Up to date on June third, 2022 by Bob Ciura

Spreadsheet knowledge up to date every day

What are excessive dividend shares?

They’re shares that pay out a dividend considerably in extra of market common dividends. The S&P 500 at present has a dividend yield of simply 1.4%.

The excessive dividend shares on this article all have dividend yields of 5% or extra.

Excessive-yield shares will be very useful to shore up revenue after retirement. A $120,000 funding in shares with a mean dividend yield of 5% creates a mean of $500 a month in dividends.

Now we have created a spreadsheet of shares (and carefully associated REITs and MLPs, and so forth.) with dividend yields of 5% or extra…

You possibly can obtain your free full record of all securities with 5%+ yields (together with essential monetary metrics comparable to dividend yield and payout ratio) by clicking on the hyperlink under:

Not all high-yield shares make equally good investments…

This text examines the 7 highest yielding securities within the Positive Evaluation Analysis Database with Dividend Danger Scores of C or higher, with a minimal yield of 5%.

Notes: We replace this text close to the start of every month so make sure you bookmark this web page for subsequent month. The spreadsheet makes use of the Wilshire 5000 because the universe of securities from which to pick out, plus a couple of further securities we display screen for five%+ dividend yields.

With yields of 5% and larger, these securities all supply excessive dividends (or distributions). And with Dividend Danger Scores of C or higher, they don’t undergo from the same old extreme riskiness of actually high-yielding securities.

In different phrases, these are comparatively protected, excessive dividend shares so that you can think about including to your retirement or pre-retirement revenue portfolio.

Desk Of Contents

All excessive dividend shares on this record have dividend yields above 5%, making them very interesting in an setting of low rates of interest.

Individually, a most of three shares had been allowed for any single market sector to make sure diversification. Lastly, all of the shares are based mostly in america.

The 7 excessive dividend shares with Dividend Danger scores of C or higher are listed so as by dividend yield, from lowest to highest.

Excessive Dividend Inventory #7: Common Well being Realty (UHT)

- Dividend Yield: 5.3%

- Dividend Danger Rating: B

Common Well being Realty Earnings Belief operates as an actual property funding belief (REIT), specializing within the healthcare sector. The belief owns healthcare and human service-related amenities. Its property portfolio consists of acute care hospitals, medical workplace buildings, rehabilitation hospitals, behavioral healthcare amenities, sub-acute care amenities and childcare facilities. Common Well being’s portfolio consists of 69 properties in 20 states.

On April twenty fifth, 2022 Common Well being launched Q1 outcomes. Web revenue decreased to $0.39 from $0.41 within the year-ago interval. Funds from operations stood at $0.90, down from $0.92 within the year-ago interval primarily because of the lower in internet revenue and reduce in depreciation and amortization expense.

In the meantime, UHT declared $275.1 million of excellent borrowings pursuant to the phrases of its credit score settlement, and had $96.7 million of accessible borrowings, internet excellent borrowings and letters of credit score excellent on March 31, 2022. Income elevated 7.1% to $22.18 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on UHT (preview of web page 1 of three proven under):

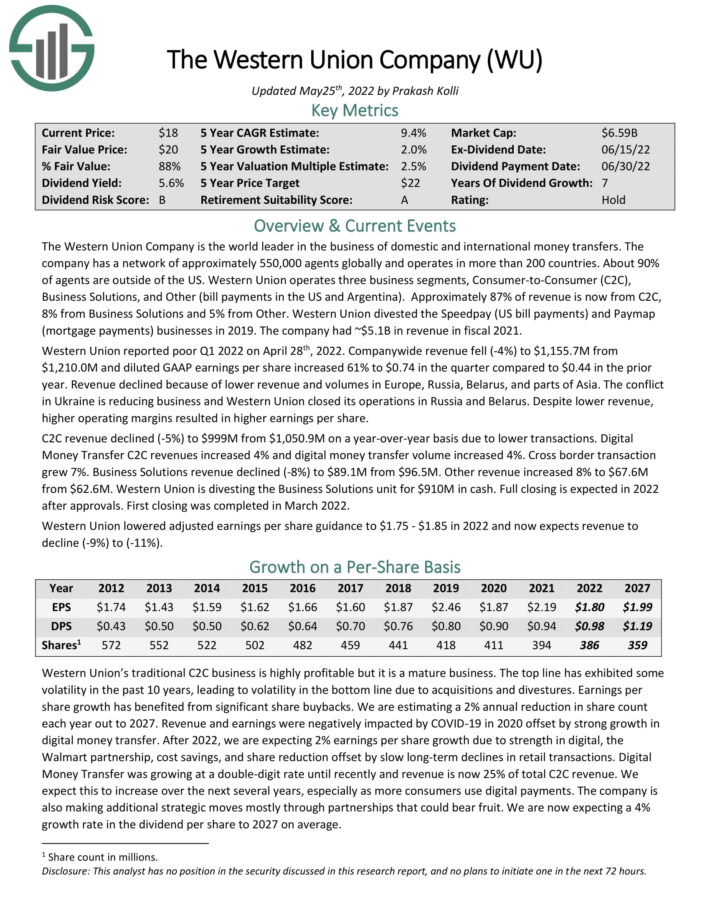

Excessive Dividend Inventory #6: Western Union (WU)

- Dividend Yield: 5.5%

- Dividend Danger Rating: B

The Western Union Firm is the world chief within the enterprise of home and worldwide cash transfers. The corporate has a community of roughly 550,000 brokers globally and operates in additional than 200 international locations. About 90% of brokers are outdoors of the US.

