A fast notice on tariffs: Over the previous few weeks, I’ve been placing collectively my quarterly name for shoppers. The problem is the right way to body the present financial state of affairs in a manner that’s helpful and informative and never the same old run-of-the-mill noise.

It’s straightforward to get distracted by the chaos of random insurance policies which were coming rapid-fire at People. We see this within the Tariffs On, Tariffs Off, Promote, Purchase sample of news-flow. However slightly than get pushed and pulled by the day by day deluge, let’s discover some higher context.

Markets are attempting to digest a troika of unknowns:

1) What are the brand new proposals truly going to be?

2) What is going to their impression be on financial exercise and inflation?

3) How will the above have an effect on company revenues and income?

That is what markets do: They suss out the complexities of occasions and calculate the likelihood of how they may impression future money flows.

~~~

The tariff construction that exists at this time was based mostly on agreements from the Uruguay Spherical that established the World Commerce Group. Recognizing the rising significance of mental property and the companies economic system, the U.S. wished to verify three of America’s largest and fastest-growing company segments had commerce protections: Finance, Expertise, and Leisure.

The Washington Put up mentioned why the WTO was an enormous win for the US:

“These have been large wins for Hollywood, Silicon Valley and Wall Avenue, and introduced order to a kind of commerce that the U.S. dominated. Whereas the U.S. has run a deficit in its merchandise commerce since 1975, it has constantly offered extra companies to the remainder of the world than it has imported. The U.S. final yr exported greater than $1 trillion value of companies, having fun with an almost $300 billion commerce surplus.”

The broad incentives of low-cost labor and minimal regulatory oversight led Company America to shift a lot of its manufacturing abroad. In hindsight, maybe an excessive amount of. As we discovered in the course of the pandemic, this created vital nationwide safety dangers.

The final administration took some steps to right this, and I give this administration the advantage of the doubt in making an attempt to do the identical – particularly in the case of China.

