Up to date on Might seventeenth, 2022 by Bob Ciura

Worth investing is a broad time period, and may imply various things to completely different buyers. Worth buyers usually search for low cost shares, though there isn’t any single definition of what constitutes an inexpensive inventory. Usually, worth buyers search for shares which can be buying and selling under intrinsic worth. That is the fundamental philosophy adhered to by Warren Buffett, arguably the best worth investor of all time.

Worth shares are sometimes labeled by low valuation ratios. Whereas there are a lot of methods to worth shares, the commonest valuation metric is the price-to-earnings ratio, in any other case known as the P/E ratio. Broadly talking, worth buyers usually search for shares with low P/E ratios.

For this text, worth shares are outlined because the 100 shares within the Russell 2000 with the bottom trailing price-to-earnings ratios. With this in thoughts, we compiled an inventory of those 100 worth shares.

You may obtain a free copy of the worth shares spreadsheet—with related monetary metrics like P/E ratios and dividend yields included—by clicking on the hyperlink under:

This text will talk about our valuation methodology, in addition to our prime 3 picks from the Worth Shares spreadsheet above. We consider these 3 picks symbolize the very best worth shares with the very best anticipated returns over the following 5 years, as ranked utilizing anticipated whole returns from the Certain Evaluation Analysis Database.

Desk Of Contents

You may immediately leap to a particular part of the article by utilizing the next desk of contents:

Breaking Down The P/E Ratio

The worth-to-earnings ratio, or P/E ratio, is probably essentially the most frequently-utilized valuation metric for inventory buyers. The P/E ratio primarily values shares based mostly on a a number of of the corporate’s earnings-per-share. It’s calculated by dividing the inventory value by the corporate’s earnings-per-share. The earnings-per-share of an organization represents its internet revenue on a per-share foundation. This may be discovered on an organization’s revenue assertion.

P/E ratios can both be calculated on a trailing foundation (by utilizing the corporate’s trailing 12-month EPS) or on a ahead foundation (by utilizing the corporate’s anticipated EPS over the following 12 months). The benefit of the trailing a number of is that it makes use of verifiable EPS outcomes as an alternative of a projection which can or could not materialize, whereas the ahead P/E ratio permits buyers to look forward, which many buyers consider is extra predictive.

Contemplate a inventory that has a present share value of $100, and earnings-per-share of $5.00. On this case, the inventory has a P/E ratio of 20 on a trailing foundation. There are solely two the reason why the inventory value would rise above $100. Both the corporate grows its earnings-per-share, or the P/E ratio expands above 20.

For instance, if EPS will increase to $6.00 within the following yr, the identical P/E ratio of 20 would lead to a share value of $120, for a 20% achieve. The inventory value might nonetheless rise to $120 (or greater) with out the underlying EPS progress, however the P/E ratio would rise consequently. To that finish, if EPS stay flat at $5.00 and the share value rises to $120, the P/E ratio would broaden to 24.

Consequently, in relation to motion in share costs, returns are generated for buyers both via earnings-per-share progress, or a rising P/E ratio. In our view, the very best investments are shares that ship a mix of rising EPS, an increasing P/E ratio, and dividends.

A Actual-Life Instance Of An Overvalued Inventory

For instance the potential influence that valuation can have on future returns, think about the instance of an overvalued inventory.

Contemplate the case of healthcare big Eli Lilly (LLY). Eli Lilly is a traditional instance of an amazing firm, buying and selling at an unfavorable valuation. Shares of Eli Lilly have generated spectacular annualized returns of 33.2% per yr prior to now 5 years. Nonetheless, we consider the inventory has develop into overvalued.

Primarily based on anticipated EPS of $8.23, Eli Lilly inventory now trades at a price-to-earnings ratio above 36. It is a very excessive valuation that’s effectively forward of its friends within the healthcare trade. Our honest worth estimate for Eli Lilly inventory is a P/E of 17.5 which is extra in-line with the inventory’s long-term historic valuation. This suggests important draw back threat for Eli Lilly on the present valuation stage.

If the inventory valuation declines to our honest worth estimate, it will symbolize a -13.6% annual drag on shareholder returns over the following 5 years. Even with anticipated EPS progress of 6% and the 1.3% dividend yield, Eli Lilly remains to be anticipated to generate adverse whole returns within the subsequent 5 years. Consequently, we price Eli Lilly inventory a promote, demonstrating the influence of valuation on anticipated returns.

Subsequently, it’s clear that investor returns can fluctuate considerably, based mostly on the valuation on the time of buy.

The Prime 3 Worth Shares As we speak

The next checklist represents our prime 3 shares from the Worth Shares spreadsheet. The shares on the checklist symbolize the 100 lowest ahead P/E shares within the Russell 2000.