Western Union operates three enterprise segments, Client-to-Client (C2C), Enterprise Options, and Different (invoice funds within the US and Argentina). Roughly 87% of income is now from C2C, 8% from Enterprise Options and 5% from Different. Western Union divested the Speedpay (US invoice funds) and Paymap (mortgage funds) companies in 2019. The corporate had ~$5.1B in income in fiscal 2021.

Within the 2022 first quarter, complete income fell 4% and diluted GAAP earnings per share elevated 61% to $0.74. Income declined due to decrease income and volumes in Europe, Russia, Belarus, and elements of Asia. The battle in Ukraine is decreasing enterprise and Western Union closed its operations in Russia and Belarus. Regardless of decrease income, larger working margins resulted in larger earnings per share.

Supply: Investor Presentation

C2C income declined (-5%) to $999M from $1,050.9M on a year-over-year foundation as a result of decrease transactions. Digital Cash Switch C2C revenues elevated 4% and digital cash switch quantity elevated 4%. Cross border transaction grew 7%. Enterprise Options income declined (-8%) to $89.1M from $96.5M. Different income elevated 8% to $67.6M from $62.6M.

Western Union lowered adjusted earnings per share steering to $1.75 – $1.85 in 2022 and now expects income to

decline (-9%) to (-11%).

Click on right here to obtain our most up-to-date Positive Evaluation report on WU (preview of web page 1 of three proven under):

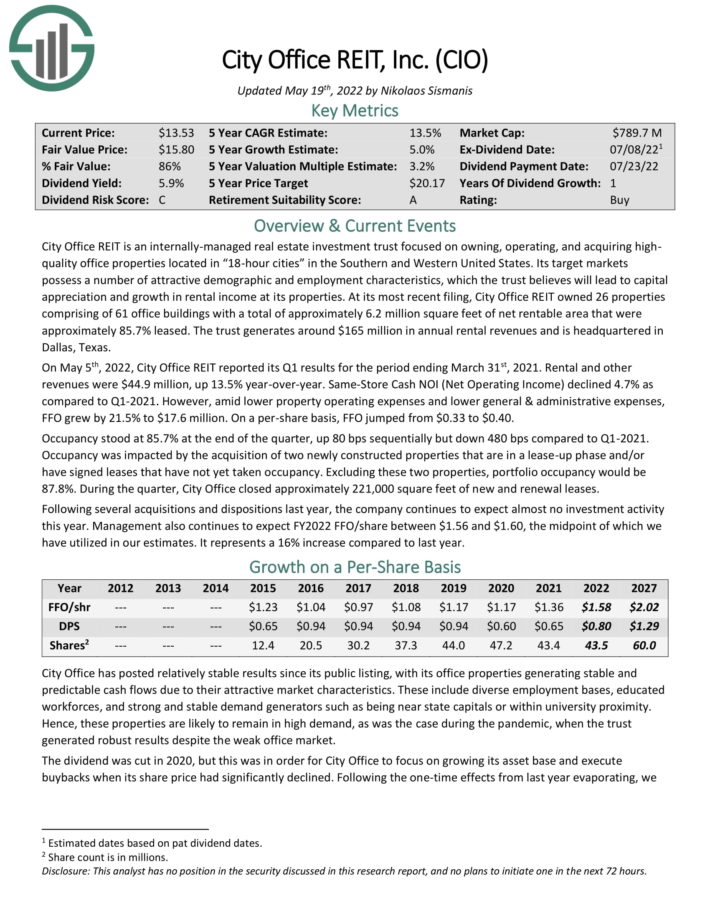

Excessive Dividend Inventory #5: Metropolis Workplace REIT (CIO)

