Nastassia Samal/iStock via Getty Images

The stock market is the story of cycles and of the human behavior that is responsible for overreactions in both directions.

– Seth Klarman, billionaire investor and author

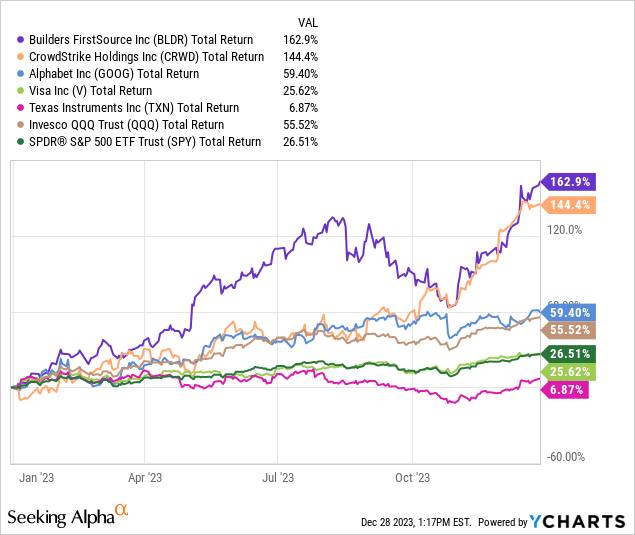

2023 was a terrific year for investors after a rough 2022. While many investors were running for the hills, there were tremendous values to be found. My top picks last year produced an average total return of 78%, beating the Nasdaq (QQQ) and S&P 500 (SPY), thanks to tremendous gains by Builders FirstSource (BLDR) and CrowdStrike (CRWD), while Texas Instruments (TXN) struggled.

To take a look back, you can check out the original article and the year in review here and here.

Looking to 2024

First, let’s acknowledge that we don’t invest year-to-year and that the business cycle doesn’t adhere to the Gregorian Calendar. The Earth’s position around the sun doesn’t affect Nvidia’s (NVDA) sales cycle, consumer debt, or interest rates.

However, a new year is an excellent time to step back and take stock (pardon the pun) of our investments and strategy; plus, it’s a great conversation starter.

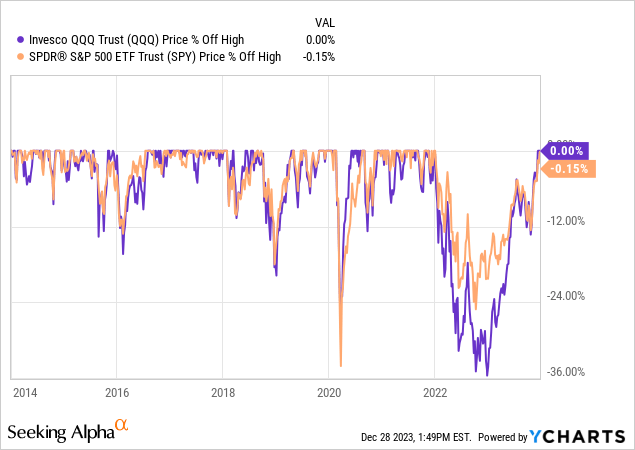

But here’s the rub. The stock market’s recent furious rally has stretched valuations. Investors are enamored with potential rate cuts in 2024, and the Fear and Greed Index shows extreme greed. Now is not the best time to buy many stocks, with markets at all-time highs, as shown below.

The market can always continue its rally; no one knows what will happen in the future. Certainly not me. Investing is partly about probabilities. We want to invest more when the odds are in our favor (like at the beginning of 2023 with the market way down) and less when the odds are the other way, as they are now at record highs.

There will likely be a healthy pullback sooner rather than later.

For this reason, I am putting purchase price targets on some of this year’s picks. Nothing extreme. In most cases, these are prices that the stock has traded for in the past 30 days.

Let’s go ahead and get to it.

