Updated on October 25th, 2023

In the world of investing, there are certain sectors that tend to lend themselves more to growth, value, or great dividend characteristics. Depending upon one’s goals, allocating most appropriately to these characteristics can make a big difference to total returns over the investor’s lifetime.

One type of stock that tends to see a high rate of dividend payers is so-called “sin stocks.” These are stocks that are generally defined as those selling tobacco or alcohol, but recently expanded to those selling cannabis or other related products that have age restrictions.

You can see the full downloadable spreadsheet of all 51 Dividend Kings (along with important financial metrics such as dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the link below:

Sin stocks tend to see fairly stable earnings during all kinds of economic conditions, which is why the group lends itself to dividend investors as a good choice for income.

In this article, we’ll take a look at 10 sin stocks we like today for total returns and income prospects.

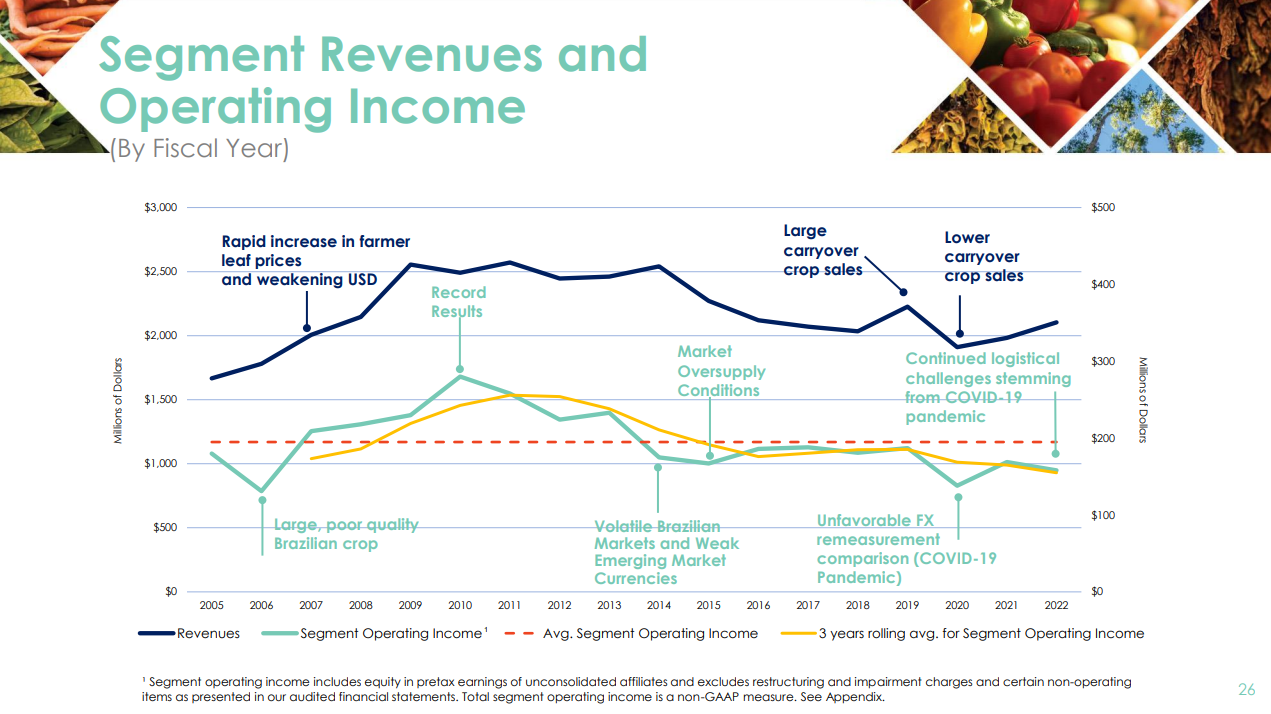

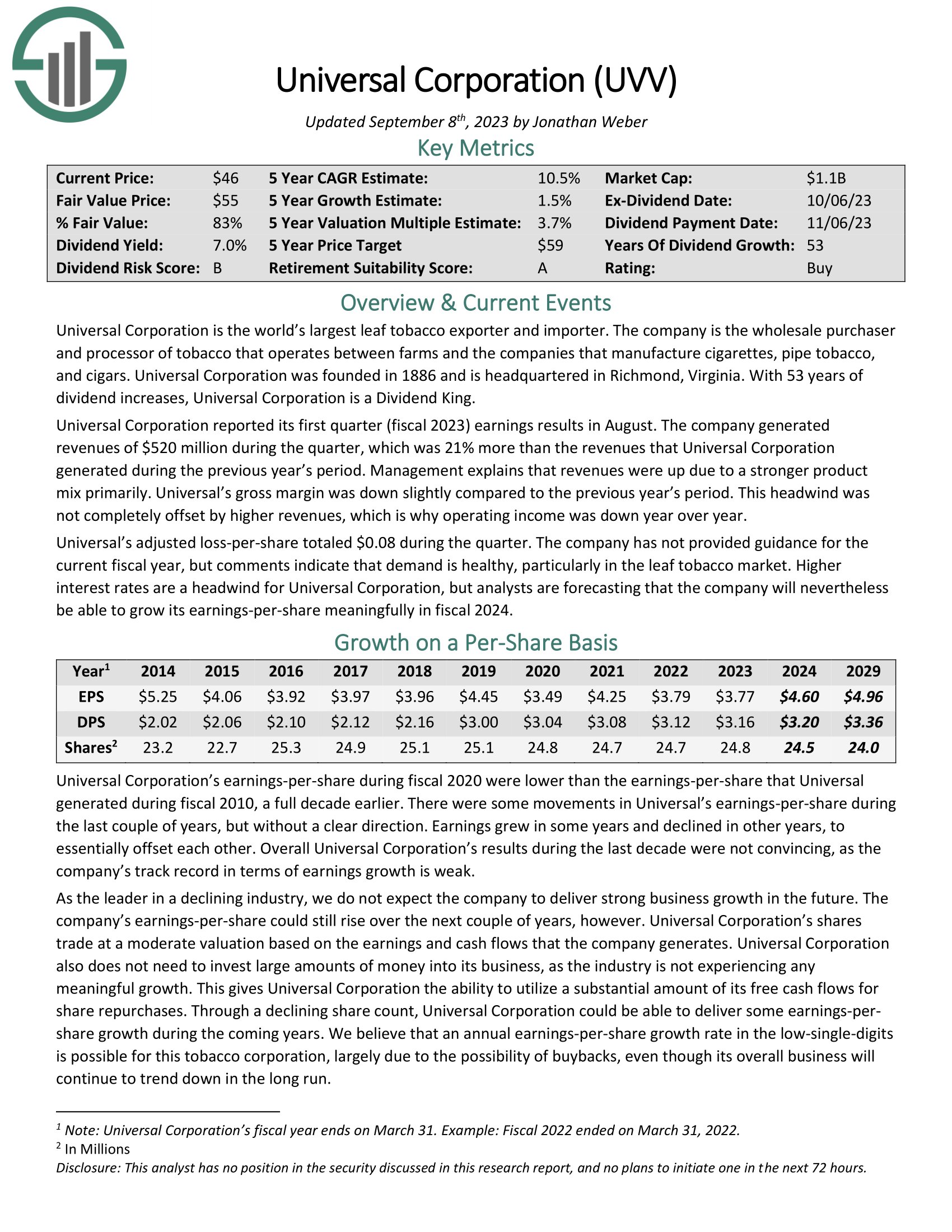

Universal Corp. (UVV)

Our first sin stock is Universal Corporation, which is a supplier of tobacco leaf and plant-based food ingredients worldwide. The company has a spotty history of growth given it is beholden to global demand for cigarettes and cigars, which has been waning for many years. The rate of decline is slow, however, so we believe Universal has the ability to pay its ample dividend for many years to come.

Universal also has an ingredients business that is separate from the core leaf segment.

Source: Investor Presentation, page 26