- Dividend Yield: 5.8%

- Dividend Danger Rating: C

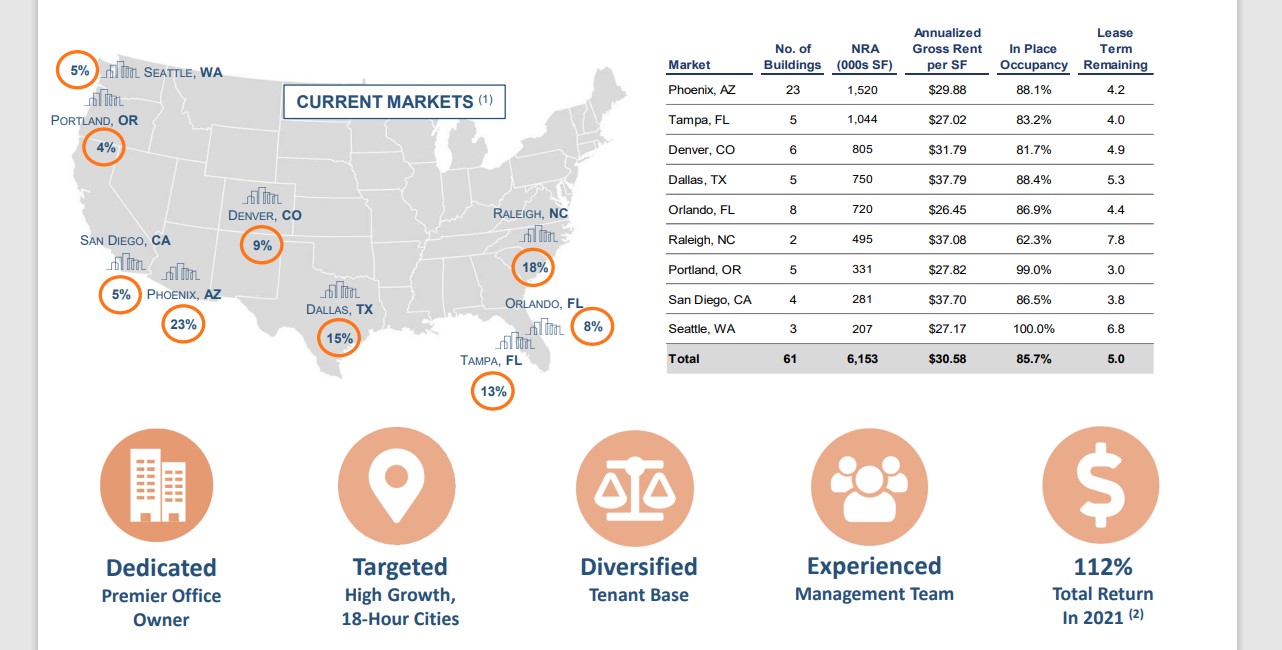

Metropolis Workplace REIT is an internally-managed actual property funding belief targeted on proudly owning, working, and buying highquality workplace properties situated in “18-hour cities” within the Southern and Western United States. Its goal markets possess quite a lot of engaging demographic and employment traits, which the belief believes will result in capital appreciation and development in rental revenue at its properties.

Supply: Investor Presentation

At its most up-to-date submitting, Metropolis Workplace REIT owned 26 properties comprising of 61 workplace buildings with a complete of roughly 6.2 million sq. toes of internet rentable space that had been roughly 85.7% leased. The belief generates round $165 million in annual rental revenues and is headquartered in Dallas, Texas.

On Might fifth, 2022, Metropolis Workplace REIT reported its Q1 outcomes for the interval ending March thirty first, 2021. Rental and different revenues had been $44.9 million, up 13.5% year-over-year. Similar-Retailer Money NOI (Web Working Earnings) declined 4.7% as in comparison with Q1-2021. Nonetheless, amid decrease property working bills and decrease basic & administrative bills, FFO grew by 21.5% to $17.6 million.

On a per-share foundation, FFO jumped from $0.33 to $0.40. Occupancy stood at 85.7% on the finish of the quarter, up 80 bps sequentially however down 480 bps in comparison with Q1-2021. Occupancy was impacted by the acquisition of two newly constructed properties which are in a lease-up part and/or have signed leases that haven’t but taken occupancy. Excluding these two properties, portfolio occupancy can be 87.8%. In the course of the quarter, Metropolis Workplace closed roughly 221,000 sq. toes of latest and renewal leases.

Following a number of acquisitions and tendencies final 12 months, the corporate continues to anticipate nearly no funding exercise this 12 months. Administration additionally continues to anticipate FY2022 FFO/share between $1.56 and $1.60, the midpoint of which we’ve got utilized in our estimates. It represents a 16% enhance in comparison with final 12 months.

Click on right here to obtain our most up-to-date Positive Evaluation report on CIO (preview of web page 1 of three proven under):

Excessive Dividend Inventory #4: Altria Group (MO)