These 3 shares have the very best whole return potential over the following 5 years from the Worth Shares sheet, as a consequence of a mix of a rising valuation a number of, future earnings progress, and dividends. Inventory picks are ranked by 5-year anticipated annual return, so as of lowest to highest.

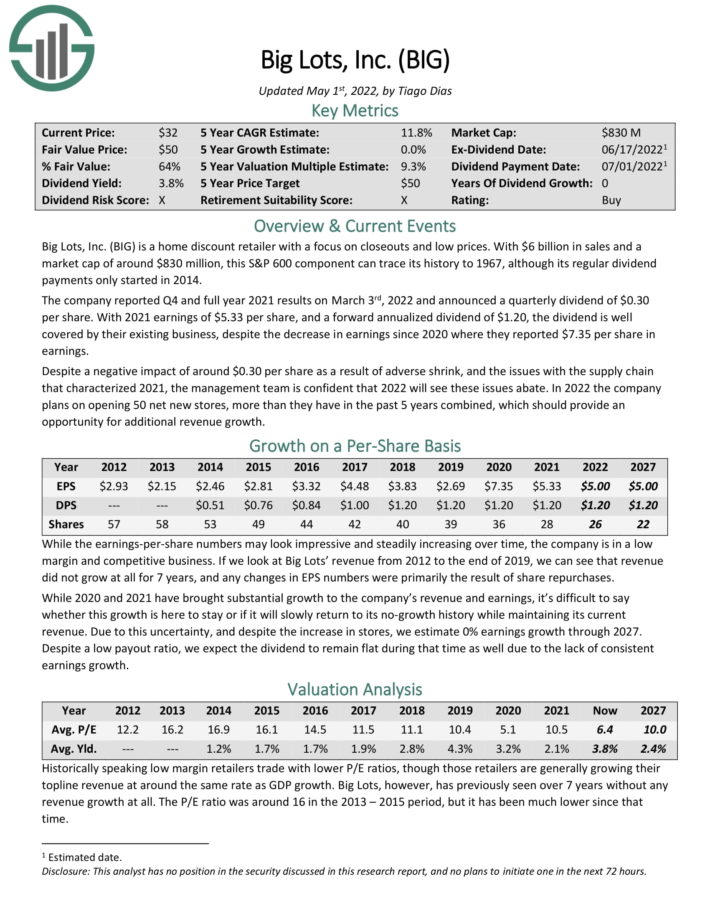

Worth Inventory #3: Huge Heaps Inc. (BIG)

- 5-year anticipated annual returns: 11.4%

Huge Heaps is a house low cost retailer with a give attention to closeouts and low costs. With $6 billion in gross sales and a

market cap of round $956 million, this S&P 600 part can hint its historical past to 1967.

Supply: Investor Presentation

The corporate reported This fall and full yr 2021 outcomes on March third, 2022 and introduced a quarterly dividend of $0.30 per share. With 2021 earnings of $5.33 per share, and a ahead annualized dividend of $1.20, the dividend is effectively lined by their present enterprise, regardless of the lower in earnings since 2020 the place they reported $7.35 per share in earnings.

Regardless of a adverse influence of round $0.30 per share because of antagonistic shrink, and the problems with the provision chain that characterised 2021, the administration staff is assured that 2022 will see these points abate. In 2022 the corporate plans on opening 50 internet new shops, greater than they’ve prior to now 5 years mixed, which ought to present a chance for extra income progress.

Huge Heaps inventory has a P/E of 5.2, making it a deep-value inventory. Shares even have a dividend yield of three.6%, whereas we count on no EPS progress. Whole returns are estimated at 11.4% over the following 5 years.

Click on right here to obtain our most up-to-date Certain Evaluation report on Huge Heaps (preview of web page 1 of three proven under):

