Editors’ observe: This column is a part of the Vox debate on the financial penalties of conflict.

Following the invasion of Ukraine, the sanctions taken towards Russia have been unprecedented in scale and, above all, in scope. For the primary time in current historical past, the overseas change reserves held by a significant central financial institution have been frozen. Reactions by Russian authorities present that this was completely sudden on their half (Berner et al. 2022). This column presents some preliminary ideas on the potential long-term and systemic penalties in a context of geopolitical rivalry and rising ‘deglobalisation’, no less than in respect to monetary transactions.

Sanctions and the greenback

A primary query to contemplate is whether or not the standing of the greenback because the dominant worldwide foreign money could possibly be put unsure or threat. Our reply is unfavorable for 3 causes.

- The freeze is going down in a state of affairs which may be perceived as actually distinctive: an armed battle triggered by the invasion carried out by a significant nation. Nobody would anticipate commonplace monetary relations and preparations to carry in these circumstances. In comparable conditions, comparable to Japan’s conflict in Asia from 1937, cross-border funds had been finally blocked. Gold owned by nations occupied or in conflict was not handed over to the aggressor by the central banks that held it. Thus, France and Britain refused handy over the reserves of the Baltic nations annexed by the Soviet Union in 1940. These are excessive and uncommon circumstances.

- All actions taken by the US authorities during the last a long time reveal their dedication to advertise and protect the greenback as a secure asset. Quite a few amenities have been deployed by the Federal Reserve to make sure the liquidity of the Treasury market – a few of them specifically designed for official overseas holders. The implicit authorities assure benefitting Fanny Mae and Freddie Mac (which function a significant instrument of overseas change reserves) has been reaffirmed when needed. With the doable exception of the Trump administration, successive US Treasury secretaries have been adamant that “a robust greenback is within the curiosity of america”.

- Lastly, engaging alternate options to the US greenback don’t exist and therefore no life like diversification instrument is out there. The facility of the US to impose sanctions derives immediately from the central position of the greenback. For any worldwide company or monetary establishment, life with out the greenback is at the moment inconceivable. Subsequently, any of their operation falls doubtlessly beneath US jurisdiction. All will stay beneath the attain of sanctions as long as the greenback stays important. Avoiding and resisting sanctions means discovering alternate options to the greenback. We’re subsequently drawn again to an outdated, and nonetheless very acute query: are there such alternate options?

Worldwide cash, outdated and new

Cash is about scale and externalities. They arrive in two kinds: community externalities – the extra individuals settle for a foreign money the higher it’s as a medium of change; and liquidity externalities – a real retailer of worth stays tradable and invaluable in instances of want (Brunnermeier et al. 2022). Within the present world economic system, an important query issues the causality between these two capabilities.

The dominant foreign money paradigm (Gopinath and Stein 2021) primarily attributes the essentiality of the greenback to its position in world funds and finance – emphasising the medium of change position and its operate as a automobile foreign money for worldwide monetary flows. In the identical vein, Eichengreen (2010), based mostly on his evaluation of historical past of the interwar interval, sees a logical sequencing within the emergence of a world foreign money: (1) invoicing and settling commerce, (2) use in non-public monetary transactions (automobile foreign money), (3) use by central banks as reserves.

If that sequence remains to be legitimate, there are actual prospects of other reserve currencies rising. China is the world’s main buying and selling energy. It has leverage to push for using its foreign money as a medium of change and unit of account. It may exploit its advance within the growth of digital currencies. A doable situation would see each Alipay and Tencent increase their worldwide operations, progressively shifting their denomination from native currencies to the renminbi. China is essentially the most superior in creating a central financial institution digital foreign money. The introduction of the e-yuan, already previous its pilot section, is commonly interpreted as an offensive transfer to advertise the RMB internationalisation.

One other, one way or the other reverse, method attributes the greenback dominance to its distinctive position as a retailer of worth, being the last word secure asset. There’s nowhere else to park a number of hundred billion with nearly complete safety and liquidity. That operate is central in a financially globalised world the place each non-public and public entities should shield their liquidity. From that position as a retailer of worth, different capabilities derive, reversing the causality which will have prevailed in different intervals. As a result of it’s a reserve asset, it’s handy to additionally use the greenback for invoicing and funds. It serves as a world unit of account. Considerably, even China abroad lending by official entities remains to be 70% denominated in {dollars} and solely 10% in renminbi.

If, as we predict, that second method is appropriate, no different cash is positioned to dislodge the greenback within the foreseeable future. Being a reserve foreign money definitely brings privileges and energy. It’s also very demanding. Two main necessities should be met, which no different nation can do: a big and liquid Treasury bond market (which Europe doesn’t at the moment have) and a totally and unconditionally open capital account (which China is not going to have). Localised swap and barter agreements, comparable to developed by China, may help however is not going to dispense of these two fundamental necessities. (A columnist lately remarked {that a} credit score line in renminbi is financially equal to being fluent in Esperanto).