- Dividend Yield: 6.6%

- Dividend Danger Rating: B

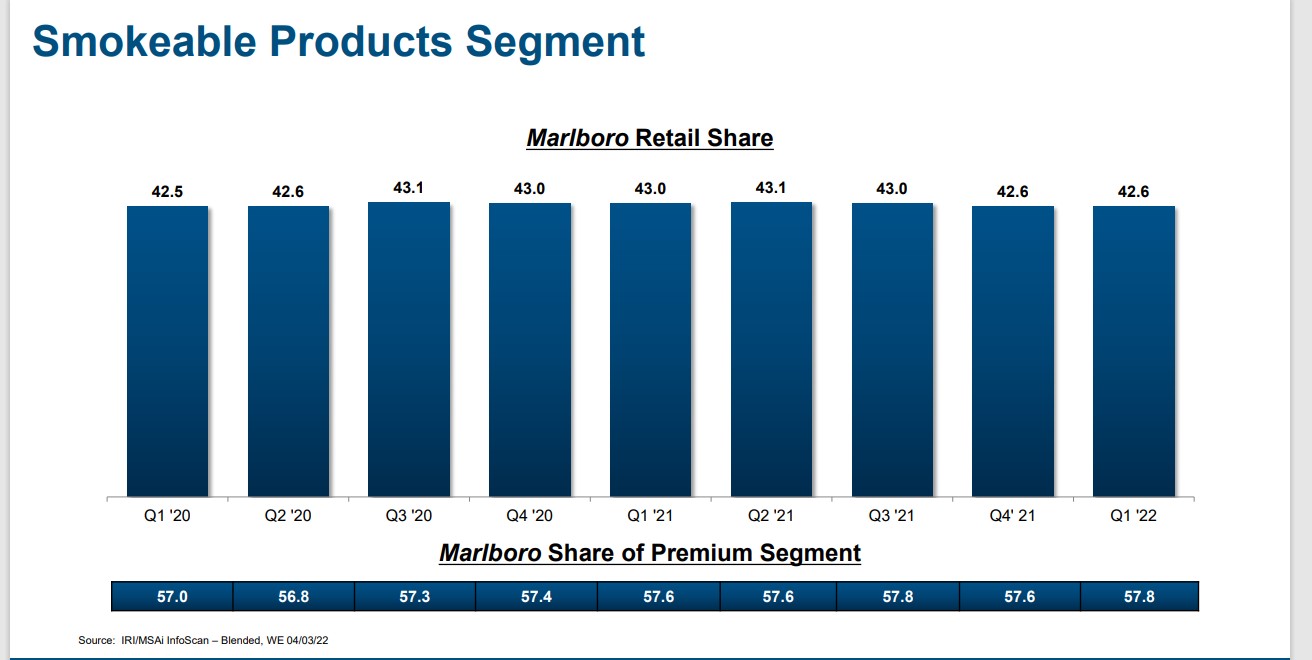

Altria Group was based by Philip Morris in 1847. As we speak, it’s a client staples large. It sells the Marlboro cigarette model within the U.S. and quite a lot of different non-smokeable manufacturers, together with Skoal and Copenhagen.

The flagship model continues to be Marlboro, which instructions over 40% retail market share within the U.S.

Supply: Investor Presentation

Altria additionally has a 10% possession stake in international beer large Anheuser-Busch InBev, along with giant stakes in Juul, a vaping merchandise producer and distributor, in addition to hashish firm Cronos Group (CRON).

On 04/28/22, Altria reported first quarter FY22 outcomes. Adjusted diluted earnings-per-share elevated 4.7% to $1.12 year-over-year. Web income stood at $5.9 billion, down by 2.4% primarily brought on by the sale of the wine enterprise in October 2021. Reported diluted earnings per share stood at $1.08, up by 40.3% year-over-year. Income decreased 1.2% to $4.82 billion year-over-year.

In the meantime, Altria reported roughly $1.2 billion remaining beneath the corporate’s current $3.5 billion share repurchase program which is predicted to finish by December 31, 2022. The corporate additionally reaffirmed full-year 2022 adjusted diluted earnings-per-share steering of $4.79-$4.93.

Altria has elevated its dividend for over 50 years, putting it on the unique Dividend Kings record. It is usually a Dividend Champion.

Click on right here to obtain our most up-to-date Positive Evaluation report on Altria Group (preview of web page 1 of three proven under):

