Published on January 10th, 2023 by Aristofanis Papadatos

Oil and gas royalty trusts came under extreme pressure in 2020 due to the coronavirus crisis and the resultant collapse of the prices of oil and gas. They all reduced their distributions sharply and some of them suspended their distributions for several months. However, as the energy market recovered from the pandemic in 2021, these trusts began to recover. Even better for them, the invasion of Russia in Ukraine and the resultant sanctions of western countries on Russia triggered a steep rally in the prices of oil and gas in 2022. As a result, oil and gas trusts are now offering exceptionally high distributions to their unitholders, resulting in much higher yields than the 1.6% dividend yield of the S&P 500.

We have created a spreadsheet of high dividend stocks with dividend yields of 5% or more…

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will discuss the prospects of the 9 highest-yielding royalty trusts.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

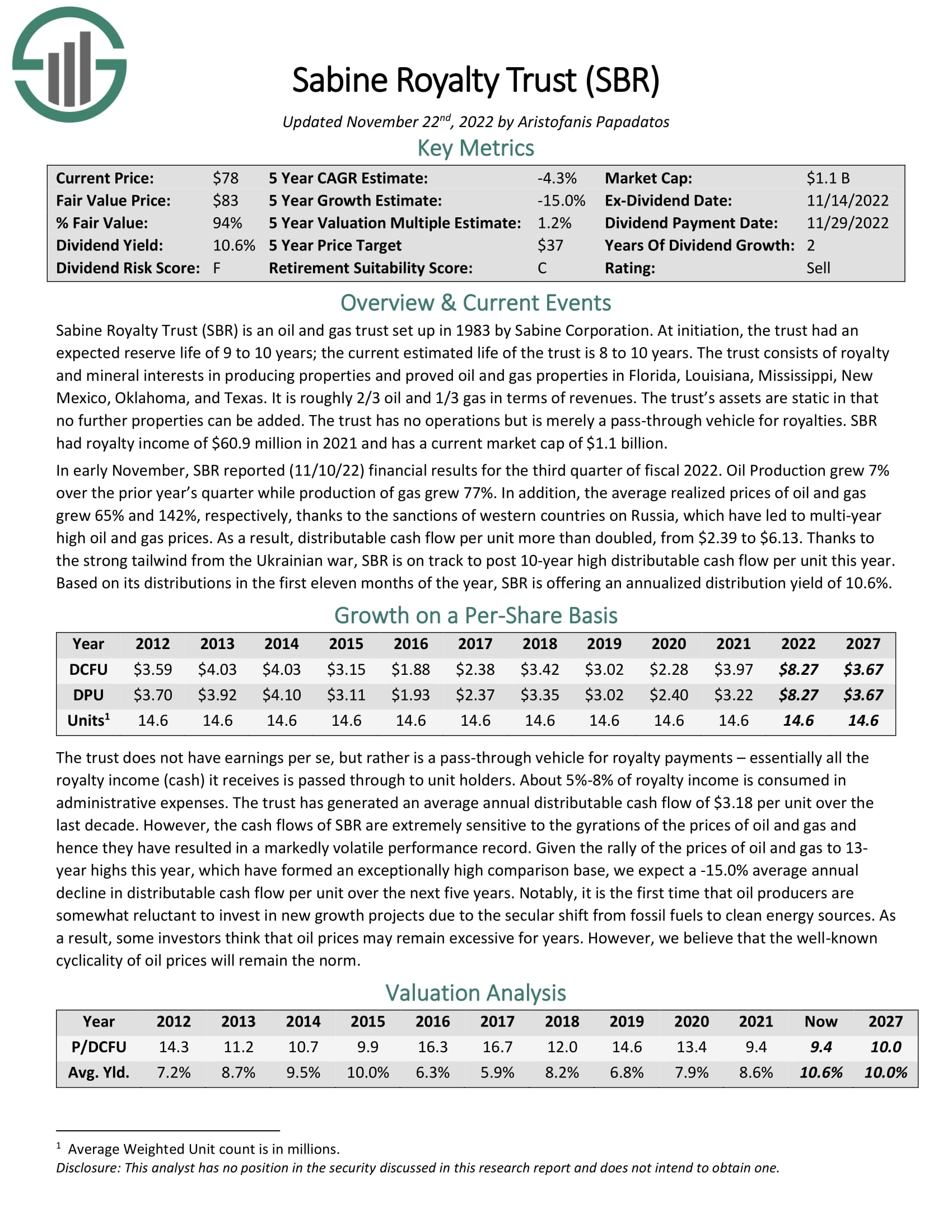

High-Yield Royalty Trust No. 9: Sabine Royalty Trust (SBR)

Sabine Royalty Trust is an oil and gas trust that was formed in 1983 by Sabine Corporation. It consists of royalty and mineral interests in producing properties and proved oil and gas properties in Florida, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas. It generates approximately two-thirds of its revenues from oil and one-third of its revenues from gas. The trust has static assets, i.e., it cannot add new properties to its asset portfolio. Sabine Royalty Trust has no operations but is merely a pass-through vehicle for royalties.