We see 1.5% growth moving forward, as pricing increases should help offset declines in overall demand. The stock is trading for slightly more than our estimate of fair value, so shareholder returns could be partially offset by a reversion to fair value at 13 times earnings.

Universal, however, has an outstanding dividend increase streak of 51 years, making it a Dividend King. This longevity, as well as the 6.5% dividend yield, make Universal a dividend stock buy.

Click here to download our most recent Sure Analysis report on UVV (preview of page 1 of 3 shown below):

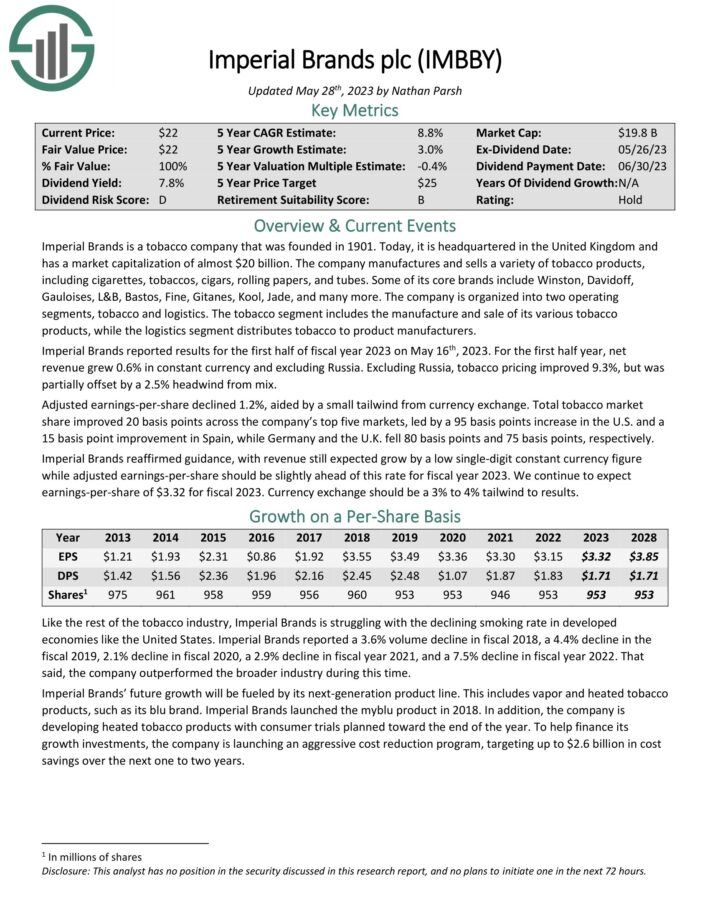

Imperial Brands PLC (IMBBY)

Our next sin stock is Imperial Brands, which is a maker of various tobacco products, including cigars and cigarettes, as well as vaping, oral nicotine, and heated tobacco products that operates globally. Imperial was founded in 1901 and is based in the United Kingdom.

Imperial Brands reported results for the first half of fiscal year 2023 on May 16th, 2023. For the first half year, net revenue grew 0.6% in constant currency and excluding Russia. Excluding Russia, tobacco pricing improved 9.3%, but was partially offset by a 2.5% headwind from mix.

Adjusted earnings-per-share declined 1.2%, aided by a small tailwind from currency exchange. Total tobacco market share improved 20 basis points across the company’s top five markets, led by a 95 basis points increase in the U.S. and a 15 basis point improvement in Spain, while Germany and the U.K. fell 80 basis points and 75 basis points, respectively.

Imperial Brands reaffirmed guidance, with revenue still expected grow by a low single-digit constant currency figure while adjusted earnings-per-share should be slightly ahead of this rate for fiscal year 2023.

Click here to download our most recent Sure Analysis report on IMBBY (preview of page 1 of 3 shown below):

