XiXinXing

Co-produced with “Hidden Opportunities.”

If you have been following the financial markets closely, 2022 has not exactly been a year most investors can speak positively of. All three of the major averages suffered their worst year since 2008, and the market participants have been quite fearful about the prospects of the economy.

Some people see a glass of water as half-empty. Some pessimists even think the glass is filled with arsenic. I’m not in either of those groups. Count me among those who always see a glass of water as half-full. I’ll admit it is not easy being optimistic with the current stock market environment. My portfolio picks have experienced a decline in value. However, I’m encouraged when I review the operating fundamentals of my securities and focus on my long-term objectives.

As an income investor, I aim to build an income stream that can sustain my living expenses plus a little extra to allow me to add to my portfolio. I am focused on the long term and am not too worried about the interest rates at the end of 2023. I am adopting one of Peter Lynch’s golden rules for investing:

Nobody can predict interest rates, the future direction of the economy, or the stock market. Dismiss all such forecasts & concentrate on what’s actually happening to the companies in which you’ve invested. – Peter Lynch, Former Fund Manager at Fidelity.

I am using the bear market fear to further my financial independence. Here are two picks with +7% yields from recession-resistant sectors that will let you get paid to wait for a market recovery.

Pick #1: UTF – Yield 7.2%

In a fragile economy with an increased likelihood of a recession, we should focus on sectors where significant investment will be flowing in for the foreseeable future. The Biden Administration’s infrastructure law from late 2021 will be a substantial source of dollars being pumped into vital sectors of the nation’s lifelines. Source.

whitehouse.gov

The federal government is spending a great deal of money on infrastructure, and secular trends such as digitalization and decarbonization will continue to drive the need for new investments, making this a very attractive sector. State and local governments are currently allocating funds to improve local infrastructure, as seen from these recent road improvement projects in Kentucky and water projects in New York.

Infrastructure is an asset-rich industry with tremendous competitive advantage and decades of unencumbered monetization potential. Warren Buffett’s Berkshire Hathaway (BRK.A, BRK.B) generates around 15% of its profits from a diversified portfolio of infrastructure assets.

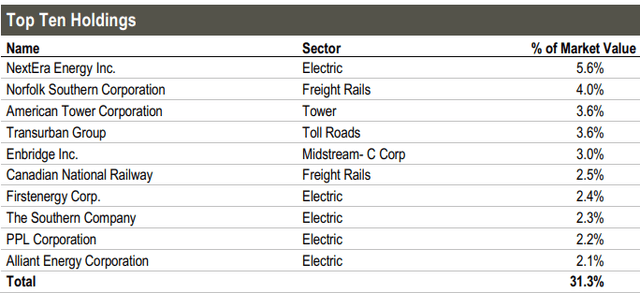

I want my own mini infrastructure and utility conglomerate to pay me big dividends from the nation’s vital assets enabling connectivity, trade, and commerce. Cohen & Steers Infrastructure Fund (UTF) fits my needs well by providing me with the means to invest in the infrastructure and utility sectors. The closed-end fund (CEF) portfolio comprises some of America’s most prominent utility, railroad, toll road, and energy pipeline companies.

cohenandsteers.com

UTF is highly diversified across 242 holdings in its portfolio, with the electric utility, corporate bonds, and midstream MLPs constituting over 50% of the fund.

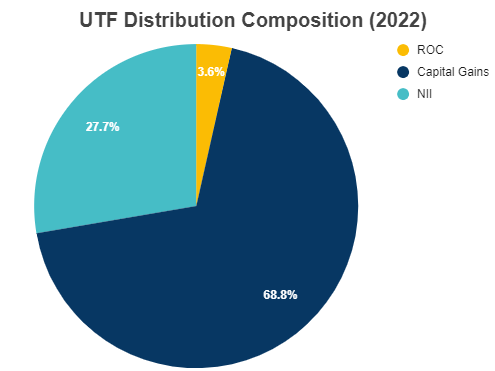

UTF’s steady $0.155 monthly distribution calculates to a 7.2% annualized yield. Looking at the CEF’s distribution breakdown in 2022, we see the most significant portions come from capital gains and Net Investment Income (“NII”).

Author’s calculations

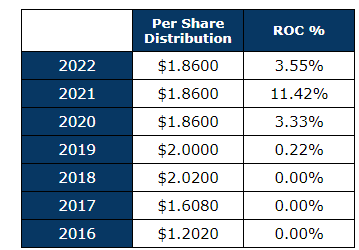

Notably, in the past seven years, the CEF’s Return of Capital (“ROC”) component has remained sparingly low, making it a suitable investment in retirement accounts.

Author’s calculations

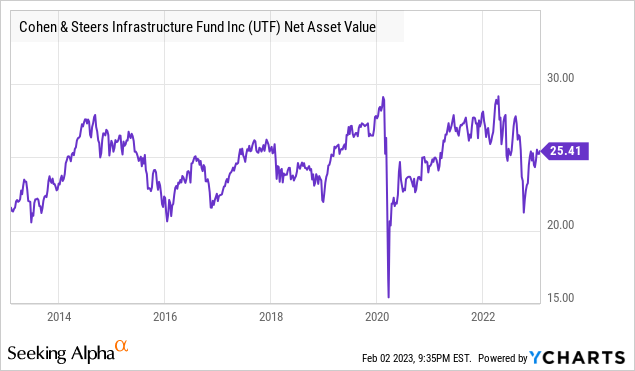

UTF has done an excellent job with steady NAV growth over the long term, making it a highly sustainable income investment when purchased at the right price.