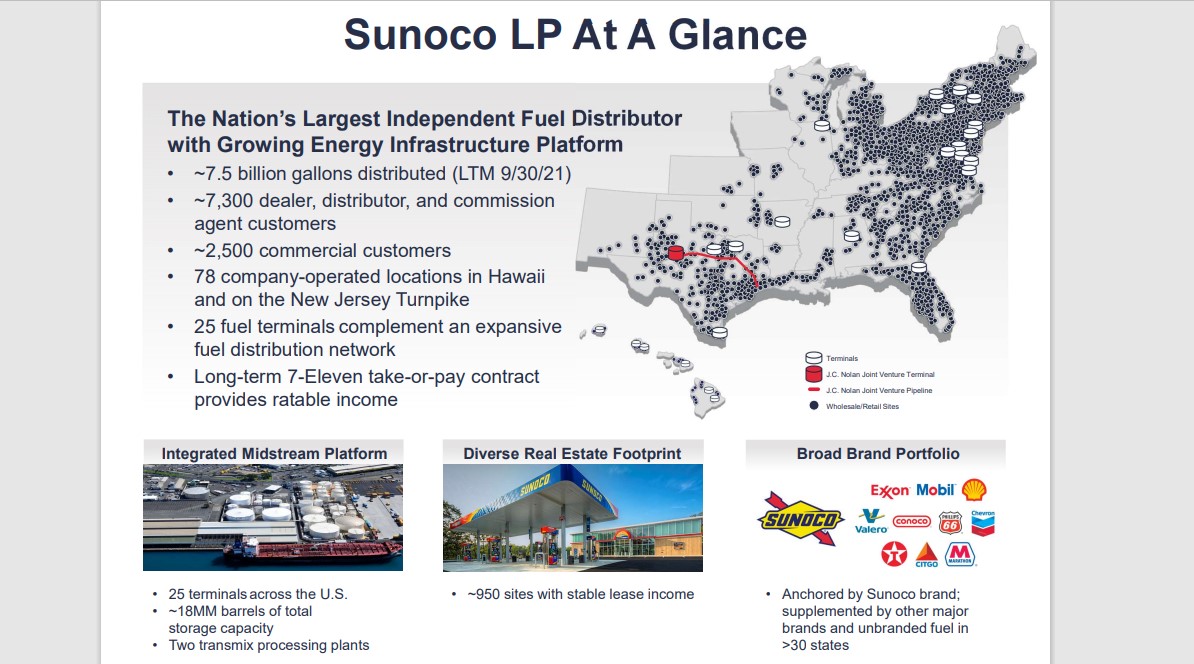

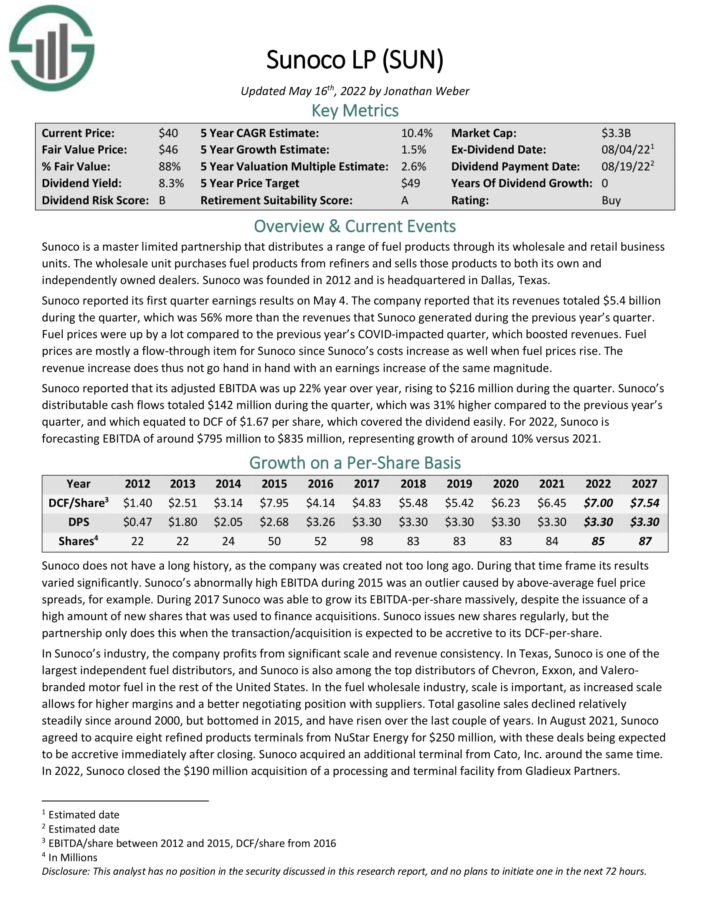

Excessive Dividend Inventory #3: Sunoco LP (SUN)

- Dividend Yield: 7.9%

- Dividend Danger Rating: B

Sunoco is a Grasp Restricted Partnership that distributes gas merchandise via its wholesale and retail enterprise items. The wholesale unit purchases gas merchandise from refiners and sells these merchandise to each its personal and independently-owned sellers.

The retail unit operates shops the place gas merchandise in addition to different merchandise comparable to comfort merchandise and meals are offered to prospects.

Associated: The Prime 20 Highest Yielding MLPs Now

Supply: Investor Presentation

Sunoco reported its first quarter earnings outcomes on Might 4. Revenues totaled $5.4 billion, which was 56% development from the earlier 12 months’s quarter. Gas costs rose closely which boosted revenues. However gas costs are largely a flow-through merchandise for Sunoco as its prices enhance when gas costs rise. Due to this fact, adjusted EBITDA was up 22% 12 months over 12 months, rising to $216 million throughout the quarter.

Distributable money flows totaled $142 million throughout the quarter, which was 31% larger in comparison with the earlier 12 months’s quarter, and which equated to DCF of $1.67 per share, which coated the dividend simply. For 2022, Sunoco is forecasting EBITDA of round $795 million to $835 million, representing development of round 10% versus 2021.

Click on right here to obtain our most up-to-date Positive Evaluation report on Sunoco (preview of web page 1 of three proven under):