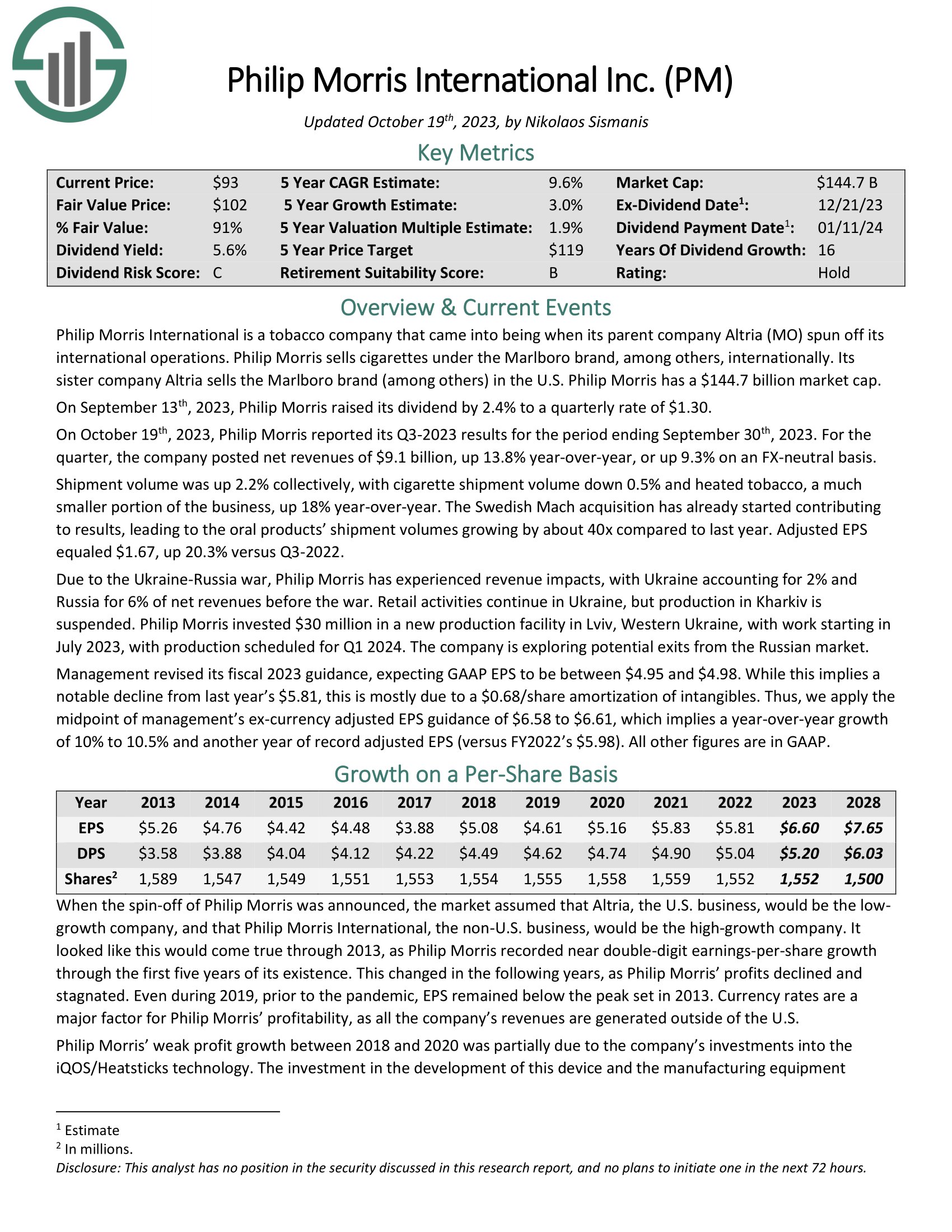

Philip Morris International Inc. (PM)

Next up is Philip Morris, one of the largest tobacco companies in the world by market cap. Philip Morris makes and distributes a variety of cigarettes and related products outside the U.S.

However, it is on a long-term journey to eventually move smokers off of its tobacco products and into smoke-free products. Over time, Philip Morris plans to cease being a tobacco company, but that is still many years away. For now, it is firmly in the category of sin stocks, and a rather good one.

Growth in earnings has been challenging in recent years as the company is subject to foreign exchange fluctuations, as well as waning demand for cigarettes in particular. We think Philip Morris can add 3% annually to earnings, on average, driven by pricing increases and share repurchases.

The company has a 15-year streak of dividend increases, which began when it was spun from former parent Altria, which we’ll look at below. We think Philip Morris has a robust dividend story behind it, but also looking forward.

The stock is yielding 5.7% today, making it another high-yield sin stock at almost four times that of the S&P 500. Philip Morris trades right at fair value, so we don’t see any impact going forward on returns from the valuation.

Click here to download our most recent Sure Analysis report on PM (preview of page 1 of 3 shown below):

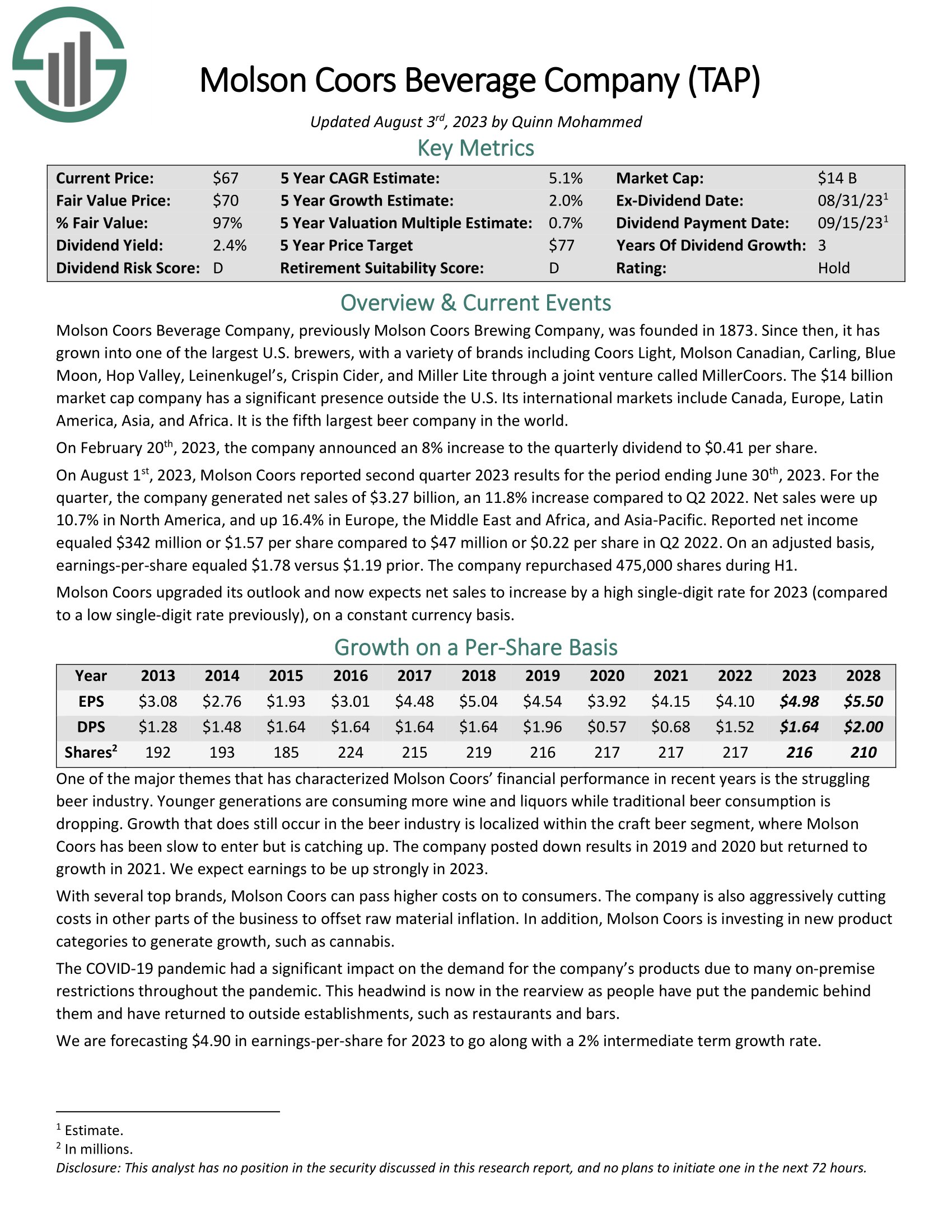

Molson Coors Beverage Company (TAP)

Molson Coors is a manufacturer and distributor of beer and malt beverages that operates globally. The company owns ubiquitous brands such as Coors, Molson, and Blue Moon, and has an enviable global distribution network.