UTF trades almost at par with NAV today, making it an attractive time to initiate/add to your infrastructure portfolio.

While consumer discretionary, technology, and other flashy sectors will struggle in a recession economy, boring old infrastructure will shine brightly in 2023 with billions of investment dollars flowing in. As such, the cash flows from underlying companies will be resilient to recession pressures. The 7.2% yielding UTF lets you collect your cut from America’s infrastructure modernization efforts.

Pick #2: EVA – Yield 7.8%

Wood biomass is an industry where money grows on trees. With leading economies targeting net zero carbon emissions, the heightened long-term focus remains to phase out coal, and wood pellets are an efficient and carbon-neutral alternative. The E.U. is expected to have imported 24.3 million metric tons of wood pellets in 2022. Homes in thousands of European cities and villages in Sweden, Denmark, Lithuania, Germany, France, Spain, and Italy are increasingly heated with wood chips from harvest residues.

Enviva Inc. (EVA) is the world’s largest producer of industrial wood pellets and a key supplier to the E.U. nations. The European Commission’s impact assessment for the amendment of the Renewable Energy Directive (REDIII) states that the use of bioenergy must increase by an average of 69% to meet climate targets, balance the grid, and decarbonize the maritime, aviation, and industrial sectors. The wood biomass industry is going to see continued growth in the upcoming decade.

Woody biomass is already one of the most regulated industries in the forestry and renewable energy sectors. EVA is certified by the SBP and has numerous other certifications with annual audits by leading independent agencies.

EVA November 2022 Investor Presentation

Investors must note that forest inventory in EVA’s sourcing area has grown by 21% since 2011. Regulations and politics aside, EVA continues to thrive as a business. The company recently announced a 10-year take-or-pay fuel supply contract with an existing E.U. customer (expandable for up to five years). As part of this agreement, EVA expects to supply 800,000 metric tons of industrial-grade wood pellets annually starting in 2027.

EVA’s total weighted average remaining term of take-or-pay off-take contracts is ~14 years, with a total contracted revenue backlog of over $23 billion. In addition, EVA’s customer sales pipeline exceeds $50 billion, including contracts in various negotiation stages. This is like the Tesla (TSLA) Cybertruck pre-orders – customers are ordering massive supply volumes from EVA for deliveries 5+ years out. One important difference: whether the customer takes the delivery or not, EVA gets paid!

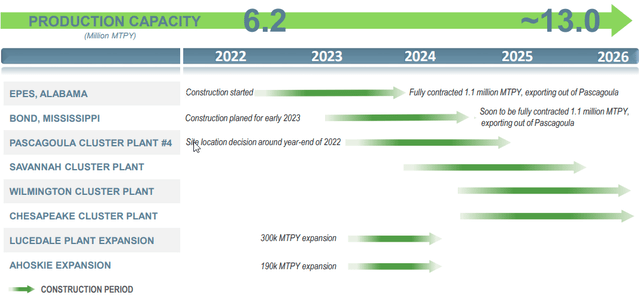

Additionally, EVA is boosting its production and projects 2026 capacity to be more than double from current levels. Source.

EVA November 2022 Investor Presentation

EVA has annual price escalators in its contracts, providing it a natural protection against long-term inflationary pressures. In Q3, the revenues were up 37% YoY due to these price escalators. During the quarter, EVA boasted a 326% higher YoY Adj. EBITDA and the company declared a 7.7% higher YoY dividend.

EVA is an excellent dividend steward, boasting seven straight years of payment growth. The company projects a 2023 dividend coverage by Distributable Cash Flow (“DCF”) of 1.1x and targets a 1.5x coverage by 2025. EVA’s current quarterly dividend calculates to a healthy 7.8% annualized yield.

Environmentalists and critics argue that the agencies certifying sustainability and biodiversity impacts have weakly defined metrics to base their decisions on. Isn’t this the case for all industries – pharmaceuticals and patient addiction, consumable goods and their effects on human health, automobiles and road safety, etc.? The wood pellet industry is growing, and with growth comes suspicion of misconduct, followed by increased scrutiny and regulation. What remains undisputed is the hard cash that EVA pays you every quarter, which you can spend at your discretion. 7.8% yields from this industry leader with a massive competitive advantage and recession-resistant business model.

Note: EVA is now structured as a corporation and no longer issues a K-1. Investors will receive a 1099. Their earnings report is expected ~March 1.

Shutterstock

Conclusion

Legendary investor Warren Buffett has always advised investors to buy fear and sell greed.

This does not bother Charlie [Munger] and me. Indeed, we enjoy such price declines if we have funds available to increase our positions. The best chance to deploy capital is when things are going down. – Warren Buffett.

We don’t know when the market will bottom. In fact, market bottoms are confirmed months after they have happened, and the skepticism and doubt-filled average investor is likely to miss the boat.

We like to get paid for all our steps in the financial markets. Whether it is to wait for the market to turn bullish or for a company to achieve its growth and profitability targets – we only own securities that pay us for our time (and money). With this mindset, we have no problem riding the roller coaster market while staying invested. At HDO, we are a net buyer of dividend-payers and are buying discounted yields with both hands. Two picks with +7% for you to grab before it is too late.

")

")

")

Q1 2025 Earnings Name Transcript")

{kind=link}