A fast have a look at different doable talked about alternate options confirms that prognosis:

- Currencies such because the Australian greenback are talked about as doable reserve devices.1 Whereas absolutely open and accessible, the dimensions of the Australian Treasury Bond market is barely 2.5% of the US.

- There have been recurrent makes an attempt to make the Particular Drawing Rights into a real various to reserves – a course actively promoted by China within the aftermath of the International Disaster (Zhou 2009). They’ve largely stalled, for causes of measurement and accessibility (the doable use of Particular Drawing Rights is intently restricted by design).

- Some observers stress the potentialities of cryptocurrencies, pointing to their position to channel funds to Ukraine after the Russian invasion (Danielsson 2022). Nevertheless, they don’t have any capability to course of transactions on a big scale (day by day quantities talked about in relation with Ukraine are within the tens of tens of millions of {dollars}). Regardless of some fascinating technological options, cryptocurrencies are even farther from having any important position as reserves. Managers are conscious of the peculiarities of those cash programs. Their day-to-day functioning depends on the initiatives and incentives of personal operators, whose exercise is only voluntary and profit-motivated. It’s uncertain that they’d entrust public reserves to teams of ‘miners’ scattered everywhere in the world, with a non-negligible proportion having migrated to Kazakhstan after having been prohibited to function in China.

Globalisation and the demand for reserves

Sanctions should have important longer-term results – not on the composition, however on the demand for reserves. The worldwide financial system could finally modify by transferring to a brand new structure, the place monetary integration is decreased and, consequently, the necessity for reserves is smaller.

Leaving apart the reciprocal relation between the US and China – famously certified by Larry Summers as a “monetary steadiness of terror” – it’s helpful to contemplate the state of affairs

of different rising nations. Round twenty nations have overseas change reserves above $100 billion, most of them rising economies. Borrowing from the finance and local weather literature, these nations clearly face a brand new ‘tail threat’ of sanctions, with a really low likelihood however very excessive influence. The identical local weather literature tells us that one can’t diversify towards these dangers. The one method to purchase insurance coverage is to cut back one’s publicity. In local weather, it means bringing down CO2 emissions and concentrations to low ranges. For rising economies, it means lowering the necessity for (and dependence upon) overseas change reserves.