Just like every oil and gas trust, Sabine Royalty Trust has greatly benefited from the sanctions of the U.S. and Europe on Russia in response to its invasion in Ukraine. Before the sanctions, Russia was producing about 10% of global oil output and one-third of natural gas consumed in Europe. Due to the sanctions, the global oil and gas markets became extremely tight and thus the prices of oil and gas skyrocketed to 13-year highs last year.

The benefit from the rally of commodity prices was clearly reflected in the results of Sabine Royalty Trust. The trust offered an all-time high distribution per unit of $8.65 in 2022, more than double the previous 10-year high distribution per unit of $4.03. Although the stock has rallied to new all-time highs, it is offering an exceptionally high distribution yield of 10.5%.

However, investors should be aware that royalty trusts offer a different distribution every month, which is determined mostly by the prevailing prices of oil and gas and the actual production level of the trusts. As the energy sector is infamous for its cyclicality, it is reasonable to expect the distributions of Sabine Royalty Trust to moderate in the upcoming years.

Moreover, due to the global energy crisis caused by the rally of oil and gas prices last year, most countries are ramping up their efforts to shift from fossil fuels to clean energy sources. As a result, there is a record number of renewable energy projects under development right now. When all these projects come online, in 2-5 years, they will take their toll on the global consumption of oil and gas and thus they will hurt the results of oil and gas trusts.

Furthermore, all the oil and gas trusts face a strong secular headwind, namely the natural decline of their producing wells. Due to this decline, their production is expected to decrease in the long run. Sabine Royalty Trust has proved superior in this aspect. When it was set up, 40 years ago, it was expected to have a life of 8-10 years. However, it is still producing meaningful volumes and is expected to remain in life for more than a decade.

Click here to download our most recent Sure Analysis report on Sabine Royalty Trust (SBR) (preview of page 1 of 3 shown below):