However the chaos of the way in which that is being carried out, and the tossing apart of a broad general technique developed over many years, has been giving Mr. Market suits. He often does an amazing job sniffing out new developments earlier than most of us understand it.

Any interpretation I attempt is extra artwork than science, so take this with a grain of salt. However the way in which this sell-off feels, and particularly how sentiment measures from shoppers and CFOs are working on future spending plans and CapEx plans, implies the market fears one thing depraved this manner comes.

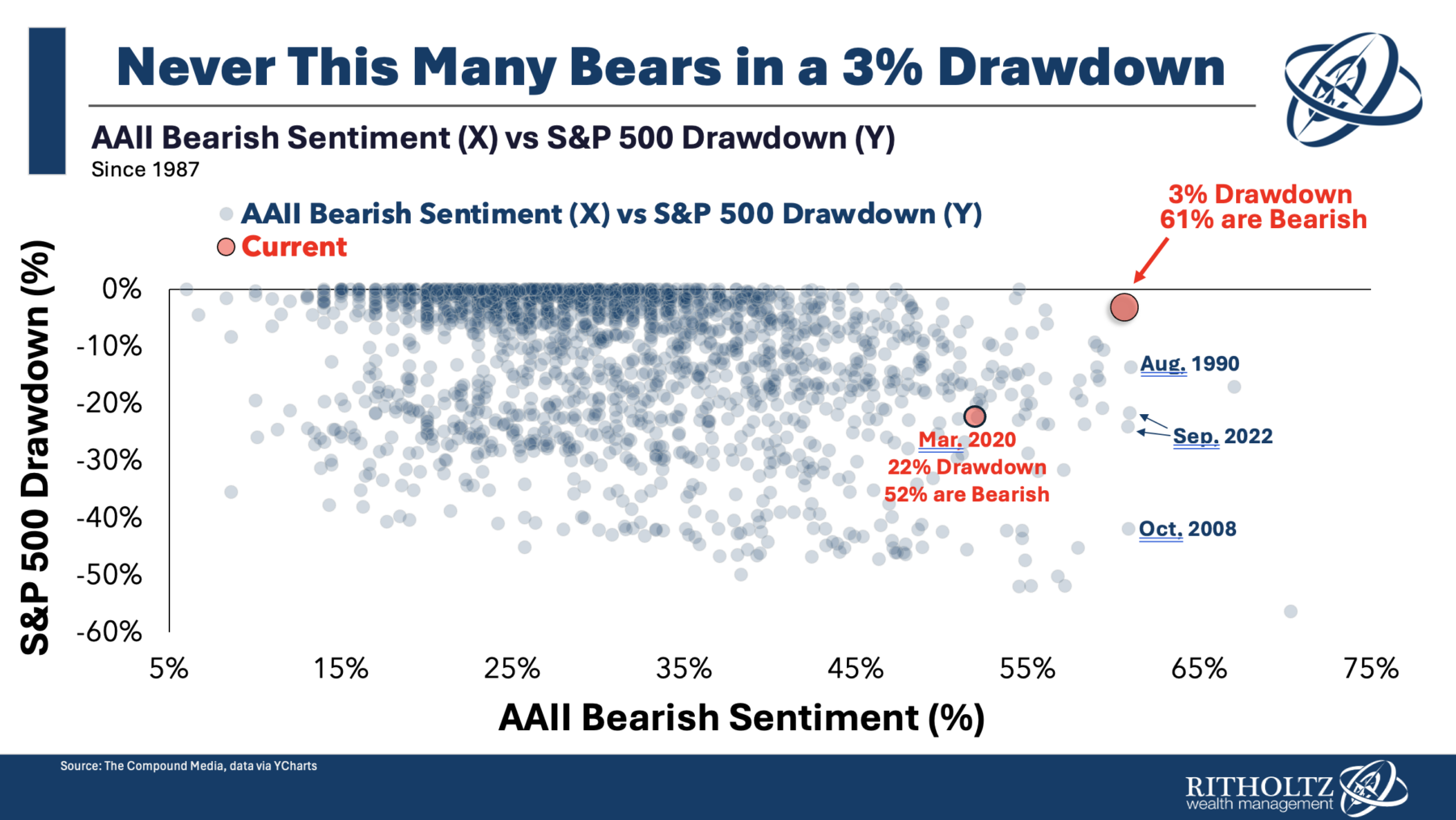

This grew to become obvious within the first 3% drop off of all-time highs:

Sentiment this excessive advised this was greater than a runoff-the-mill selloff. I didn’t perceive this as representing a big menace to the established financial order. Because the chart at prime implies, it seems that the financial adjustments aren’t a one-time adjustment however a everlasting tax on consumption.

In a phrase, the U.S. tariff implementation appears to be shifting in the direction of the equal of a nationwide VAT tax.

Hey, I perceive that tariffs aren’t the equal of a nationwide VAT tax. It’s not the identical factor in idea, however in apply, particularly with the chatter of lowering earnings taxes, it feels that manner: European consumption tax minus the common well being care, schooling, and retirement advantages.

I hope this take is improper. I perceive that any VAT or gross sales tax is agnostic as to put of manufacturing, whereas tariffs aren’t. It’s not an ideal metaphor, however the parallels between a consumption tax versus an earnings tax are there.

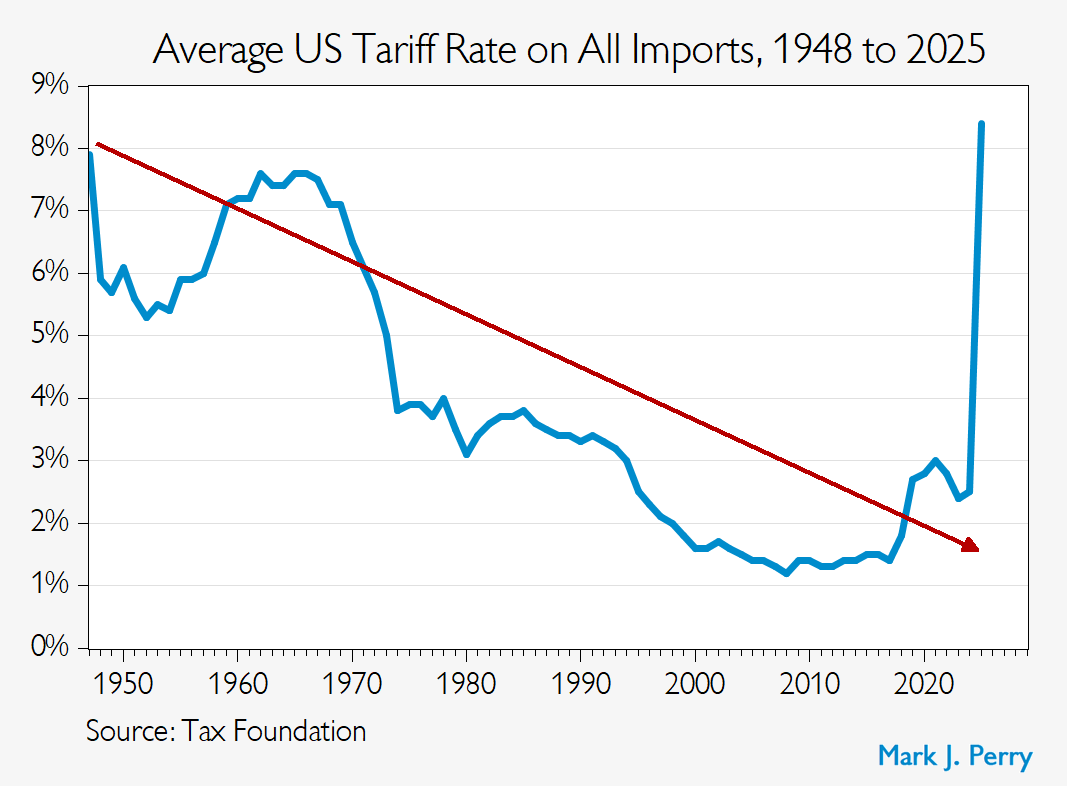

The market response appears to be anticipating one thing greater than reciprocal tariffs. Or as Mark Perry‘s chart under reveals, the brand new proposal is an excessive post-war historic anomaly:

We’ll get a greater sense of precise tariffs Wednesday; for higher or worse, markets will continues incorporating these new VAT-like consumption Taxes into costs as we transfer ahead.

Beforehand:

7 Rising Chances of Error (February 24, 2025)

Tune Out the Noise (February 20, 2025)

{kind=link}