Booking Holdings

Booking Holdings (BKNG) is profitable and incredibly capital-light, leading to tremendous free cash flow (FCF). It is ramping up its share buyback program, and the future is bright.

Booking runs leading travel sites, including Booking.com, Priceline, KAYAK, and OpenTable. It also competes with Airbnb (ABNB) for short-term rentals (which Booking calls “alternative accommodations”), although Booking focuses on rentals provided by professional management companies rather than individuals. This means Booking avoids some of the headaches that Airbnb deals with but has a smaller potential addressable market. This segment accounted for 33% of total room nights last quarter on 24% year-over-year (YOY) growth.

The company is focused on increasing its presence in airline ticket bookings (up 57% YOY last quarter) and becoming an end-to-end travel partner. Both will be lucrative.

Why I like the stock

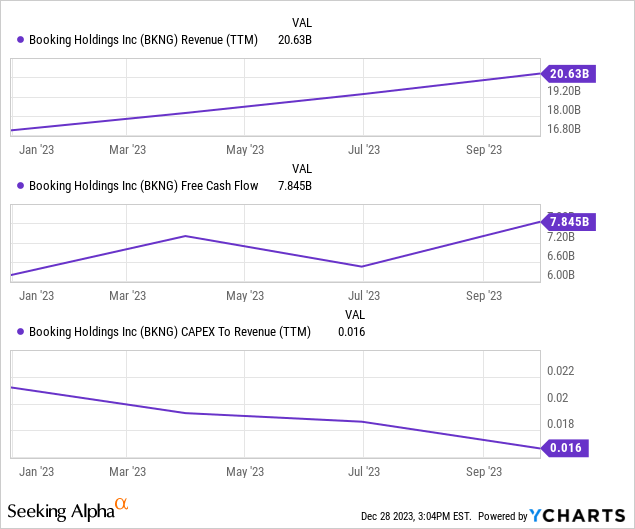

Booking’s business uses very little CapEx, which means tons of free cash flow. The FCF margin over the trailing twelve months (TTMs) is 38%, as depicted below.

This means that 38 cents of each dollar earned falls right into the company’s pocket, enabling Booking to go on a share buyback bonanza that should continue. Here are the numbers:

- $6.6 billion repurchased in 2022;

- $7.9 billion repurchased through Q3 2023;

- 13% reduction in diluted shares outstanding since January 2022;

- $16 billion remaining on the current authorization; and

- The program is dynamic.

Management expresses that they take into account the share price when making purchases.

Management said they expected Q4 purchases to outpace Q3 purchases because of the share price on the November 2nd conference call. The price was $2,839 that day and has rocketed to over $3,550. This means that buybacks have probably slowed, and investors can be patient and wait for a pullback.

Booking has $11.9 billion long-term debt on the balance sheet; however, $7.5 billion comes due in 2028 and beyond and $4.9 billion after 2030. The rates are favorable, so it does not concern me.

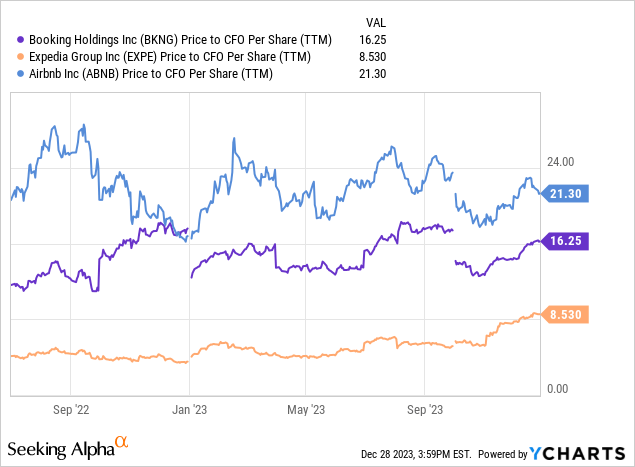

The stock trades at a price-to-operating cash flow (CFO) per share of 16, which is higher than Expedia (EXPE) and lower than Airbnb, as shown below.