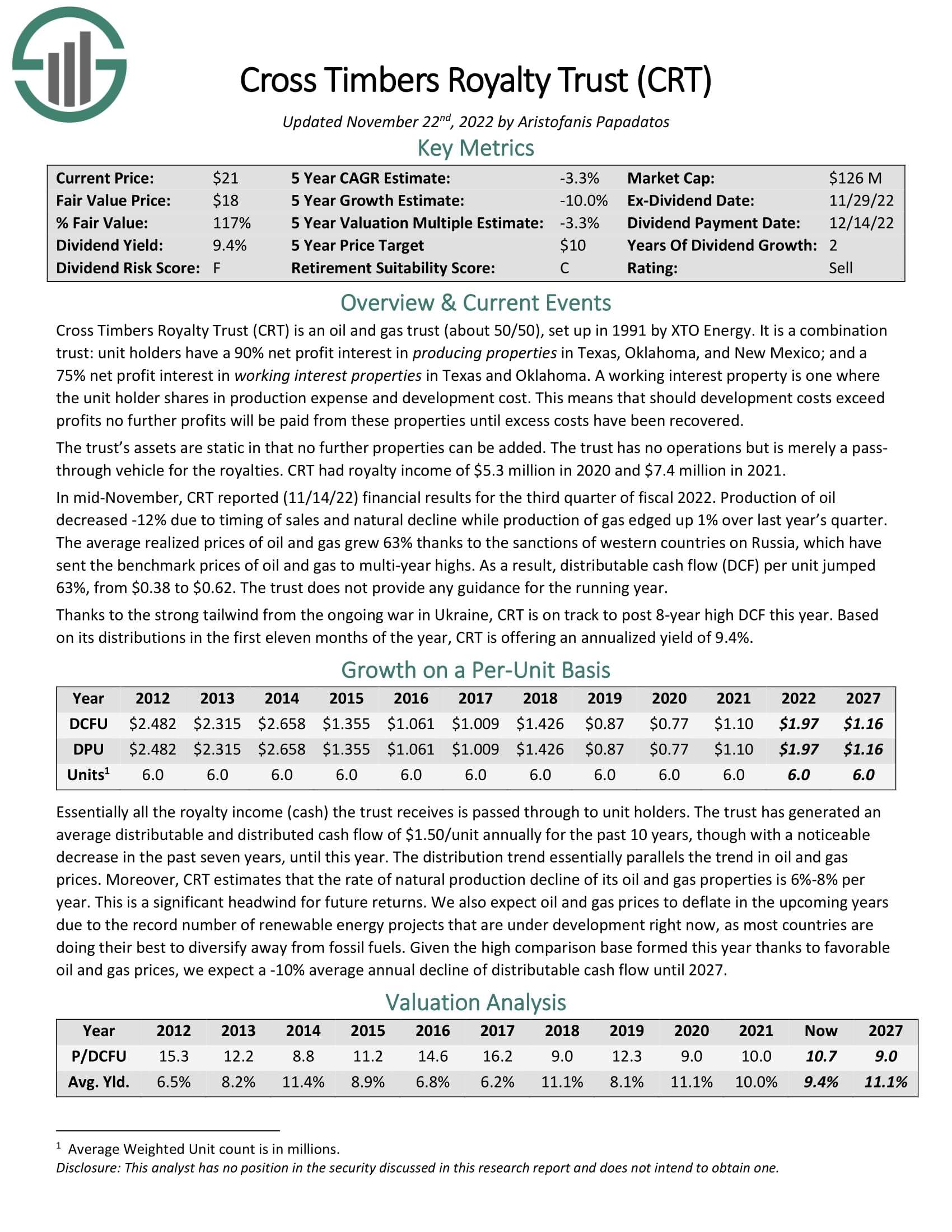

High-Yield Royalty Trust No. 8: Cross Timbers Royalty Trust (CRT)

Cross Timbers Royalty Trust is an oil and gas trust (about 50/50), set up in 1991 by XTO Energy. Its unitholders have a 90% net profit interest in producing properties in Texas, Oklahoma, and New Mexico; and a 75% net profit interest in working interest properties in Texas and Oklahoma. A working interest property is one where the unitholder shares in production expense and development cost. This means that the trust does not offer any distributions to its unitholders when its development costs exceed its revenues.

Thanks to the strong tailwind from the ongoing war in Ukraine, Cross Timbers Royalty Trust offered an 8-year high distribution per unit of $1.96 in 2022. This distribution corresponds to a yield of 8.2%. While this distribution yield is much greater than the 1.6% yield of the S&P 500, it is in line with the historical yields of this trust. Cross Timbers Royalty Trust has offered an 8.8% average distribution yield over the last decade.

On the other hand, the trust significantly reduced its distributions between 2014 and 2021 due to unfavorable oil and gas prices and the natural decline of its producing wells. Cross Timbers Royalty Trust estimates that the rate of natural production decline of its oil and gas properties is 6%-8% per year. This is a significant headwind for future returns. We also expect oil and gas prices to deflate in the upcoming years due to the record number of renewable energy projects that are under development right now. As a result, we expect the distributions of Cross Timbers Royalty Trust to decrease significantly in the upcoming years.

Click here to download our most recent Sure Analysis report on Cross Timbers Royalty Trust (CRT) (preview of page 1 of 3 shown below):