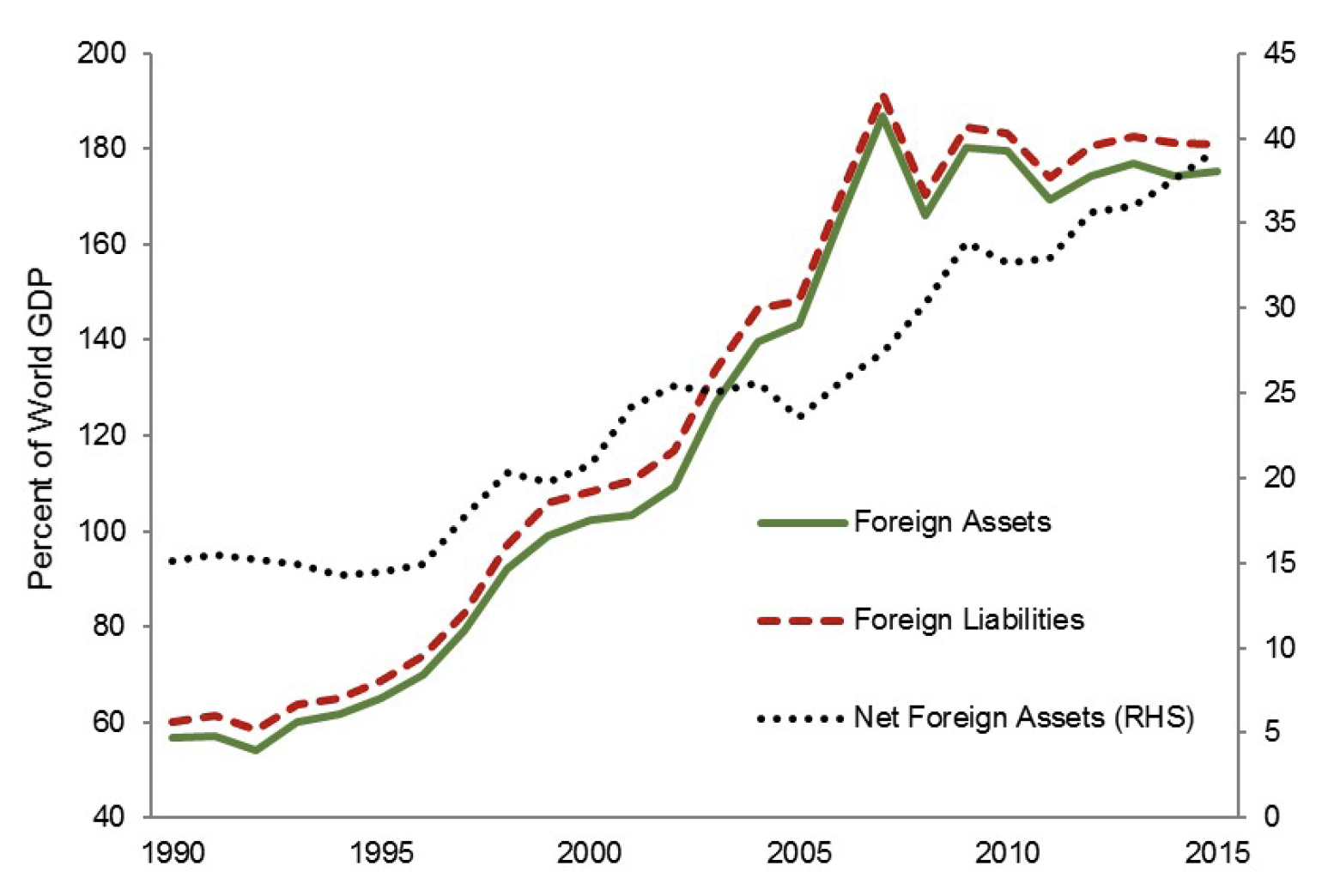

There was a continuing improve in overseas change reserves till 2015 and a plateauing since then. That evolution nearly mirrors (with a lag of some years) the tendencies in gross cross-border capital flows and worldwide exposures, which expanded till 2010 after which stabilised as a consequence of the International Disaster.

Determine 1

a) International change reserves

Supply: ECB Financial Bulletin subject 7/2019.

b) Gross worldwide property and liabilities

Supply: Adler and Garcia-Macia (2018).

This isn’t a coincidence. Apart from China, nations’ demand for reserves is a direct results of their monetary integration with the world. Reserves are historically seen as a software for change charge administration. However they play a broader position. In lots of rising economies, the productive and monetary sector is partially ‘dollarised’. As a consequence of capital account liberalisation, each company and monetary establishments are in a position to borrow and lend in overseas foreign money. Consequently, they might be dealing with maturity and liquidity mismatch in {dollars}. International reserves permit central banks in these nations to behave as lenders of final resort in overseas foreign money and shield home, in addition to exterior, monetary stability. That is the basic purpose why reserves have, over the 2 final a long time, expanded to ranges which are inconceivable to clarify and rationalise by conventional metrics of commerce and monetary openness.

These coverage decisions could be reversed if and when reserves are carrying new dangers. Monetary globalisation had primarily come to a halt effectively earlier than the invasion of Ukraine.

New types of sanctions, even when very uncommon, could result in an additional retreat and segmentation of the world monetary system (Harding 2022).

In the end, sanctions, and their implications, reveal a fundamental, and forgotten, fact: the motion in the direction of better monetary globalisation has been underpinned by a long-term commonality of functions, requirements and understanding between nations. By supplying a reserve foreign money (and benefiting from it), by augmenting it in disaster moments comparable to 2008 or 2020 by swap traces, the US has supplied the world with a world public good (Wolf 2022): widespread entry to a secure asset, which can be utilized as a buffer towards monetary shocks. Whether or not that equilibrium could be preserved in a geopolitically divided world is a significant query for the long run.

References

Adler, G and D Garcia-Macia (2018), “The Stabilizing Function of Internet International Asset Returns”, IMF Working Paper WP/18/79.

Berner, R, S Cecchetti and Okay Schoenholtz (2022), “Russian sanctions: Some questions and solutions”, VoxEU.org, 21 March.

Brunnermeier, M, S Merkel and Y Sannikov (2021), “Debt as Secure Asset”, NBER Working Paper 29626.

Danielsson, J (2022), “Crypto currencies and the conflict in Ukraine”, VoxEU.org, 11 March.

Eichengreen, B (2010), “The renminbi as a global foreign money”, coverage paper.

Gopinath, G and J C Stein (2021), “Banking, Commerce, and the Making of a Dominant Forex”, The Quarterly Journal of Economics 136(2): 783-830.

Harding, R (2022) “Toppling the greenback as reserve foreign money dangers dangerous fragmentation”, Monetary Instances, 10 March.

Landau, J P (2021), “Worldwide Forex Competitors: the Digital Dimension”, Markus Academy.

Wheatley, J and C Smith (2022), “Russia sanctions threaten to erode dominance of US greenback, says IMF”, Monetary Instances, 31 March.

Wolf, M (2022), “A brand new world of foreign money dysfunction looms”, Monetary Instances, 29 March.

Zhou, X (2009), “Reform the worldwide financial system”, BIS Overview 41/2009.

Endnotes

1 Gita Gopinath quoted within the Monetary Instances (2022).

{kind=link}