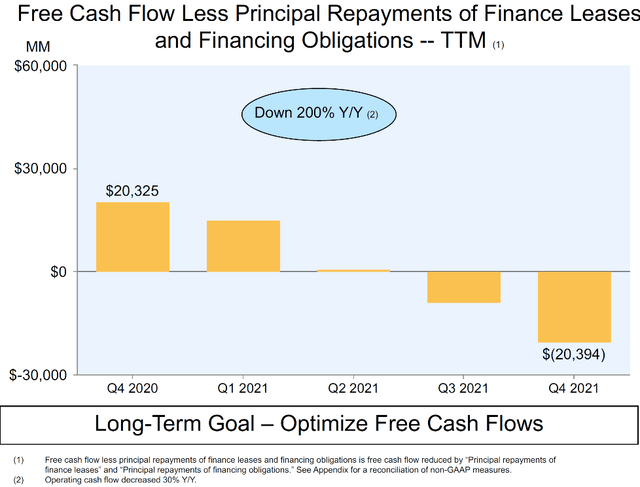

For AMZN, a key difficulty I like to recommend traders to maintain an in depth on within the upcoming earnings launch is the leasing accounting. We’ve got cautioned readers earlier than the 2021 This fall earnings launch concerning the function of its lease accounting and the potential of its free money movement (“FCF”) deterioration after being adjusted for leasing accounting. And as you’ll be able to see from the next chart, sadly, its FCF has certainly suffered a dramatic deterioration to a adverse $20B in 2021 This fall. Within the incoming 2022 Q1 launch, it is a key merchandise that I’d be watching.

AMZN 2021 This fall earnings launch

Abstract and closing ideas

The inventory market is infamous for fully ignoring enterprise fundamentals each on the greed excessive and on the worry excessive. The stark distinction between BABA and AMZN serves as a common instance of such market psychology so traders may establish mispricing alternatives.

The thesis is that BABA is now within the excessive worry finish of the spectrum and its inventory worth has not too long ago turn into disconnected from fundamentals. Particularly,

- The present market valuation has already priced in all of the dangers surrounding BABA. BABA’s worth to gross sales ratio is discounted by nearly half relative to AMZN regardless of its greater margin and profitability.

- Each shares pursue new alternatives aggressively with 10% to 12% of their complete gross sales spent on R&D efforts, however BABA enjoys a much better yield.

- I additionally see each effectively poised to learn from the secular pattern of world e-commerce penetration and likewise from the alternatives in different areas equivalent to cloud computing. Nonetheless, I do see some asymmetries right here. For instance, the remaining e-commerce shift can be inconsistently distributed and the Asian-Pacific area would be the heart of the momentum, the place BABA is best positioned to learn from its authorities help and cultural/geographic proximity.

")

{kind=link}