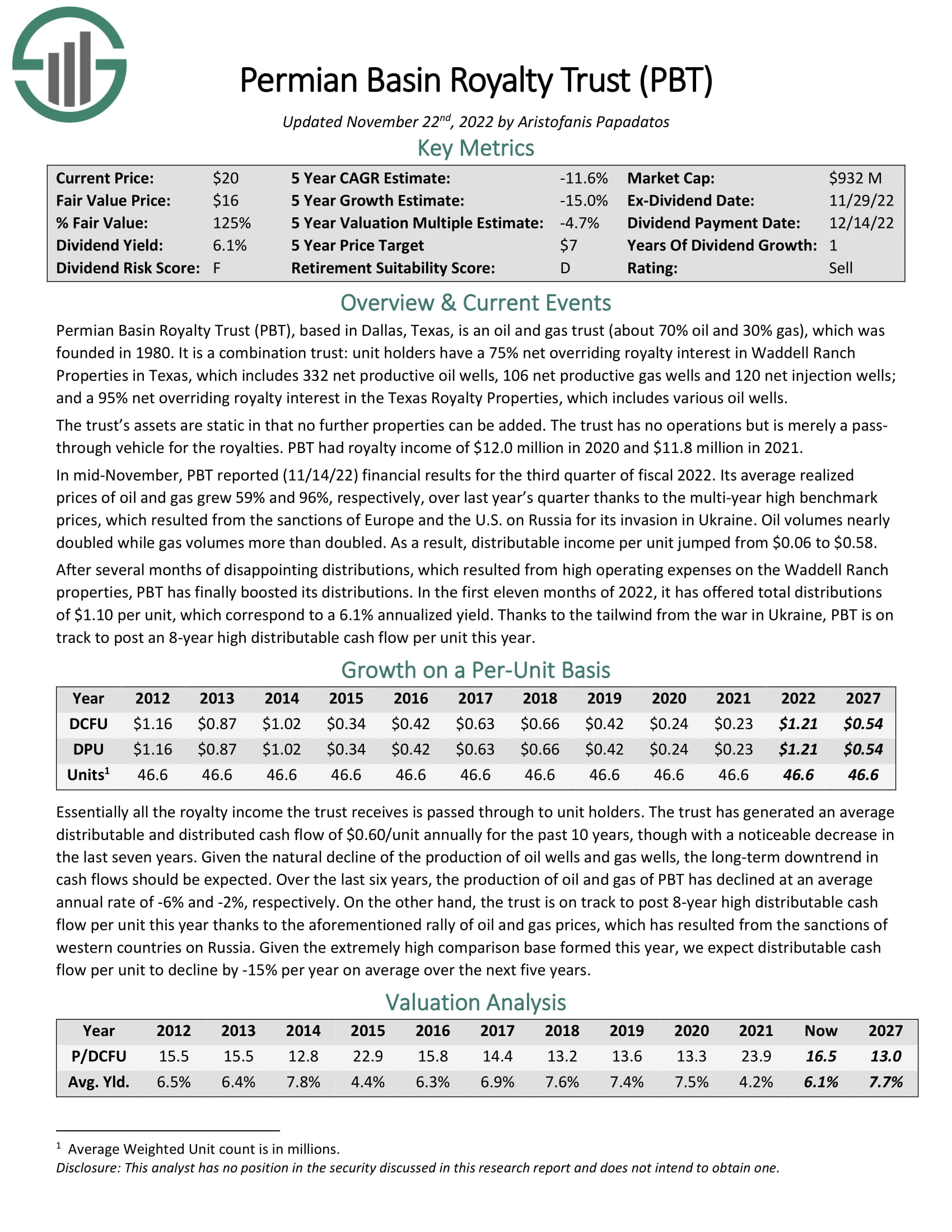

High-Yield Royalty Trust No. 7: Permian Basin Royalty Trust (PBT)

Founded in 1980, Permian Basin Royalty Trust is based in Dallas, Texas, and is an oil and gas trust (about 70% oil and 30% gas). Its unitholders have a 75% net overriding royalty interest in Waddell Ranch Properties in Texas, which includes 332 net productive oil wells, 106 net productive gas wells and 120 net injection wells; and a 95% net overriding royalty interest in the Texas Royalty Properties, which includes various oil wells.

Permian Basin Royalty Trust failed to recover from the pandemic as fast as the other oil and gas trusts due to high operating expenses on the Waddell Ranch properties. Due to these expenses, the trust offered essentially flat distributions in 2021 vs. 2020. That was a striking difference from the other oil and gas trusts, which recovered strongly from the pandemic in 2021.

On the bright side, Permian Basin Royalty Trust is thriving right now thanks to the aforementioned tailwind from the Ukrainian crisis. In 2022, the trust quintupled its total distributions per unit, from $0.23 in 2021 to a nearly 10-year high of $1.15. This level of distributions corresponds to a 5.5% yield.

Nevertheless, the trust is severely hurt by the natural decline of its production. Over the last six years, the production of oil and gas of the trust has declined at an average annual rate of -6% and -2%, respectively. Given also an expected moderation of oil and gas prices in the upcoming years, Permian Basin Royalty Trust is likely to post a sharp decrease in its distributions in the upcoming years.

Click here to download our most recent Sure Analysis report on Permian Basin Royalty Trust (PBT) (preview of page 1 of 3 shown below):