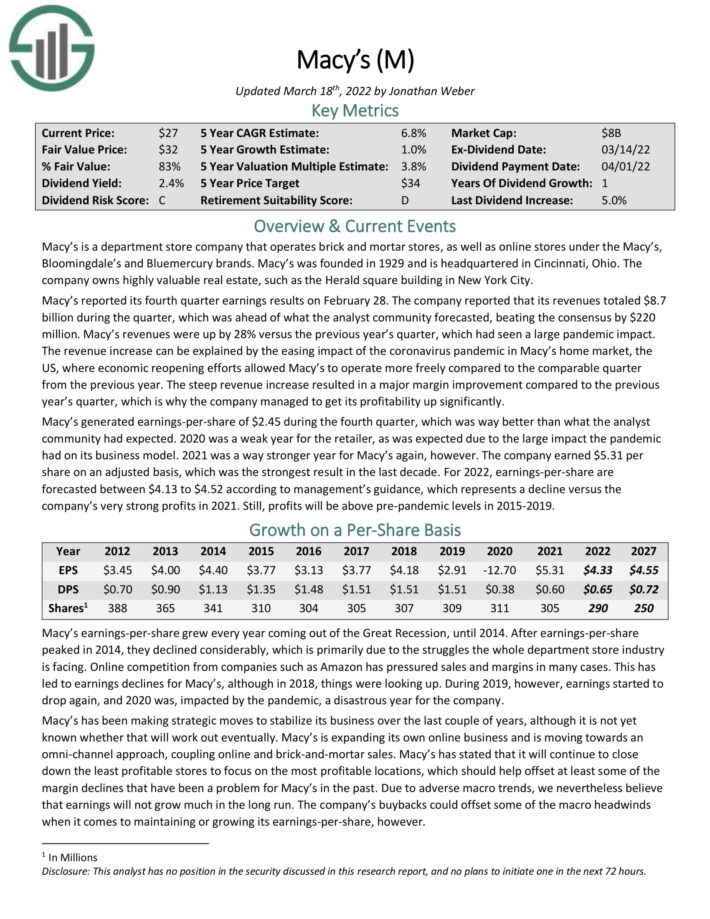

Worth Inventory #2: Macy’s Inc. (M)

- 5-year anticipated annual returns: 12.1%

Macy’s is a division retailer firm that operates brick and mortar shops, in addition to on-line shops underneath the Macy’s, Bloomingdale’s and Bluemercury manufacturers. Macy’s was based in 1929 and is headquartered in Cincinnati, Ohio. The corporate owns extremely invaluable actual property, such because the Herald sq. constructing in New York Metropolis.

Macy’s reported its fourth quarter earnings outcomes on February 28. The corporate reported that its revenues totaled $8.7 billion through the quarter, which was forward of forecasts, beating the consensus by $220 million. Macy’s revenues have been up by 28% versus the earlier yr’s quarter, which had seen a big pandemic influence.

The income enhance may be defined by the easing influence of the coronavirus pandemic in Macy’s house market, the US, the place financial reopening efforts allowed Macy’s to function extra freely in comparison with the comparable quarter from the earlier yr. The steep income enhance resulted in a serious margin enchancment in comparison with the earlier yr’s quarter, which is why the corporate managed to get its profitability up considerably.

Macy’s can be seeing sturdy progress as a consequence of its transformation right into a multi-channel retailer.

Supply: Investor Presentation

Macy’s generated earnings-per-share of $2.45 through the fourth quarter, which was approach higher than what the analyst

neighborhood had anticipated. 2020 was a weak yr for the retailer, as was anticipated as a result of giant influence the pandemic had on its enterprise mannequin. 2021 was a approach stronger yr for Macy’s once more, nonetheless. The corporate earned $5.31 per share on an adjusted foundation, which was the strongest end result within the final decade.

Macy’s inventory has a P/E of 4.2, making it a deep-value inventory. Shares even have a dividend yield of two.2%, and we count on the corporate to develop its earnings-per-share by 1% per yr. Whole returns are estimated at 12.1% over the following 5 years.

Click on right here to obtain our most up-to-date Certain Evaluation report on Macy’s (preview of web page 1 of three proven under):

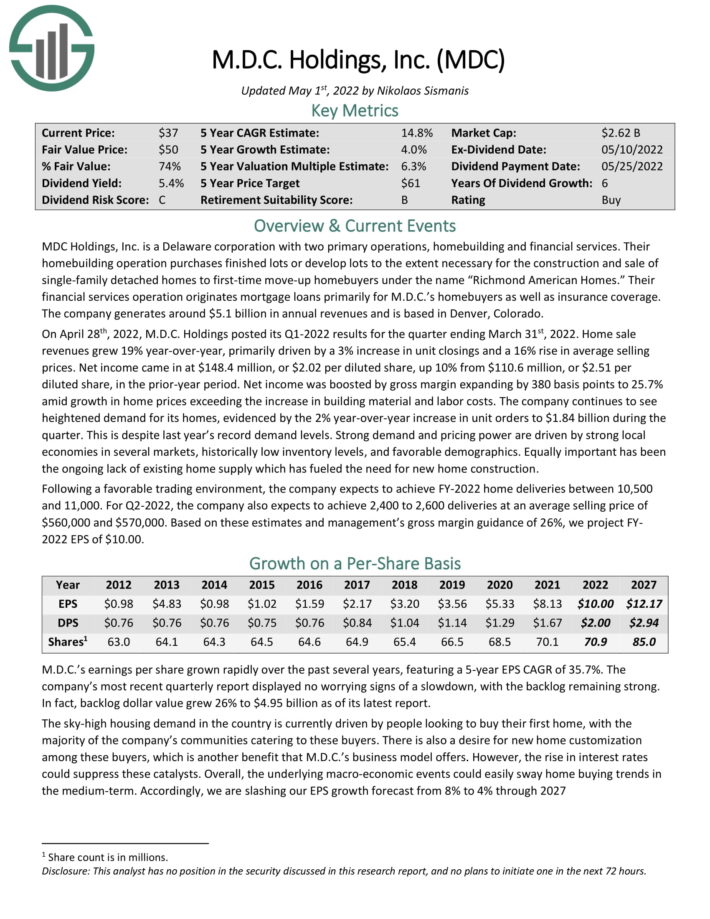

Worth Inventory #1: M.D.C Holdings (MDC)