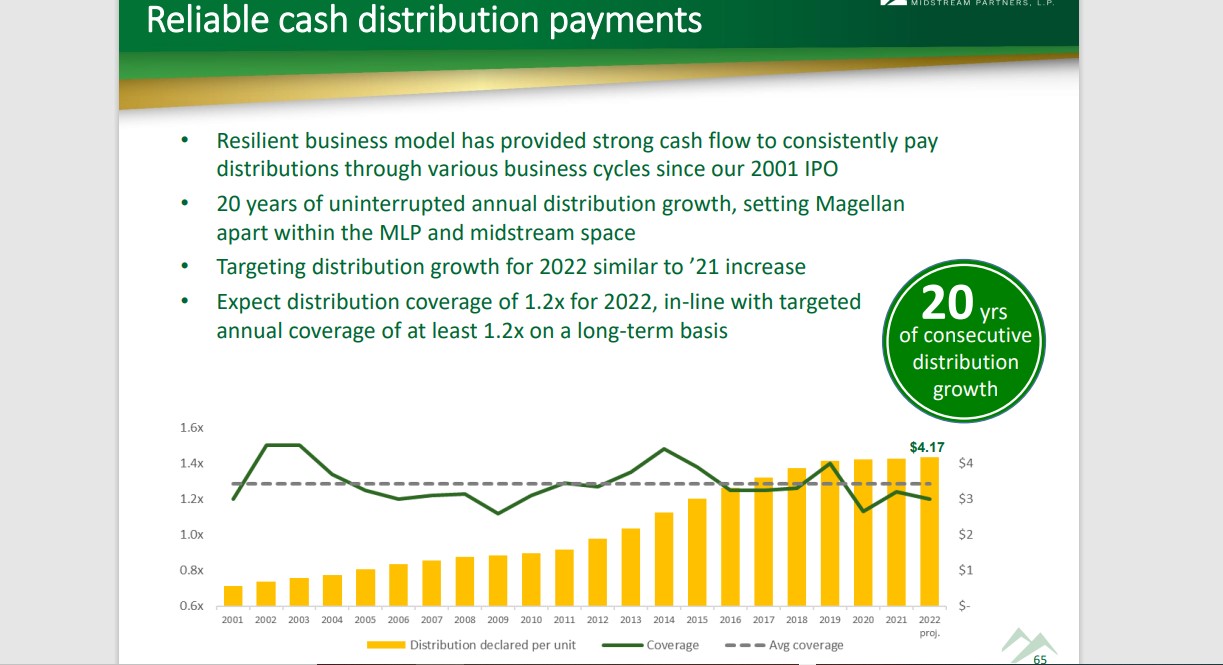

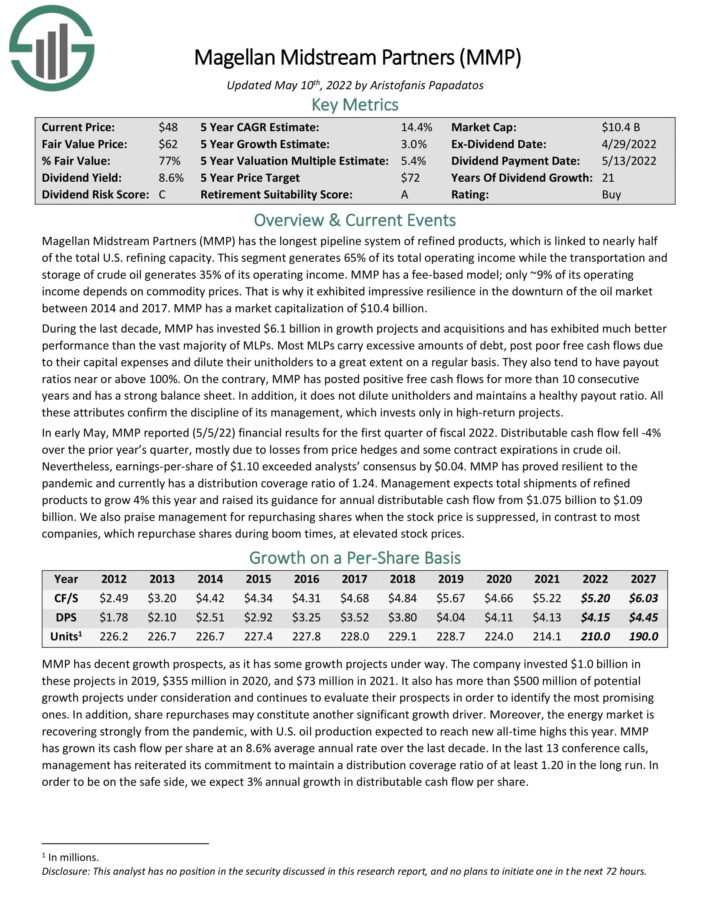

Excessive Dividend Inventory #2: Magellan Midstream Companions LP (MMP)

- Dividend Yield: 7.9%

- Dividend Danger Rating: C

Magellan Midstream Companions is a Grasp Restricted Partnership, or MLP. Magellan has the longest pipeline system of refined merchandise, which is linked to almost half of the overall U.S. refining capability.

This section generates ~65% of its complete working revenue whereas the transportation and storage of crude oil generates ~35% of its working revenue. MMP has a fee-based mannequin; solely ~10% of its working revenue is determined by commodity costs.

MMP has a protracted historical past of regular distributions:

Supply: Investor Presentation

In early Might, MMP reported (5/5/22) monetary outcomes for the primary quarter of fiscal 2022. Distributable money stream fell -4% over the prior 12 months’s quarter, largely as a result of losses from value hedges and a few contract expirations in crude oil. However, earnings-per-share of $1.10 exceeded analysts’ consensus by $0.04. MMP has proved resilient to the pandemic and at present has a distribution protection ratio of 1.24.

Administration expects complete shipments of refined merchandise to develop 4% this 12 months and raised its steering for annual distributable money stream from $1.075 billion to $1.09 billion.