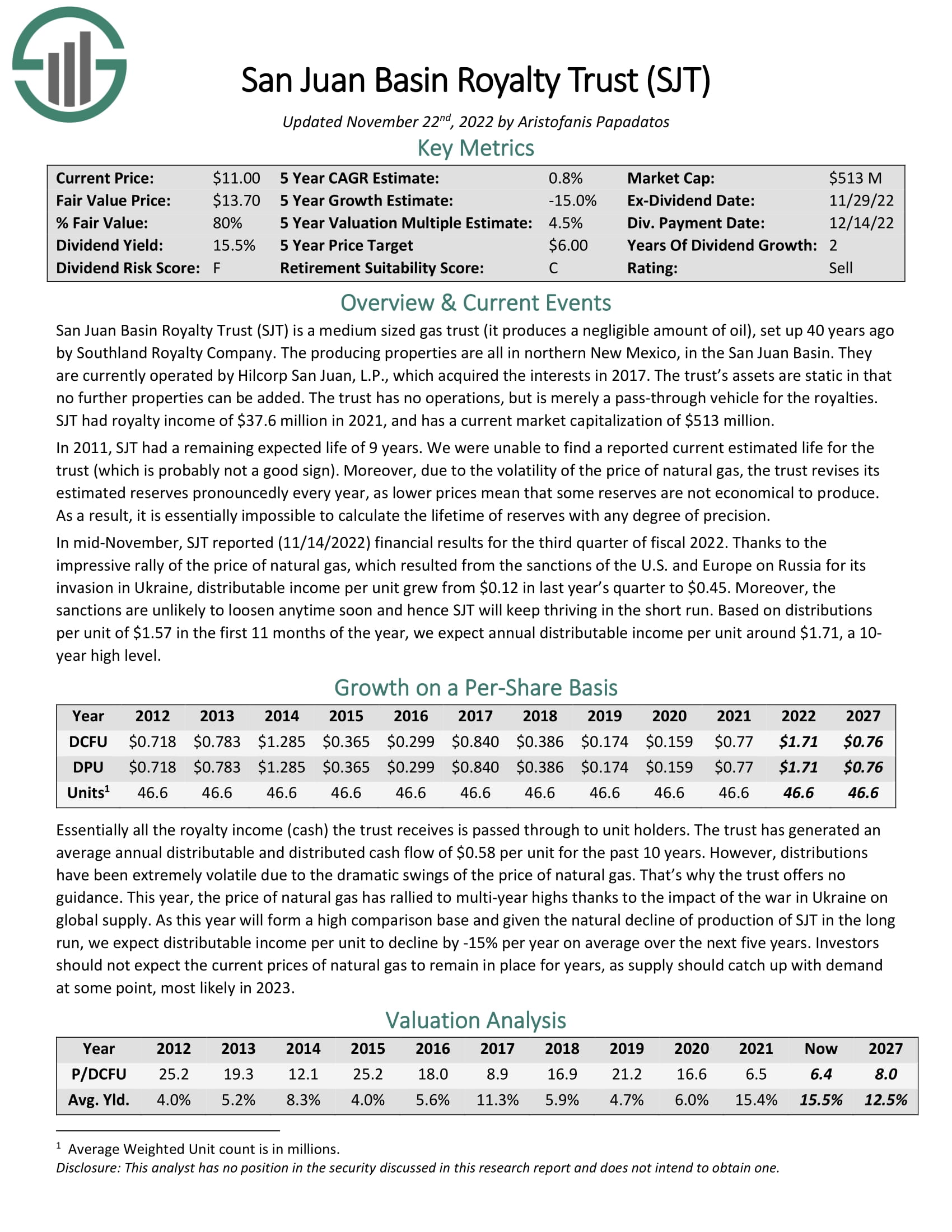

High-Yield Royalty Trust No. 6: San Juan Basin Royalty Trust (SJT)

San Juan Basin Royalty Trust is a medium sized gas trust, which was set up 40 years ago by Southland Royalty Company. The producing properties are all in northern New Mexico, in the San Juan Basin.

San Juan Basin Royalty Trust has a key difference from the other royalty trusts. It produces a negligible amount of oil and thus its results are affected only by the cycles of the price of natural gas. As a result, San Juan Basin Royalty Trust proved more resilient than its peers during the coronavirus crisis, which hurt the oil market much more severely than the gas market. In 2020, while the other trusts incurred a slump in their distributable cash flow (DCF) per unit, San Juan Basin Royalty Trust posted just a 9% decrease in its DCF per unit.

Moreover, the trust is thriving right now thanks to the sanctions of western countries on Russia. As Russia used to provide about one-third of natural gas consumed in Europe before the sanctions, the latter imported a record number of LNG cargos from the U.S in 2022. As a result, the U.S. natural gas market became exceptionally tight.

Thanks to favorable gas prices, San Juan Basin Royalty Trust more than doubled its annual distribution, from $0.77 in 2021 to a 10-year high of $1.71 in 2022. This level of distribution corresponds to a 17.3% yield. However, it is important to note that U.S. gas prices have slumped below pre-war levels lately, as the global gas market seems to have finally absorbed the effect of the Ukrainian crisis. Therefore, San Juan Basin Royalty Trust is likely to slash its distributions sharply in the upcoming months.

Click here to download our most recent Sure Analysis report on San Juan Basin Royalty Trust (SJT) (preview of page 1 of 3 shown below):

High-Yield Royalty Trust No. 5: Hugoton Royalty Trust (HGTXU)

Hugoton Royalty Trust was created in late 1998, when XTO Energy conveyed 80% net profit interests in some predominantly gas-producing properties in Kansas, Oklahoma and Wyoming to the trust. Net profits in each area are calculated by subtracting production costs, development costs and labor costs from revenues. The trust produced 88% natural gas and 12% oil in 2021.

Hugoton has a striking difference from the other oil and gas trusts, namely its extreme sensitivity to gas prices as well as to its production and development costs. Between April 2018 and October 2020, the costs of the trust exceeded its revenues, mostly due to suppressed gas prices. As a result, Hugoton did not offer any distributions during that period. Even worse, when gas prices began to recover in late 2020, the trust had to wait for its revenues to offset past losses.

On July 2nd, 2021, Hugoton announced that it had agreed to be sold to XTO Energy for $0.165 per unit in cash. That price was more than 90% lower than the stock price of Hugoton before the suspension of distributions, in 2018. In the special meeting held in December 2021, the deal was rejected by unitholders. Hugoton resumed paying monthly distributions only in August 2022. The suspension of distributions for over 4 years and the failed attempt of Hugoton to dissolve are stern reminders of the excessive risk of the trust.