Growth has been hard to come by in recent years after a rapid ascension out of the Great Recession. Since peak earnings were hit in 2018, Molson Coors has struggled somewhat to produce earnings growth. We see 2% growth going forward as the company has recognizable brands with pricing power, and as the company is aggressively cutting costs.

Molson Coors cut its dividend during the COVID recession, so its increase streak stands at just two years. The dividend is nearly back to pre-COVID levels, however, and the yield is at nearly 3% today, which is nearly double that of the S&P 500.

Shares also trade about 10% below fair value, so we see a nice tailwind to returns from the valuation in the years to come. Combined with the yield and projected growth, we think Molson Coors can produce ~9% total returns in the coming years.

Click here to download our most recent Sure Analysis report on TAP (preview of page 1 of 3 shown below):

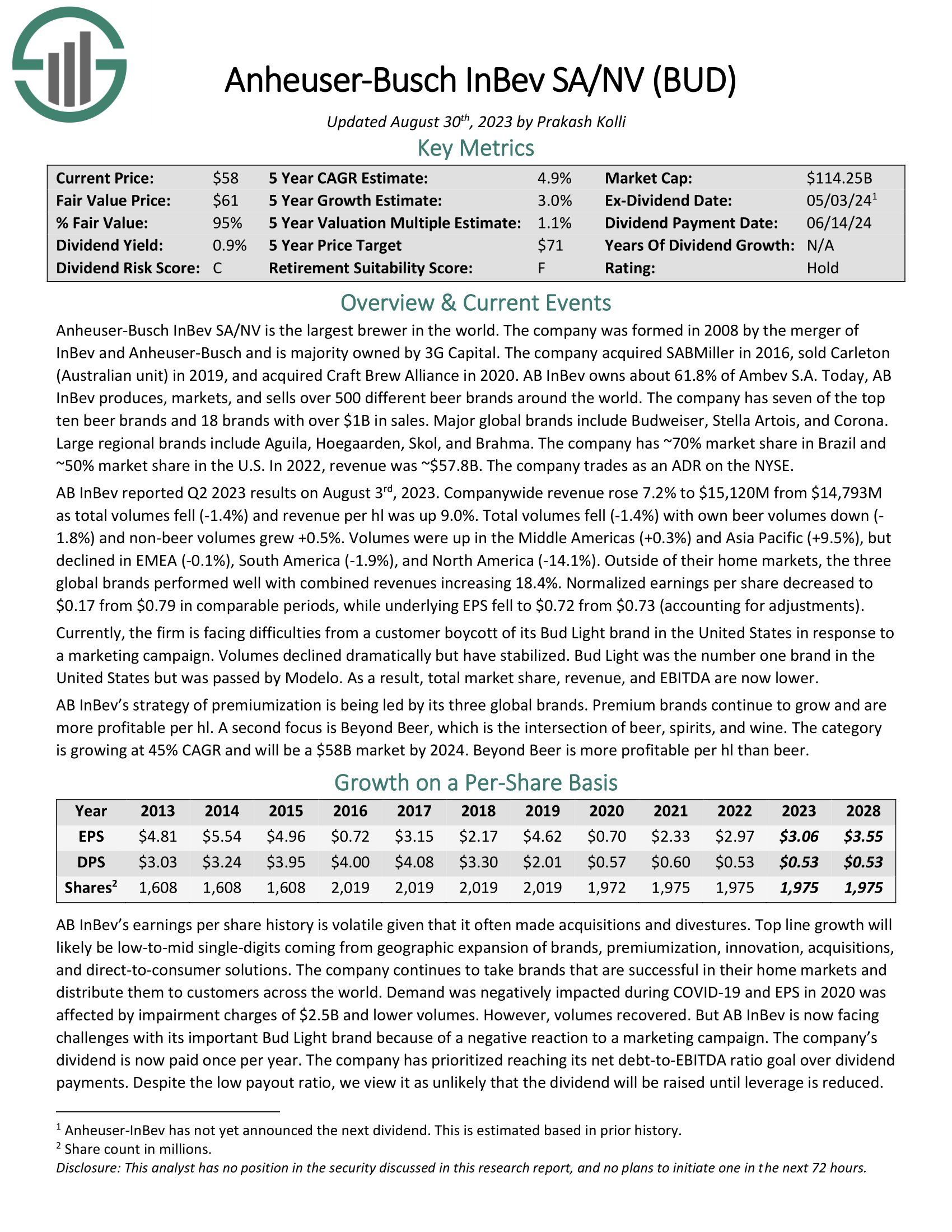

Anheuser-Busch InBev SA/NV (BUD)

Our next stock is Anheuser-Busch InBev, which is the combination of the formerly separate Anheuser-Busch and InBev businesses that merged in 2008. That merger created the largest alcoholic beverage company in the world, and one that owns 500 different beer brands. These include Budweiser, Corona, Stella Artois, Michelob Ultra, Modelo, and more of some of the world’s most popular beers.

Overall, AB-InBev has 17 individual beers that each generate at least $1 billion in annual sales.

Source: Investor Presentation

AB InBev has a spotty history with earnings growth, as it sees peaks and troughs over time. This history of uneven growth meant that the dividend was unsustainable in 2016 and 2017, and was cut sharply. The company now pays a much lower, variable dividend each year.

That dividend is good for a current yield around 1% today, meaning the stock is one of the lowest-yielding sin stocks in the market today.

