yullz/iStock Editorial through Getty Pictures

The timing was not taking part in in our favor, however we’re believers within the development companies for the time forward. Right here on the Mare Proof Lab Towers, we reiterate our optimistic view and our purchase scores for each LafargeHolcim (HCMLF, OTCPK:HCMLY) and for HeidelbergCement (HLBZF, OTCPK:HDELY).

As a quick recap, our key takeaways for Holcim have been:

- Greater authorities spending on infrastructure plans to revitalise enterprise after the pandemic;

- We see Holcim as a pacesetter within the ESG atmosphere;

- Supportive M&A;

- And robust monetary efficiency.

Trying on the firm’s efficiency and the inventory worth appreciation, we couldn’t be extra comfortable. We bought it proper for all of the above factors and we affirm our thesis.

Q1 Outcomes

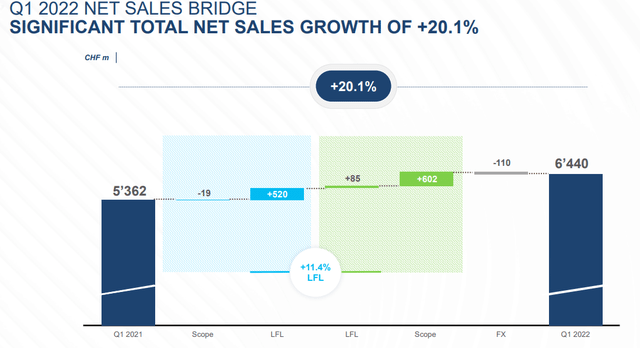

Beginning with level 4, Holcim reported report top-line income at CHF 6,440m, posting a plus +20.1%. This was pushed by sturdy demand, supportive acquisitions (level three), and pricing energy. Taking place on the P&L, the corporate posted one other report efficiency on the working revenue degree with a Q1 that posted CHF 614m with a complete development of +16.3% at CET. As soon as once more, a robust contribution was because of the newest acquisition, in our newest article on Holcim, we emphasised the a number of arbitrage alternative because of Firestone. Certainly, the roofing enterprise contribution was at a 17% working revenue margin.

Holcim gross sales pattern (Q1 Outcomes)

Our Factors Two and Three

An image paints a thousand phrases and we will use some to see what Holcim is doing. Jan Jenisch Holcim’s CEO stated: “With sustainability on the core of our technique, we revealed our first Local weather Report, sharing our net-zero journey with 2030 and 2050 targets validated by the Science-Primarily based Targets initiative. A primary in our business, it evaluations our decarbonisation actions, from inexperienced constructing options, all the best way to round development and next-generation applied sciences.”

ECOPact inexperienced concrete reached 10% of ready-mix gross sales in March 2022. Holcim is just not solely working on the ESG degree on net-zero emission, however it additionally making the most of the beneficial EU laws within the inexperienced bond space (with extraordinarily low-interest charges).

Holcim ESG (Q1 Outcomes)

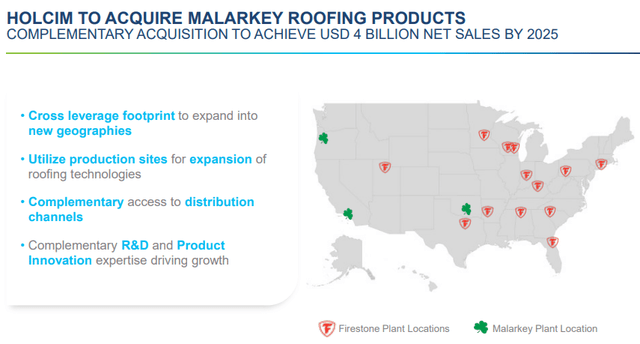

Relating to the acquisition, we see Holcim as a real worth participant. Malarkey is a confirmed development driver and may be very complementary to the Firestone acquisition. Accretive EPS ranging from this yr, synergies of $40 million by yr three, and a greater gross sales diversification.

Malarkey M&A particulars (acquisition presentation)

Conclusion and Valuation

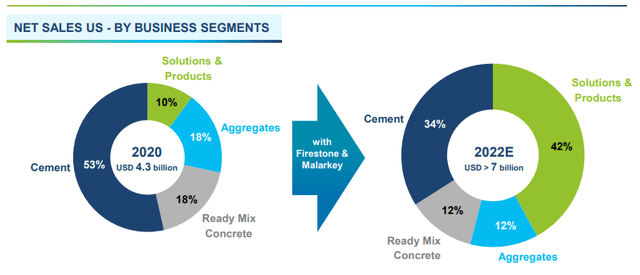

Regardless of the current macro growth, Holcim as soon as once more raised the bar on 2022 steerage and we’re assured that they are going to meet their inner outlook. Our inner crew is forecasting an EBITDA of seven billion CHF because of a greater product combine, the newest acquisition, and robust pricing energy. We actually like companies that are adaptive and Holcim is definitely considered one of them. From a pure participant in cement, aggregates, and concrete, they’ve determined to shift to extra value-added merchandise (picture beneath). We worth the corporate based mostly on our forecast EBITDA of 6.5x and we arrive at a valuation of 67 CHF per share, implying a present upside of greater than 42%. Other than the standard dangers within the development enterprise sector, we might like our readers to contemplate the Syria litigation.

Holcim enterprise transformation (Malarkey acquisition presentation)

Earlier protection within the development/cement sector:

- LafargeHolcim: A number of Arbitrage Thanks To Firestone Acquisition

- HeidelbergCement: The Finest Is But To Come

- Trying At HeidelbergCement’s Russian Publicity

")

")

")

{kind=link}