On the bright side, thanks to the exceptionally favorable conditions in the U.S. natural gas market, Hugoton offered total distributions of $0.35 per unit last year. These distributions correspond to an eye-opening yield of 20.8%. Nevertheless, as mentioned above, gas prices have deflated lately. Given also the proven vulnerability of Hugoton to downturns, it is natural that the market has punished the stock with a 50% plunge off its peak, in August, which has resulted in the abnormally high distribution yield of the trust. It is prudent for investors to expect much lower distributions going forward.

Click here to download our most recent Sure Analysis report on Hugoton Royalty Trust (HGTXU) (preview of page 1 of 3 shown below):

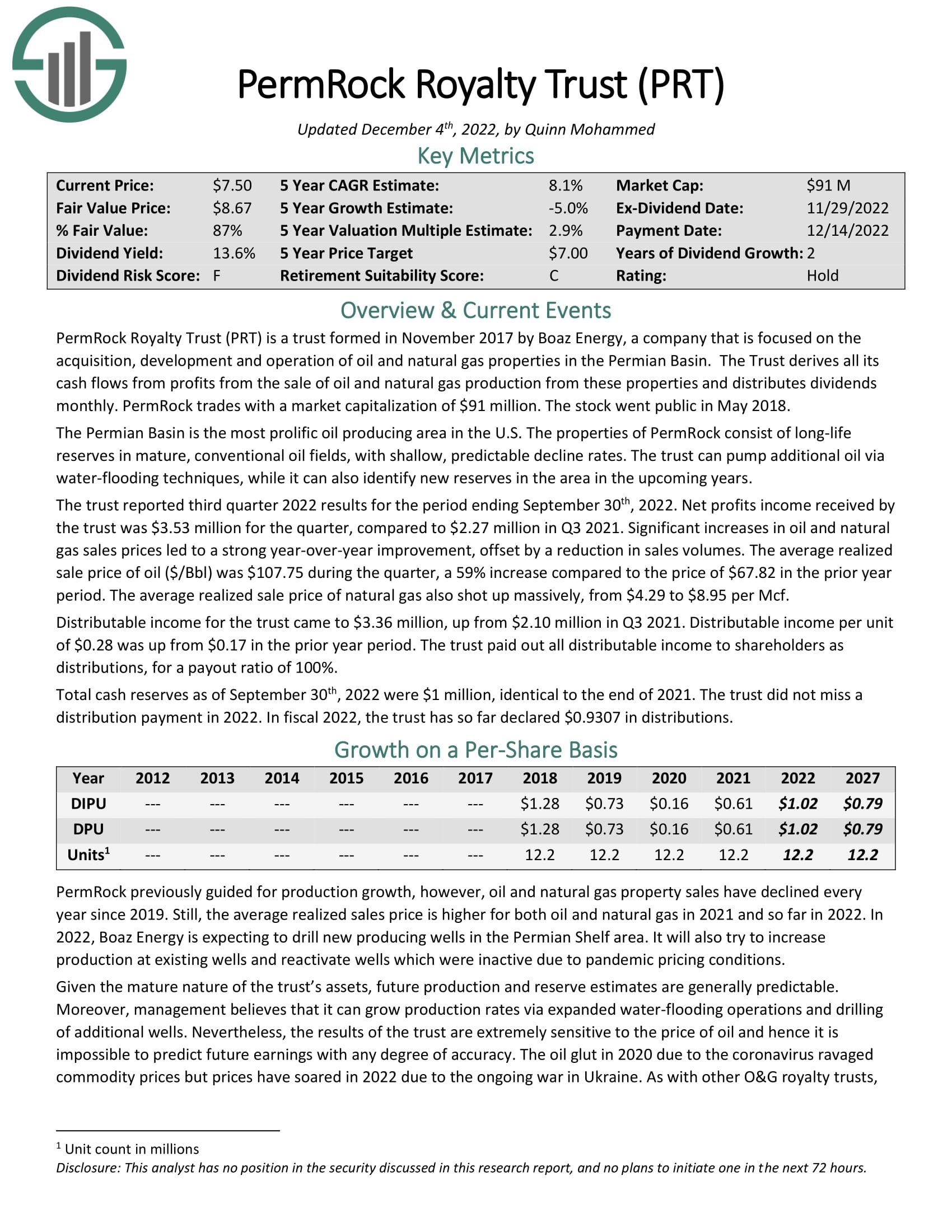

High-Yield Royalty Trust No. 4: PermRock Royalty Trust (PRT)

PermRock Royalty Trust is a trust formed in late 2017 by Boaz Energy, a company that is focused on the acquisition, development and operation of oil and natural gas properties in the Permian Basin. The Trust benefits from the unique characteristics of the Permian Basin, which is the most prolific oil producing area in the U.S. The properties of PermRock consist of long-life reserves in mature, conventional oil fields, with shallow, predictable decline rates.