Click here to download our most recent Sure Analysis report on BUD (preview of page 1 of 3 shown below):

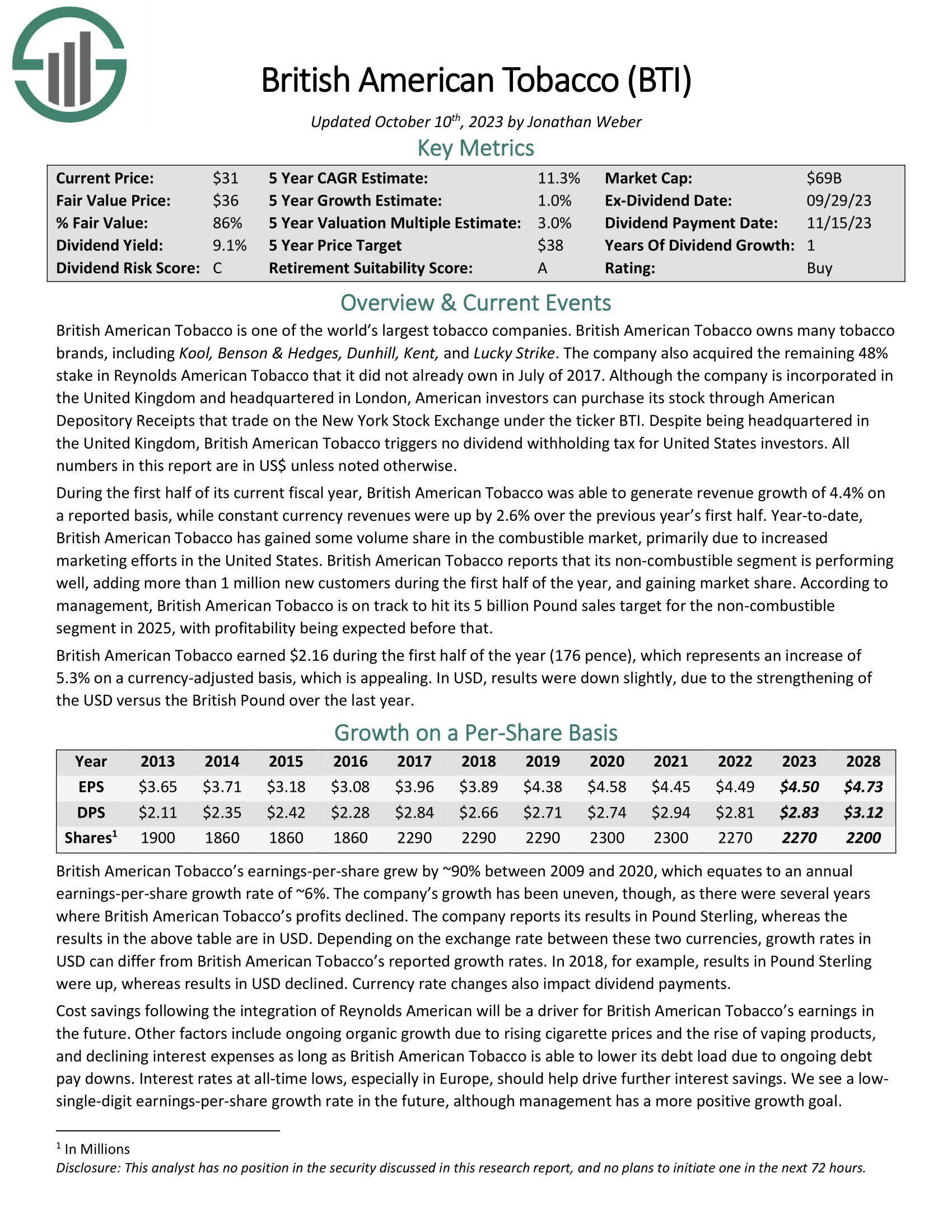

British American Tobacco PLC (BTI)

Our next stock is British American Tobacco, a company that makes and distributes a wide variety of cigarettes, snuff, heated tobacco, and oral nicotine products globally. The company owns some highly lucrative brands, including Camel, Lucky Strike, and Newport, among others.

British American Tobacco managed to boost earnings in the past decade, although progress has seen some starts and stops. Still, we think 3% growth looking forward is reasonable given the company’s focus on share repurchases, as well as its pricing power with its strong suite of brands.

The company pays a variable dividend each year, so its streak of dividend increases stops rather frequently. In addition, dividends are declared in British pounds, so there is a measure of currency translation risk for U.S. investors. Even so, the stock yields more than 7% today, making it a very strong income stock on that measure.

Shares trade slightly below fair value, so we see a modest tailwind to total returns from the valuation in the coming years. Combined with the huge yield and 1% annual EPS growth, that should be good enough for the stock to produce ~11% total annual returns over the next five years.

Click here to download our most recent Sure Analysis report on BTI (preview of page 1 of 3 shown below):