This valuation is lower than the 18 it traded for in January 2020, just before the pandemic upended metrics.

Still, there are macro concerns. Consumer spending is still rising, but so is consumer debt. The recent rate hikes haven’t had a chance to work fully through the economy, student loan payments recently restarted, Buy Now Pay Later balances make me nervous, and I am concerned about a consumer pullback.

The stock is up 25% since November 2nd, and I’m not chasing it until it cools off. I’m ready to accumulate shares at $3,200 per share and below.

RTX Corporation

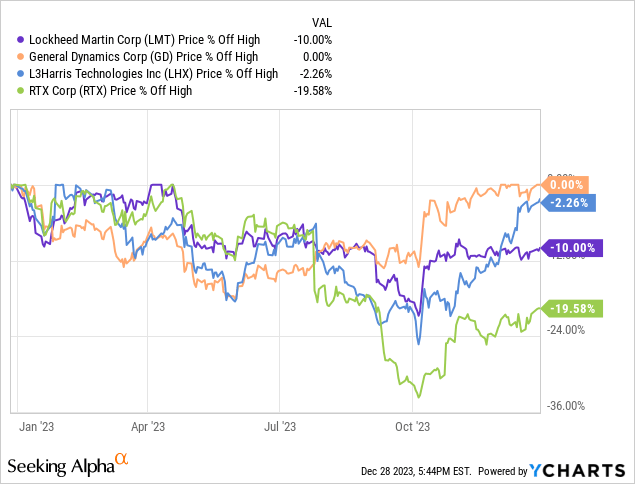

Venturing out to a company that I haven’t covered before is RTX Corporation (RTX), formerly Raytheon. Given the geopolitical climate in Europe, the Middle East, and the Pacific, Aerospace and Defense (A&D) is a terrific sector. I think RTX is recession-resistant, with a $190 billion backlog and significant government contracts.

The problem is that this isn’t exactly breaking news, right? Stocks like Lockheed Martin (LMT), General Dynamics (GD), and L3 Harris (LHX) are riding high, as shown below.

RTX missed the boat because of serious issues with some Pratt & Whitney engines. The short-term pain could be a long-term gain for patient investors.

RTX announced another accelerated $10 billion share buyback program in Q3 to support shareholders, and the yield of 2.8% is higher than recent averages and easily covered by free cash flow.

Amazon

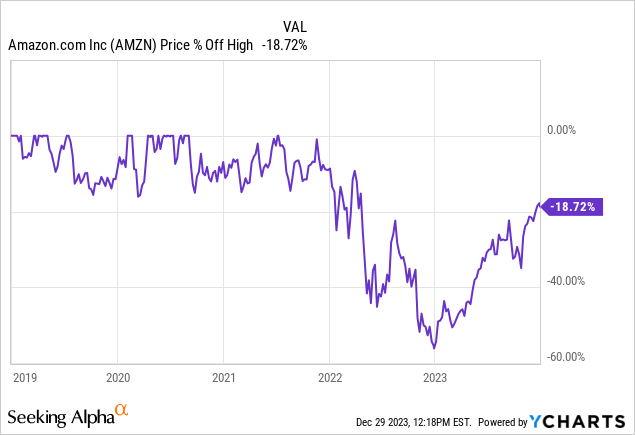

Much has been made about the Magnificent 7’s incredible rise in 2023. But again, this is an arbitrary timeframe. Amazon stock rose 81% in 2023 but is still 19% off its all-time high. It just happened that the stock troughed near the new year, as shown below.

This is the longest the stock has gone in over five years without making a new all-time high. Its 2021 high was partly driven by economic stimulus leading to a tech bubble, but it is still telling.