PermRock is thriving right now thanks to the favorable environment of oil and gas prices. In 2022, the trust grew its distribution 67% over the prior year, from $0.61 to $1.02. This distribution corresponds to a 14.7% yield at the current stock price. However, as oil and gas prices have fallen below pre-war levels lately, the trust is likely to cut its distributions sharply in the upcoming months.

PermRock expects to drill new producing wells in the Permian Shelf area. It will also try to grow its production at existing wells and reactivate wells which were inactivated due to the slump of commodity prices during the pandemic. Nevertheless, it is important to note that the production of PermRock has declined in each of the last three years. Given also the short history of the trust and the suspension of its distributions for five consecutive months in 2020 due to the pandemic, it is evident that PermRock is riskier than most of its peers.

Click here to download our most recent Sure Analysis report on PermRock Royalty Trust (PRT) (preview of page 1 of 3 shown below):

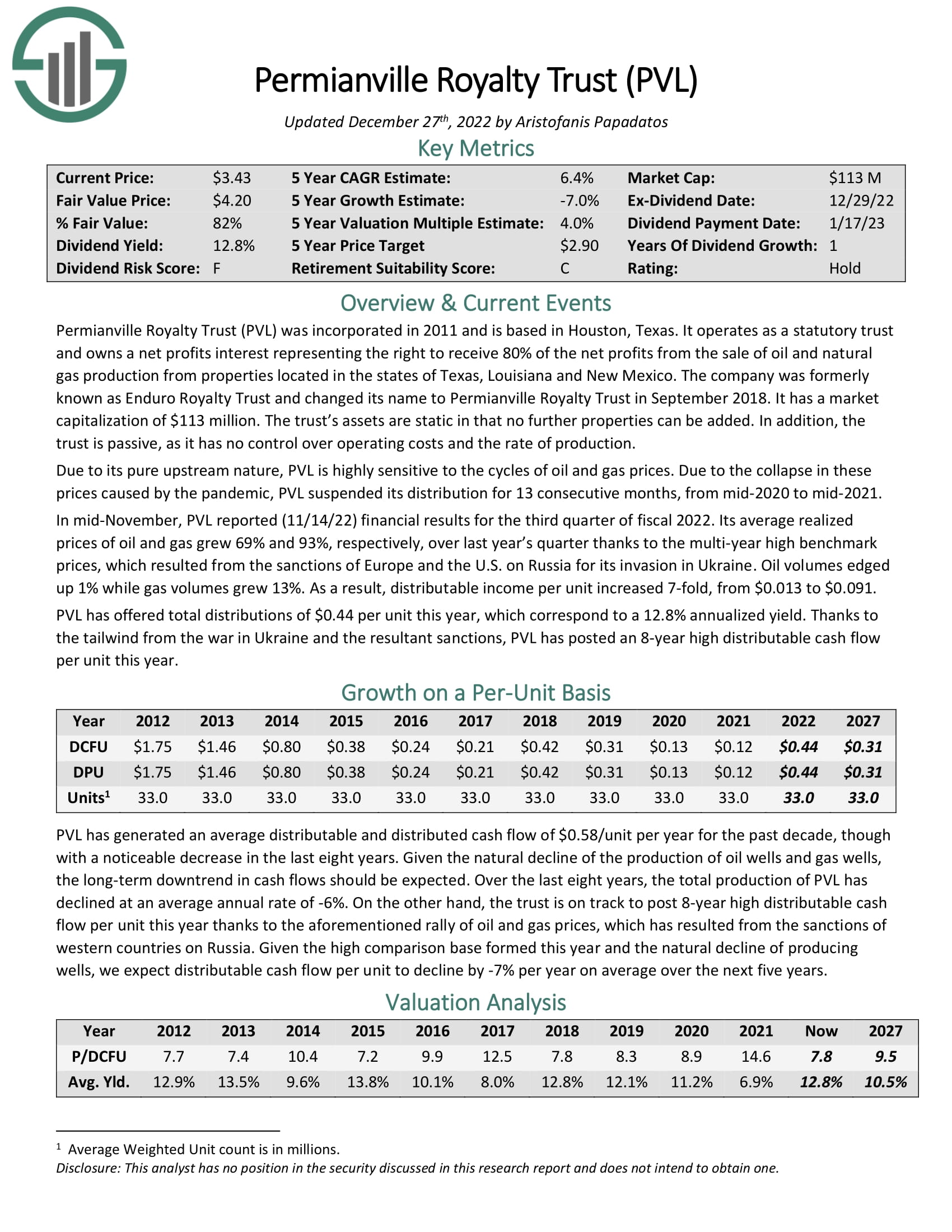

High-Yield Royalty Trust No. 3: Permianville Royalty Trust (PVL)

Permianville Royalty Trust was incorporated in 2011 and is based in Houston, Texas. It operates as a statutory trust and owns a net profits interest representing the right to receive 80% of the net profits from the sale of oil and natural gas production from properties located in the states of Texas, Louisiana and New Mexico. The company was formerly known as Enduro Royalty Trust and changed its name to Permianville Royalty Trust in September 2018.