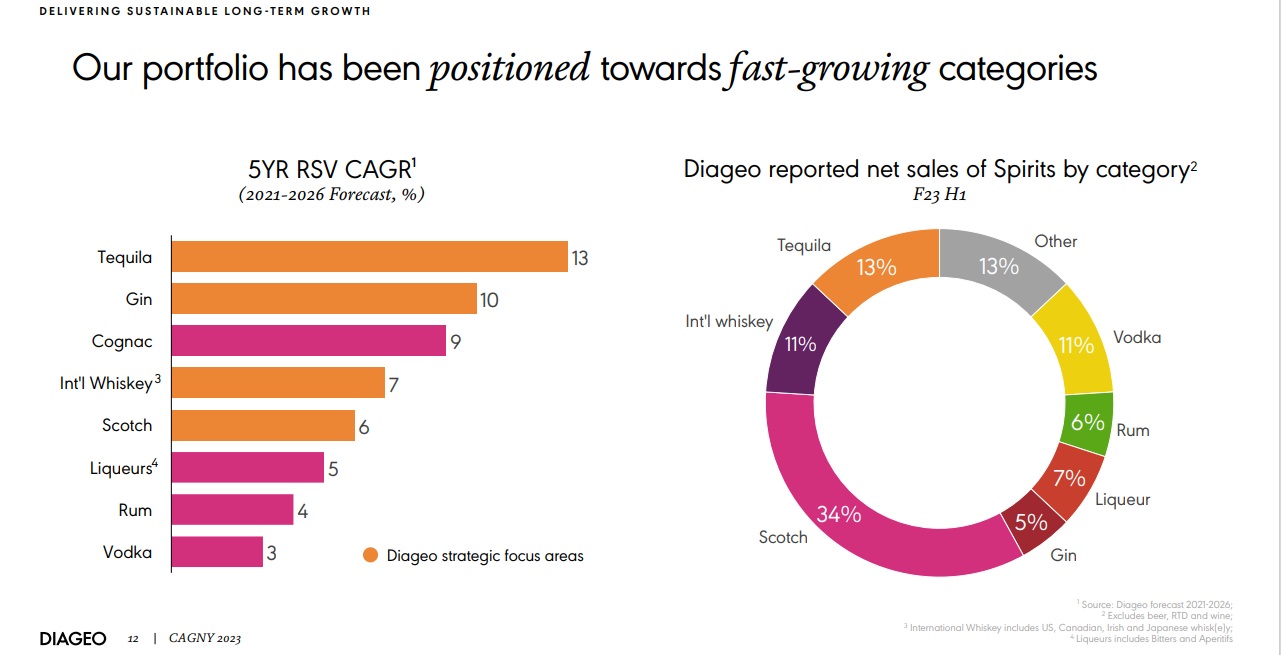

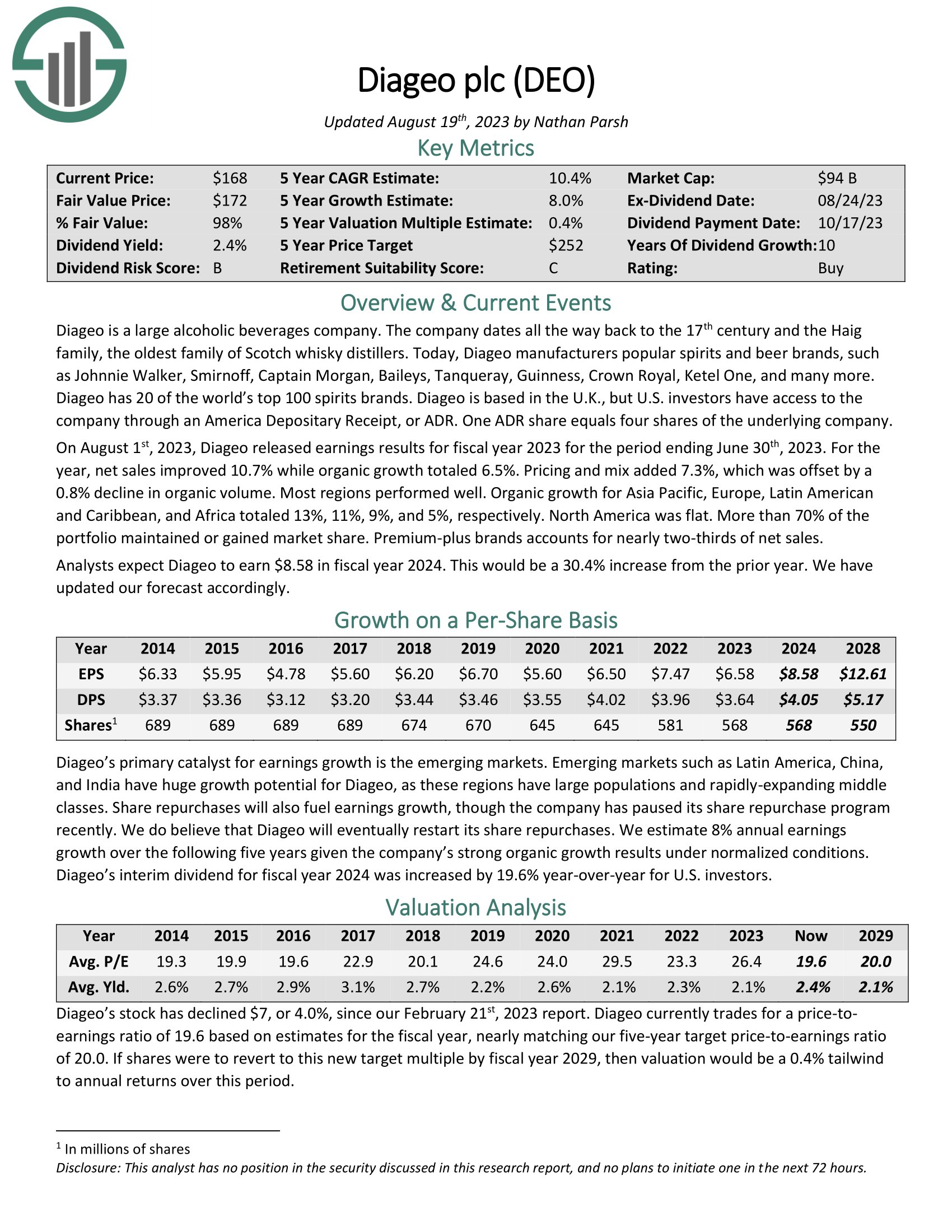

Diageo PLC (DEO)

Diageo manufacturers some of the most popular spirits and beer brands in the world, such as Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, Guinness, Crown Royal, Ketel One, and many more. In all, Diageo has 20 of the world’s top 100 spirits brands.

Source: Investor Presentation

Diageo raised its dividend for nine consecutive years, and we expect that streak to get much longer over time. Diageo’s payout ratio is under half of earnings, and its rapid earnings growth rate should afford it the ability to continue to increase the dividend indefinitely. The current yield is 2.4%, so while it’s not a pure income stock, it’s still about 1.5 times that of the S&P 500. In addition, shareholders get strong growth potential from the dividend with Diageo.

The stock is trading just under fair value, so we see a modest tailwind to returns from that. All told, we expect to see ~11% total annual returns in the years to come, mostly from earnings growth.

Click here to download our most recent Sure Analysis report on DEO (preview of page 1 of 3 shown below):