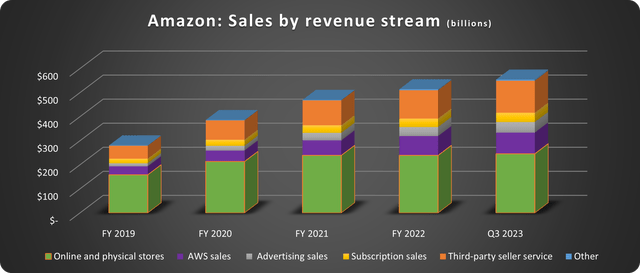

Meanwhile, the business is superior to any time in the company’s history.

Revenue is diversified, and services now outpace low-margin product sales, as shown below.

Data source: Amazon. Chart by the author.

Companies cut data usage budgets in 2023 because of recession fears, which led to Amazon taking heat this year because AWS growth slowed to the mid-teens. The opposite could happen in 2024. Generative AI and loosening budgets could cause a reacceleration of growth in AWS. If this happens, the stock will likely embark on a significant rally.

UiPath

Building a successful company (and fruitful investment) is a lot like making a cake. It takes many ingredients all coming together at the right time to rise. A company can have a brilliant idea, but nothing will come of it if the timing is wrong. Or it could have an idea and timing but need more financial resources to implement it. This is especially important now when so many companies fight for a position in artificial intelligence (AI).

The robotic process automation (RPA) company UiPath (PATH) has the ingredients to be successful. Here are a few.

Tech and timing

Imagine you run a company’s accounts payable department. The unit receives invoices from suppliers over email, possibly hundreds daily. The manual process of opening emails, downloading attachments, and then inputting the bill into the accounting system is incredibly inefficient.

Now, imagine if you could use an RPA program to do this automatically or with limited human supervision. This is precisely the type of problem that UiPath’s technology solves. More companies will be looking at using AI to solve these problems as we head into 2024.

UiPath reported 10,865 customers last quarter, including 1,974 providing over $100,000 in annual recurring revenue (ARR) and 264 over $1 million – YOY increases of 15% and 31%, respectively.

Financial results

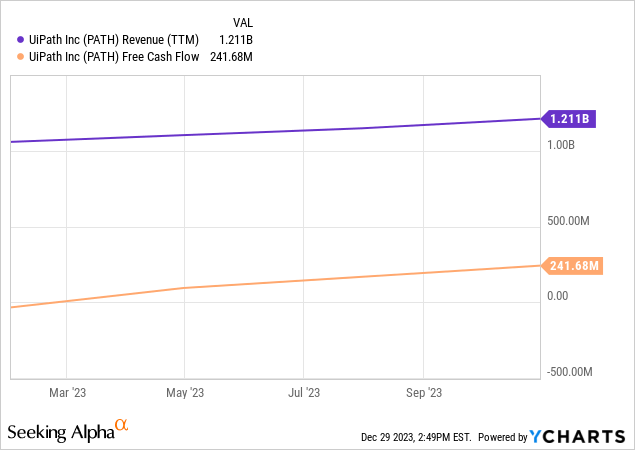

UiPath’s ARR reached $1.4 billion last quarter, and TTM sales crossed $1.2 billion. Just as importantly, UiPath produced $242 million FCF, as shown below.

This has allowed UiPath to amass a war chest of $1.8 billion in cash and investments to fund growth and make strategic tuck-in acquisitions if they arise. The company is also long-term debt-free – a big plus for shareholders.

Naturally, FCF is created by significant stock-based compensation (SBC), which raised the diluted shares outstanding by 3% YOY last quarter. But this isn’t necessarily negative. Put it this way: Would you rather the company use SBC and align employees and executives with shareholders or issue debt in a high-interest environment to fund operations? I’ll take the SBC.

Is UiPath stock a buy?