Click on right here to obtain our most up-to-date Positive Evaluation report on MMP (preview of web page 1 of three proven under):

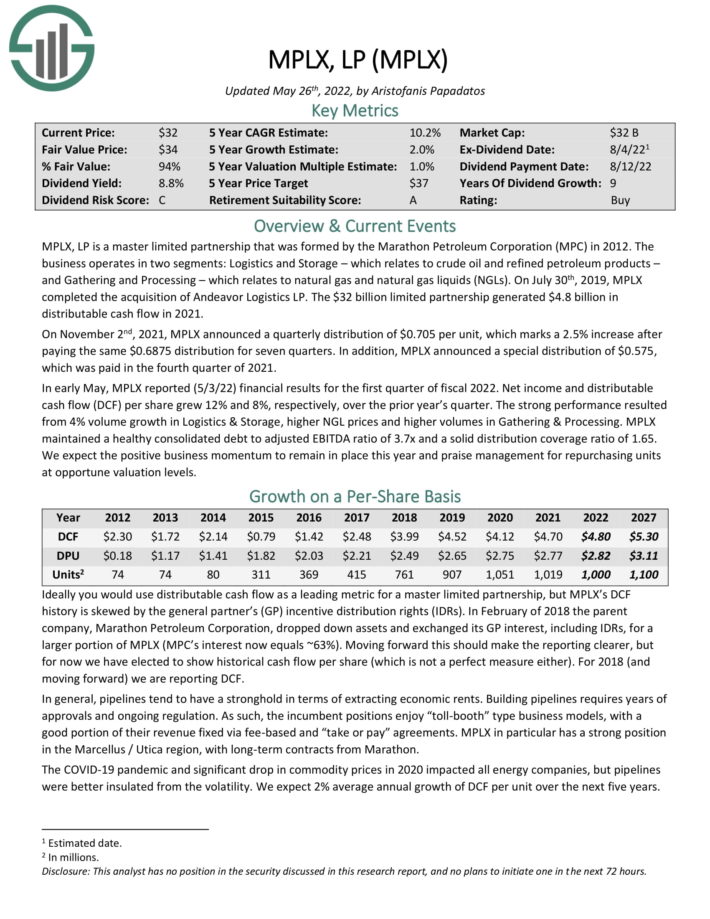

Excessive Dividend Inventory #1: MPLX LP (MPLX)

- Dividend Yield: 8.5%

- Dividend Danger Rating: C

MPLX, LP is a Grasp Restricted Partnership that was fashioned by the Marathon Petroleum Company (MPC) in 2012.

The enterprise operates in two segments: Logistics and Storage – which pertains to crude oil and refined petroleum merchandise – and Gathering and Processing – which pertains to pure fuel and pure fuel liquids (NGLs). In 2019, MPLX acquired Andeavor Logistics LP.

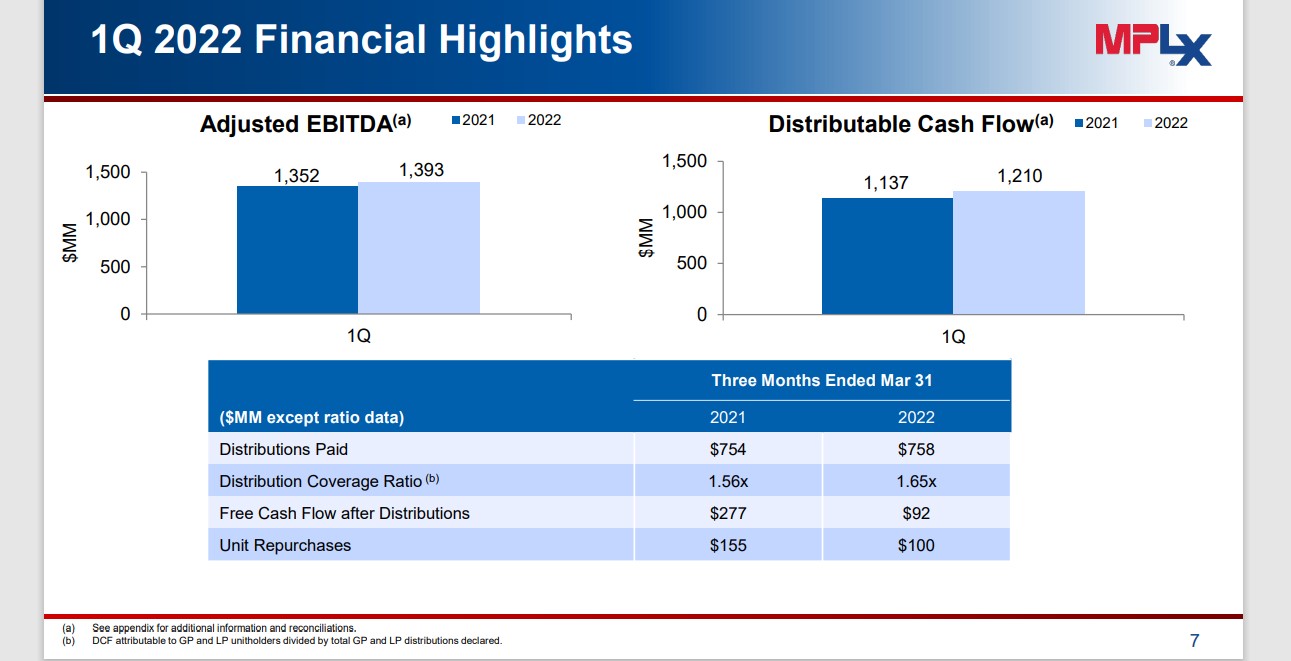

You possibly can see highlights of the corporate’s first-quarter report within the picture under:

Supply: Investor Presentation

Web revenue and distributable money stream (DCF) per share grew 12% and eight%, respectively, over the prior 12 months’s quarter. The robust efficiency resulted from 4% quantity development in Logistics & Storage, larger NGL costs and better volumes in Gathering & Processing.