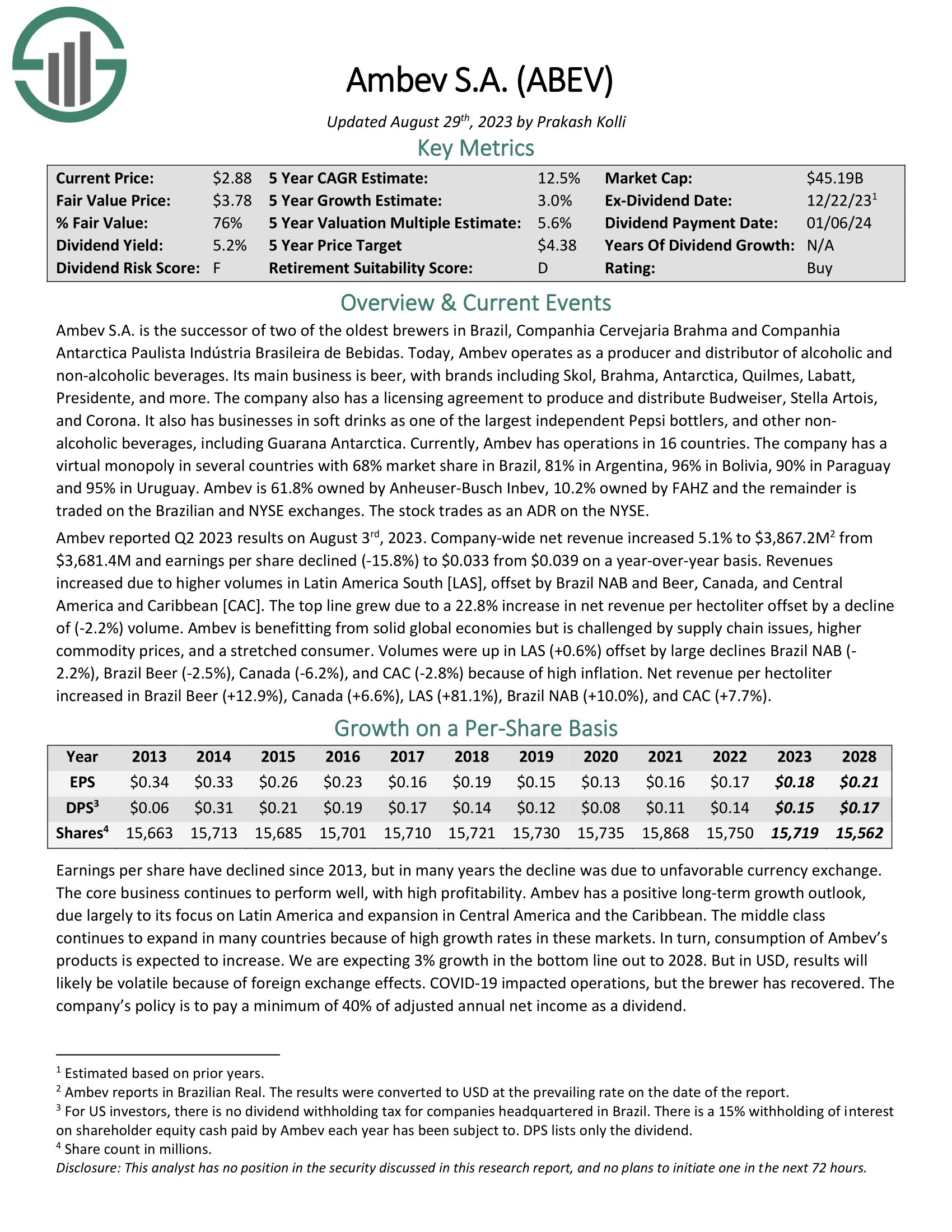

Ambev SA (ABEV)

Ambev is our next sin stock, a company that makes and distributes a variety of drinks, most of which are alcoholic. The company sells beer, draft beer, carbonated soft drinks, malt, and food products throughout much of the Western Hemisphere. The company does not compete in the United States.

Ambev has struggled somewhat with profitability over the years, owed to fluctuating revenue totals from year to year. Looking ahead, we think the company can average 3% growth in earnings from slightly higher revenue, and strong margins. We note that foreign exchange is a big line item for Ambev given the wide variety of geographies where it competes, so results can fluctuate from year to year for that reason.

Ambev pays a variable dividend, so like some of the others on this list, it sees cuts from time to time. The current payout is good for a 5% dividend yield, which is quite attractive. It’s equal to about two-thirds of net income, so we don’t necessarily see a huge runway for growth in the payout, but the current yield is nice.

Shares trade at about a 20% discount to fair value, so we think the valuation could produce a roughly 5% tailwind to total returns each year for the foreseeable future.

Click here to download our most recent Sure Analysis report on ABEV (preview of page 1 of 3 shown below):

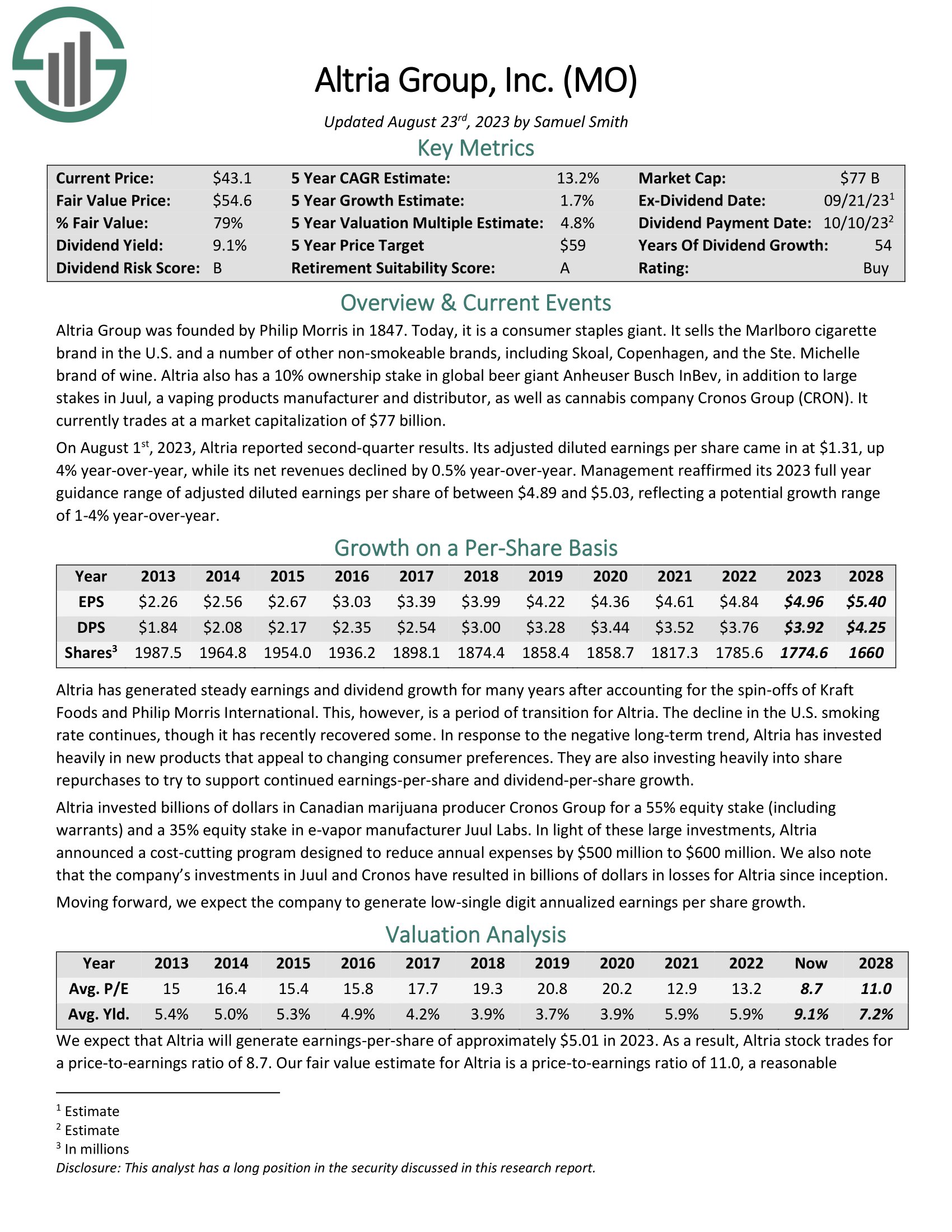

Altria Group Inc. (MO)