Permianville Royalty Trust has proved more vulnerable than most royalty trusts to the downturns of the energy market. Due to the collapse in the prices of oil and gas caused by the pandemic, Permianville Royalty Trust suspended its distributions for 13 consecutive months, from mid-2020 to mid-2021. Given also the 86% plunge of the stock of Permianville Royalty Trust in 2020 due to the pandemic, it is evident that the trust is highly volatile and vulnerable to the cycles of oil and gas prices.

Despite the 13-year high oil and gas prices that prevailed last year, the total distributions of $0.44 of Permianville Royalty Trust were far lower than the annual distributions of the trust in 2012-2014. The trust suffers from the natural decline of its producing wells. Over the last eight years, the total production of Permianville Royalty Trust has declined at an average annual rate of 6%. Such a decline rate weighs heavily on future growth prospects. Overall, Permianville Royalty Trust is highly risky and hence investors should consider purchasing it only during severe downturns.

Click here to download our most recent Sure Analysis report on Permianville Royalty Trust (PVL) (preview of page 1 of 3 shown below):

High-Yield Royalty Trust No. 2: BP Prudhoe Bay Royalty Trust (BPT)

BP Prudhoe Bay Royalty Trust operates as a grantor trust in the U.S. It holds overriding royalty interest in the Prudhoe Bay oil field located on the North Slope of Alaska. The Prudhoe Bay field extends approximately 12 miles by 27 miles and contains approximately 150,000 gross productive acres. BP Prudhoe Bay Royalty Trust was formed in 1989 and is based in Houston, Texas.

In contrast to all the above trusts, BP Prudhoe Bay Royalty Trust pays its distributions every quarter, not every month. In addition, the trust has proved extremely vulnerable to the two risk factors facing all the oil and gas trusts, namely the natural decline of production and the downturns in commodity prices.

Due to the plunge in oil and gas prices caused by the pandemic, BP Prudhoe Bay Royalty Trust suspended its distributions for five consecutive quarters in 2020-2021. Moreover, despite the rally in commodity prices last year, the trust offered total distributions of $3.78, which were 59% lower than the distributions of $9.30 offered in 2012. The sharp decrease in distributions amid 13-year high oil and gas prices was caused by a steep decrease in production. The sharp decrease in production also helps explain the 85% plunge of the stock over the last decade. Overall, BP Prudhoe Bay Royalty Trust is one of the riskiest oil and gas trusts.

High-Yield Royalty Trust No. 1: MV Oil Trust (MVO)

MV Oil Trust acquires and holds net profits interests in the oil and natural gas properties of MV Partners, LLC. Its properties include about 860 producing oil and gas wells located in the Mid-Continent region in the states of Kansas and Colorado. The trust was formed in 2006 and is based in Houston, Texas.

MV Oil Trust has similar characteristics to BP Prudhoe Bay Royalty Trust. In contrast to the other trusts, MV Oil Trust pays its distributions every quarter, not every month. In addition, it has proved highly vulnerable to the natural decline of its producing wells. Despite the exceptionally favorable commodity prices last year, the trust offered total distributions of $2.21, which were 38% lower than the distributions of $3.55 offered in 2012. Based on its latest distribution, the stock is currently offering a forward distribution yield of 11.1% but it is likely to slash its distributions in the upcoming quarters due to the correction of commodity prices.

On the bright side, this performance of MV Oil Trust is much better than the aforementioned performance of BP Prudhoe Bay Royalty Trust. It is also worth noting that MV Oil Trust suspended its distributions for only one quarter in 2020 due to the pandemic. Overall, MV Oil Trust has exhibited decent business performance over the last decade but it is undoubtedly vulnerable to the major headwinds facing the oil and gas trusts, namely the downturns in oil and gas prices and the natural decline of production.

Final Thoughts

All the oil and gas trusts thrived in 2022 thanks to the exceptionally high prices of oil and gas, which resulted from the sanctions of western countries on Russia. All the trusts offered multi-year high distributions to their unitholders and thus their 12-month trailing distribution yields are exceptionally high.

However, oil and gas prices are infamous for their dramatic swings and have already returned below their level just before the onset of the Ukrainian crisis. Therefore, investors should be prepared for much lower distributions from royalty trusts going forward. They should also be aware of the excessive risk of all these trusts near the peak of their cycle. The ideal time to buy these trusts is during a severe downturn of the energy sector, when these stocks plunge and thus become deeply undervalued from a long-term perspective.

As mentioned above, all the oil and gas trusts are highly risky due to the natural decline of their production and their sensitivity to the prices of oil and gas. Sabine Royalty Trust is the trust which has proved the most resilient to these risk factors throughout its history.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them regularly:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

{kind=link}