CEOs are paid exorbitant amounts of money and therefore expected to execute flawlessly. When external factors affect a company, we expect management to be transparent and use their industry expertise to navigate investors through tough times. When guidance gets adjusted three times in a row (cough, cough Planet Labs) it shows that management is detached from operations. This breeds distrust among investors.

When we invest in companies, we trust what management says until they give us a reason not to. After all, if management has a history of incompetency, we wouldn’t have invested to begin with. That’s why today’s article will focus on what SolarEdge (SEDG) management is telling the markets about their current situation. With negative gross margins and revenues all but disappearing, we need to understand how bad the situation is and how management plans to guide the company through severe times of turmoil. Only then can we decide if it’s time to add shares, hold and pray, or bail entirely.

Surviving, Not Thriving

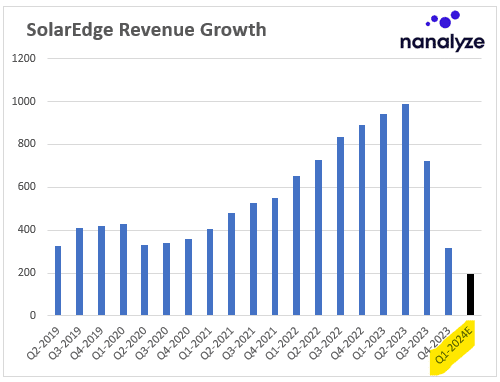

Let’s rehash the problem. SolarEdge was growing like mad selling solar hardware when things took a turn for the worse as high interest rates threw a monkey wrench into solar projects. As demand for solar hardware fell off a cliff across the globe, revenues for solar hardware manufacturers plummeted with geographical diversification not providing any benefits. Below you can see just how dramatic the drop has been for SolarEdge (Q1-2024 estimates in black).

is making ready to report Q2 outcomes. Right here’s what to anticipate")

experiences greater Q1 2025 gross sales and revenue")

")

")

{kind=link}