Altria Group was founded by Philip Morris in 1847. Today, it is a consumer staples giant. It sells the Marlboro cigarette brand in the U.S. and a number of other non-smokeable brands, including Skoal and Copenhagen.

Altria has increased its dividend for over 50 years, placing it on the exclusive Dividend Kings list. This is a rare business longevity achievement that speaks to the staying power of the company’s brands, even with the gradual decline in smoking in the U.S.

Source: Investor Presentation

On August 1st, 2023, Altria reported second-quarter results. Its adjusted diluted earnings per share came in at $1.31, up 4% year-over-year, while its net revenues declined by 0.5% year-over-year.

Management reaffirmed its 2023 full year guidance range of adjusted diluted earnings per share of between $4.89 and $5.03, reflecting a potential growth range of 1-4% year-over-year.

Click here to download our most recent Sure Analysis report on Altria (preview of page 1 of 3 shown below):

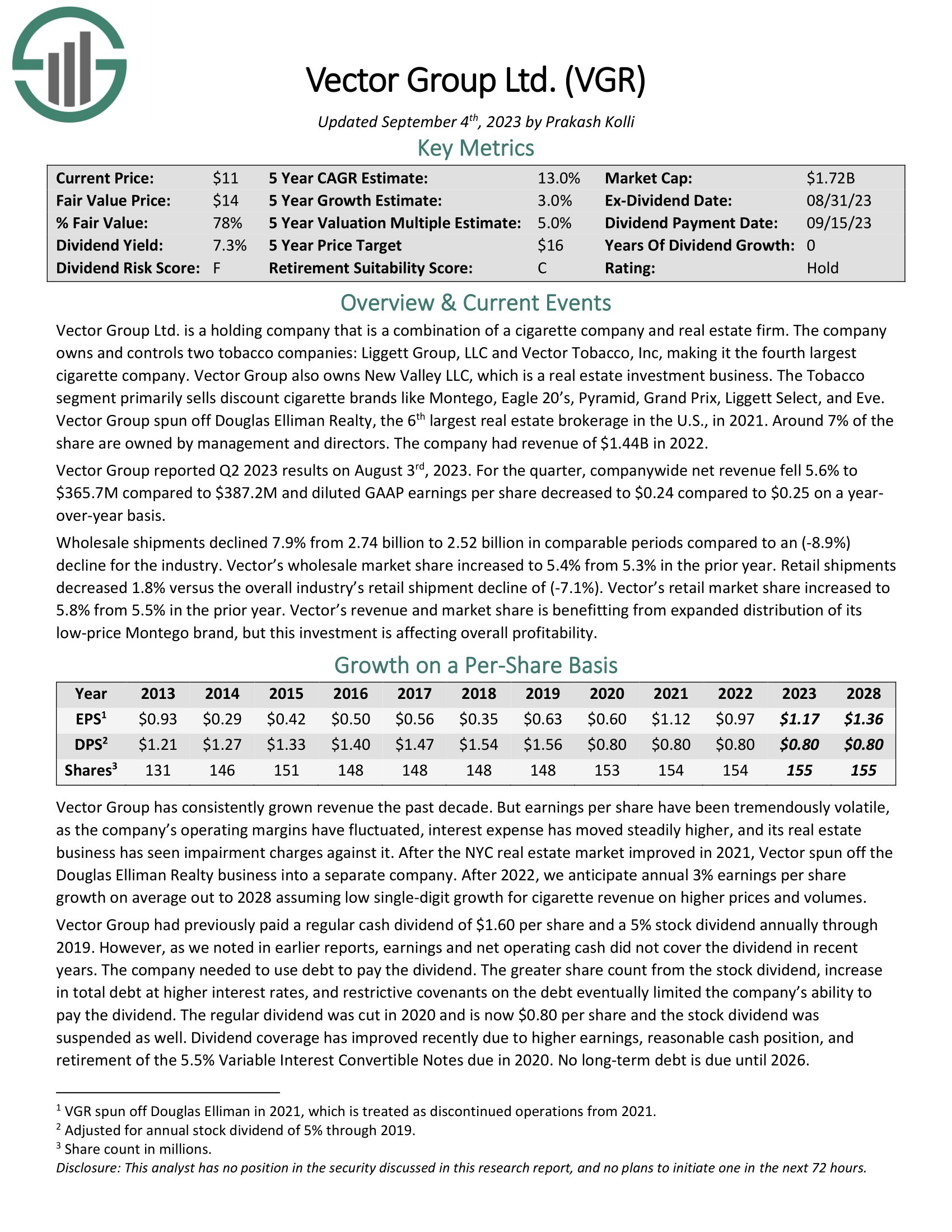

Vector Group Ltd. (VGR)

Our final stock is Vector Group, a conglomerate that makes and sells cigarettes in the U.S, as well as a real estate business that invests in properties. Vector’s primary business is selling cigarettes, a portfolio that includes about 100 brands, mostly in the lower end of the market that competes on price.

Growth has been quite good for Vector, including 2021 that saw a near doubling of earnings-per-share. We see strong earnings again this year, followed by 3% growth in the years to come.

Vector previously had an unsustainable dividend, but it was cut in 2020 and has been flat ever since. Even so, the stock yields over 7%, which will drive strong total returns in the years to come.

Click here to download our most recent Sure Analysis report on VGR (preview of page 1 of 3 shown below):

Final Thoughts

While sin stocks generally don’t offer a huge amount of growth to investors, they often sport very high dividend yields, and trade for reasonable earnings multiples. This list includes some high-yield names, good value stocks, and a couple of higher growth names. All pay dividends, and all offer good total return prospects for the years to come.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

believes that despite near-term challenges, the long-term prospects for housing remain strong")

{kind=link}