- 5-year anticipated annual returns: 14.8%

M.D.C. Holdings has two major operations, house constructing and monetary companies. Its house constructing operation purchases completed heaps or develops heaps to the extent mandatory for the development and sale of single-family indifferent houses to house consumers underneath the identify “Richmond American Houses.” Its monetary companies operation points mortgage loans primarily for the house consumers of the corporate whereas it additionally sells insurance coverage protection.

Because of the nature of its enterprise, M.D.C. Holdings has all the time been extremely weak to recessions, as demand for brand spanking new houses plunges throughout tough financial intervals. Within the Nice Recession, the quarterly gross sales of M.D.C. Holdings plunged 99% inside only a few quarters and the corporate incurred hefty losses.

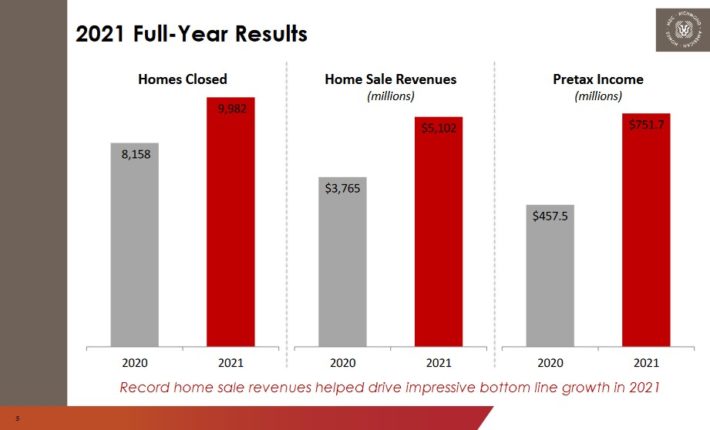

Nonetheless, M.D.C. Holdings has proved markedly resilient all through the coronavirus disaster. Regardless of the fierce recession brought on by the unprecedented lockdowns imposed in 2020, the house builder grew its earnings per share 50% in that yr, from $3.56 to $5.33.

Even higher, because of the extreme fiscal stimulus packages provided by the federal government and powerful pent-up demand, M.D.C. Holdings posted blowout leads to 2021.

Supply: Investor Presentation

The corporate grew its house sale models by 22%, from 8,158 to a document 9,982, and its earnings per share by 53%, from $5.33 to a brand new all-time excessive of $8.13.

Even higher, the enterprise momentum stays sturdy. Within the fourth quarter, the corporate grew its house sale revenues 22% over the prior yr’s quarter because of a 4% enhance in new models and a 17% enhance in common promoting costs. Consequently, it grew its earnings per share 10%.

Because of lack of present house provide and pent-up demand, M.D.C. Holdings is more likely to proceed to take pleasure in sturdy pricing energy for the foreseeable future. It additionally has a document backlog of $4.3 billion.

Administration expects 10,500-11,000 house deliveries in 2022, which correspond to five%-10% progress vs. 2021, and a gross margin round 25%, a big enchancment from 20.8% in 2020 and 23.1% in 2021.

MDC inventory has a trailing price-to-earnings ratio of 4.3. The inventory additionally has a 5.4% dividend yield, whereas we count on 4% annual EPS progress over the following 5 years. Whole returns are anticipated to achieve 14.8% per yr via 2027.

Click on right here to obtain our most up-to-date Certain Evaluation report on MDC (preview of web page 1 of three proven under):

Last Ideas

Worth investing is all about shopping for shares when they’re undervalued. However simply because a inventory has a low P/E ratio, doesn’t mechanically make it a purchase. Traders nonetheless have to carry out basic evaluation to find out the corporate’s enterprise outlook. Generally, shares seem low cost on the floor as a result of they’ve low P/E ratios, however quantity to worth traps because the enterprise mannequin is deteriorating.

Along with low P/E ratios, the three shares on this checklist even have optimistic future progress potential, and excessive dividend yields. We count on excessive whole returns from these shares over the following 5 years.

Different Dividend Lists

Worth investing is a invaluable course of to mix with dividend investing. The next lists include many extra high-quality dividend shares:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}