MPLX maintained a wholesome consolidated debt to adjusted EBITDA ratio of three.7x and a strong distribution protection ratio of 1.65.

Click on right here to obtain our most up-to-date Positive Evaluation report on MPLX (preview of web page 1 of three proven under):

The Excessive Dividend 50

You possibly can see evaluation on the 50 highest-yielding shares under, excluding worldwide securities, royalty trusts, REITs, and MLPs.

The Excessive Dividend 50 are listed so as of their dividend yields as of March 14th, 2022. The latest Positive Evaluation Analysis Database report for every safety is included as effectively.

- Artisan Companions Asset Administration (APAM) | [See newest Sure Analysis report]

- Lumen Applied sciences (LUMN) | [See newest Sure Analysis report]

- Antero Midstream (AM) | [See newest Sure Analysis report]

- Through Renewables (VIA) | [See newest Sure Analysis report]

- Vector Group (VGR) | [See newest Sure Analysis report]

- B&G Meals (BGS) | [See newest Sure Analysis report]

- Altria Group (MO) | [See newest Sure Analysis report]

- New York Group Bancorp (NYCB) | [See newest Sure Analysis report]

- ONEOK Inc. (OKE) | [See newest Sure Analysis report]

- Southern Copper Company (SCCO) | [See newest Sure Analysis report]

- Common Corp. (UVV) | [See newest Sure Analysis report]

- Western Union (WU) | [See newest Sure Analysis report]

- Northwest Bancshares (NWBI) | [See newest Sure Analysis report]

- Philip Morris Worldwide (PM) | [See newest Sure Analysis report]

- Blackstone Group (BX) | [See newest Sure Analysis report]

- Xerox Holdings (XRX) | [See newest Sure Analysis report]

- Worldwide Enterprise Machines (IBM) | [See newest Sure Analysis report]

- Foot Locker (FL) | [See newest Sure Analysis report]

- Gilead Sciences (GILD) | [See newest Sure Analysis report]

- M.D.C. Holdings (MDC) | [See newest Sure Analysis report]

- Viatris Inc. (VTRS) | [See newest Sure Analysis report]

- Verizon Communications (VZ) | [See newest Sure Analysis report]

- AT&T Inc. (T) | [See newest Sure Analysis report]

- Mercury Common (MCY) | [See newest Sure Analysis report]

- Phillips 66 (PSX) | [See newest Sure Analysis report]

- Leggett & Platt (LEG) | [See newest Sure Analysis report]

- Pinnacle West Capital (PNW) | [See newest Sure Analysis report]

- Dow Inc. (DOW) | [See newest Sure Analysis report]

- PetMed Specific (PETS) | [See newest Sure Analysis report]

- Cracker Barrel Outdated Nation Retailer (CBRL) | [See newest Sure Analysis report]

- Prudential Monetary (PRU) | [See newest Sure Analysis report]

- Unum Group (UNM) | [See newest Sure Analysis report]

- Worldwide Paper (IP) | [See newest Sure Analysis report]

- Edison Worldwide (EIX) | [See newest Sure Analysis report]

- Valero Vitality (VLO) | [See newest Sure Analysis report]

- Franklin Sources (BEN) | [See newest Sure Analysis report]

- Hole, Inc. (GPS) | [See newest Sure Analysis report]

- Newell Manufacturers (NWL) | [See newest Sure Analysis report]

- ExxonMobil Company (XOM) | [See newest Sure Analysis report]

- OGE Vitality (OGE) | [See newest Sure Analysis report]

- Kraft-Heinz (KHC) | [See newest Sure Analysis report]

- H&R Block (HRB) | [See newest Sure Analysis report]

- Weyco Group (WEYS) | [See newest Sure Analysis report]

- Kontoor Manufacturers (KTB) | [See newest Sure Analysis report]

- 3M Firm (MMM) | [See newest Sure Analysis report]

- TrustCo Financial institution Corp. (TRST) | [See newest Sure Analysis report]

- Huntington Bancshares Inc. (HBAN) | [See newest Sure Analysis report]

- Spire Inc. (SR) | [See newest Sure Analysis report]

- United Bankshares Inc. (UBSI) | [See newest Sure Analysis report]

- Washington Belief Bancorp (WASH) | [See newest Sure Analysis report]

Ultimate Ideas

The 7 excessive dividend shares analyzed above all have dividend yields of 5% or larger. And importantly, these securities typically have higher threat profiles than the typical high-yield safety.

That mentioned, a dividend is rarely assured, and excessive dividend shares are probably liable to dividend reductions or suspensions if a recession happens within the close to future.

Buyers ought to proceed to watch every inventory to ensure their fundamentals and development stay on observe, significantly amongst shares with extraordinarily excessive dividend yields.

Moreover, the next Positive Dividend databases comprise essentially the most dependable dividend shares in our funding universe:

You possibly can obtain the free spreadsheet under for extra high-yield funding concepts.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}