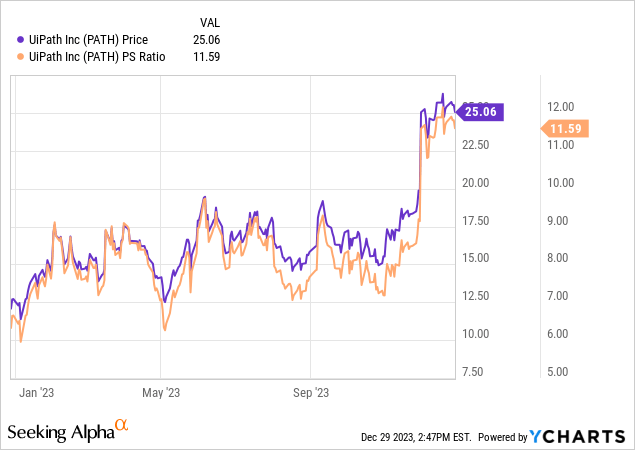

UiPath stock trades at 11.5 times sales, which isn’t out of this world for a growing, high gross margin-tech company. For instance, Palantir (PLTR) and Cloudflare (NET) trade for 18 and 23 times, respectively. However, the stock is on a tear (shown below), and ARR growth is forecast to slow to 20% YOY next quarter. Management needs a big year in 2024.

The stock has gotten ahead of itself. I will continue accumulating shares under $20.

Medtronic And Quipt Home Medical

Medical device stocks were stymied this year by the idea that weight-loss drugs would hurt the long-term outlook for things like mobility equipment, insulin pumps, diabetes therapies, CPAPs, oxygen machines, etc.

Then, just when I thought I had heard it all, Stifel came out with this gem stating that apparel stocks would benefit. Apparently, Stifel thinks Americans will take a miracle drug and hit the gym in droves.

I understand the logic for each, but they are ludicrous and juvenile in their naivety. Weight-loss drugs are not a magic elixir; side effects are emerging, and the impact on the medical equipment market is wildly overblown. Meanwhile, our population is aging, and diseases like Diabetes affect a large and growing percentage of the population.

This makes Medtronic (MDT) and microcap company Quipt Home Medical (QIPT) compelling.

Medtronic’s dividend yields 3.3%, well above its 4-year average of 2.5%, and its valuation metrics are better than industry averages.

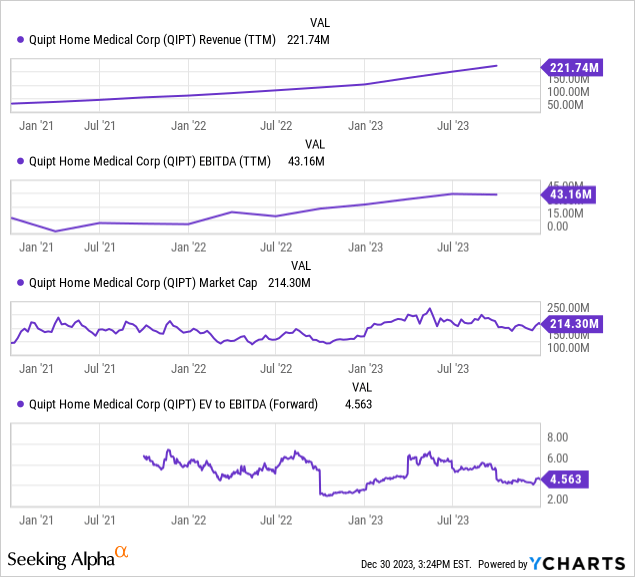

Quipt is riskier as a microcap but has significant upside potential. The company is growing through acquisition, expanding to 26 desirable states for respiratory care, and 78% of revenue is recurring.

Earlier this year, a proposed at-the-market (ATM) stock sale to fund acquisitions upset many shareholders. The ATM was canceled after the outcry, but the stock remains out of favor.

Revenue and EBITDA are ramping up on accretive acquisitions, and the market cap does not reflect the potential, as shown below.

The company has significant debt to manage, mainly a $61 million credit facility, but the risks appear priced in.

Ringing in 2024

The recent stock market rally makes it important to be selective about purchases by focusing on long-term value plays that are out of favor or waiting until the price is right to accumulate high-flying growth stocks.

Wishing everyone the very best in the New Year.

")

{kind=link}